Kevin Hagen/Getty Images News

Undoubtedly, one of the most controversial, but also most diverse, companies in the entertainment space is Fox Corporation (NASDAQ:FOX) (NASDAQ:FOXA). As the parent of Fox News, the company has long been a business loved by many and hated by many at the same time. Irrespective of this mixed public perception, there is no denying that the business offers investors with some interesting prospects. Today, shares of the enterprise look to be attractively priced. The historical financial performance of the business has been generally positive even as it struggles in some rather important ways. On the whole, for investors who don’t mind the controversy and who are value-oriented, this may make for an interesting prospect moving forward. But it’s certainly not a player that is without its downsides.

A diverse play in entertainment

Today, Fox is a standalone news, sports, and entertainment company that owns a variety of key valuable properties. Operationally, the business has three different segments that it runs. The first of these to pay attention to is the Cable Network Programming segment, which is responsible for the production and licensing of news and sports content distributed mostly through traditional cable television systems, direct broadcast satellite operators, and various telecommunications companies. The segment also offers content through online multi-channel video programming distributors across the US. Properties here include Fox News Media (which includes both Fox News and Fox Business), as well as the company’s cable sports programming networks known as FS1, FS2, the Big Ten Network, and Fox Deportes. During the company’s 2021 fiscal year, this particular segment was responsible for 44% of the firm’s overall revenue and 83.8% of its positive segment profits.

The other big segment the company has is the Television segment. This particular unit is responsible for the ‘production, acquisition, marketing, and distribution of broadcast network programming and free advertising-supported video-on-demand services’ under both the Fox and Tubi brand names. Its properties consist of 29 broadcast television stations, eleven of which are classified as duopolies. last year, this segment was responsible for 54.6% of the company’s overall revenue and just 16.2% of its positive segment profits. The final segment the company has is the Other, Corporate and Eliminations segment. This consists of a few miscellaneous properties, such as the Fox Studio Lot, Credible Labs, and everything covering the firm’s miscellaneous corporate overhead operations. It was responsible for just 1.44% of the firm’s sales last year and generated a loss.

Author – SEC EDGAR Data

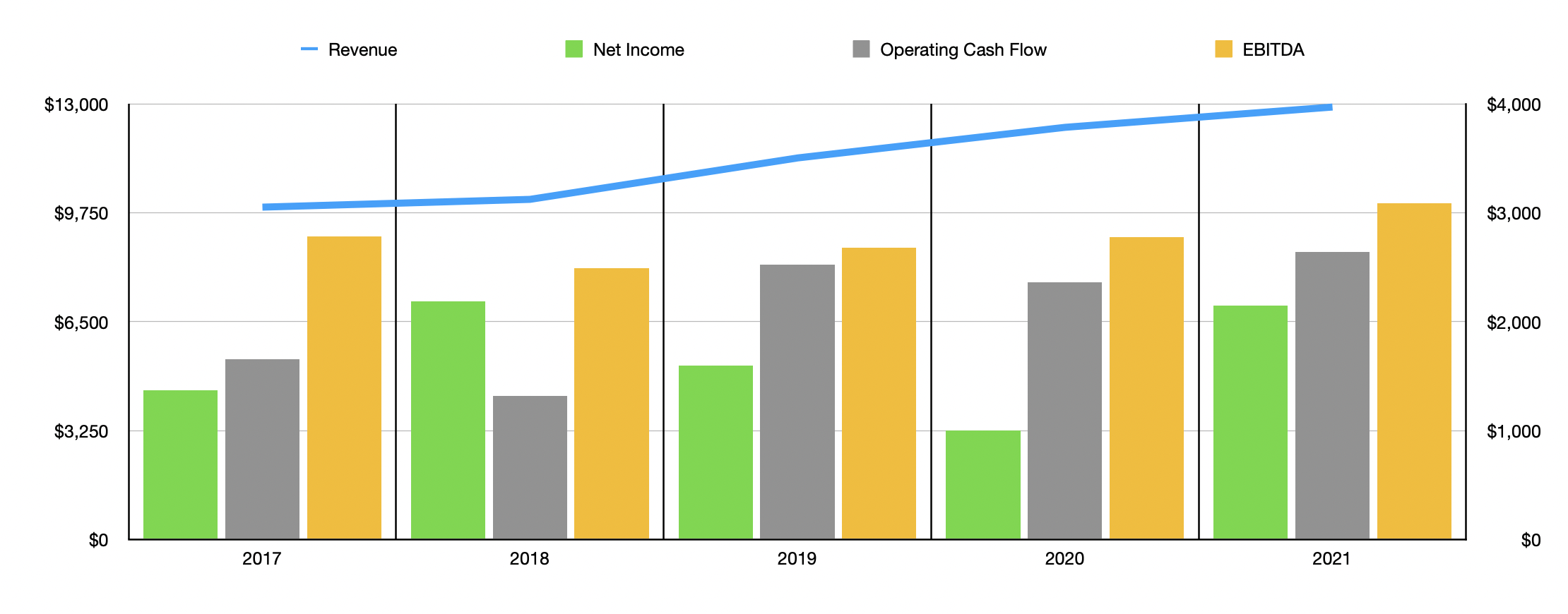

Over the past few years, management has done well to grow the company’s top and bottom lines. As an example, we need only look at revenue first. between 2017 and 2021, revenue increased year after year, climbing from $9.92 billion to $12.91 billion. Interestingly, this increase in revenue came as some of the company’s other numbers that relate to the top line have suffered. Although revenue for its Cable Network Programming segment increased during this window, climbing from $4.32 billion to $5.68 billion, the business actually suffered a decline in subscribers on its platform. Data has not been provided for 2017 specifically. But in 2018, as an example, Fox News had 87 million subscribers, while Fox Business had 84 million. By the end of the company’s 2021 fiscal year, these numbers had dropped to 77 million and 73 million, respectively.

Other cable networks owned by the company have also suffered during this timeframe. FS1 and FS2 also posted declines, with their numbers dropping from 83 million and 58 million down to 74 million and 54 million, respectively. Meanwhile, The Big Ten Network and Fox Deportes saw their numbers drop from 58 million and 21 million down to 51 million and 16 million, respectively. To be fair, management did claim that Nielsen, which reports these figures, experienced a disruption in its ability to maintain the efficacy of its in-home panel as a result of the COVID-19 pandemic, which they believe had a negative impact on subscriber and audience estimates in the 2021 fiscal year. Even if this is the case, there would have been declines in recent years. Despite the issues associated with declining cable network data, growth for the business has continued into the current fiscal year. Revenue in the first six months of its 2022 fiscal year, for instance, came in at $7.49 billion. That represents a sizable increase over the $6.80 billion reported at the same time or near earlier.

Author – SEC EDGAR Data

In recent years, profitability for the company has been much more volatile than revenue has been. But the overall trend has been positive. Between 2017 and 2021, net income at the business expanded, climbing from $1.37 billion to $2.15 billion. The high point in the past five years was the $2.19 billion management reported for 2018, while the low point was the $999 million the company generated in 2020. There are, of course, other profitability metrics to consider. Operating cash flow is one such example. Between 2017 and 2021, this metric grew from $1.66 billion to $2.64 billion. Meanwhile, EBITDA expanded from $2.79 billion to $3.09 billion, but not before dipping at one point to $2.49 billion in 2018.

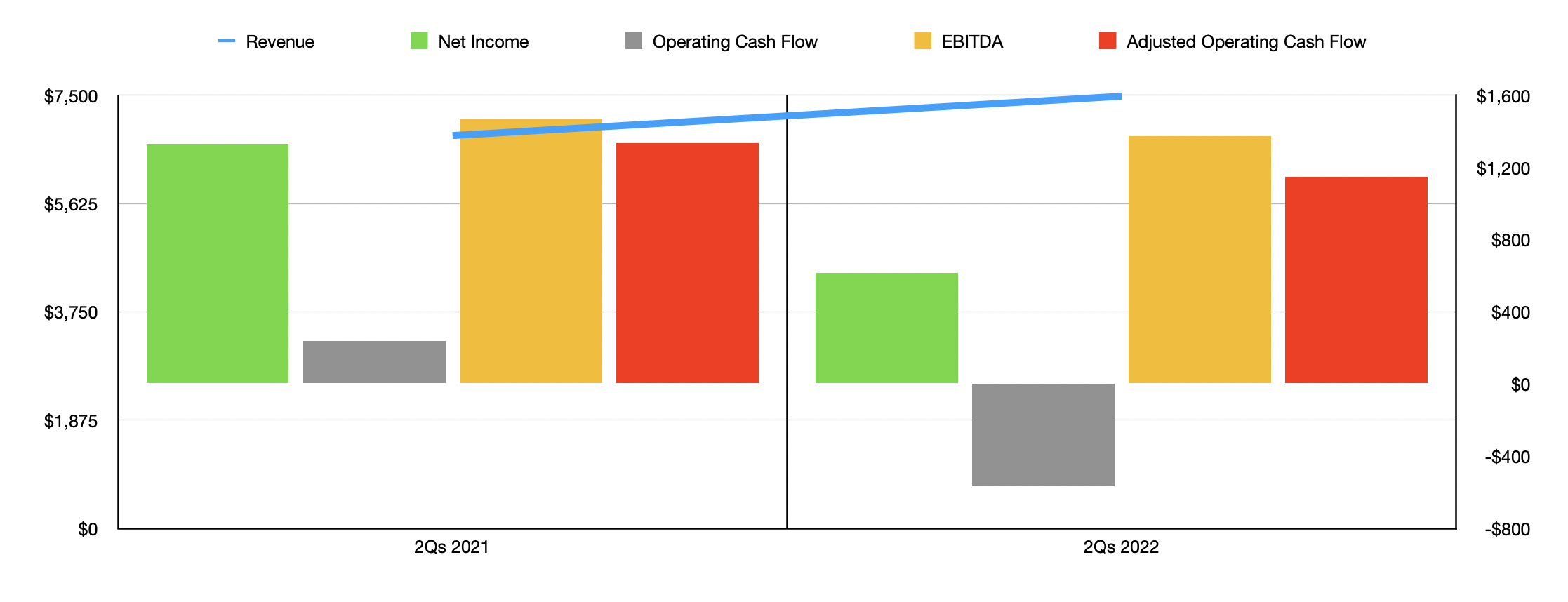

Looking into the 2022 fiscal year, financial results for Fox have been rather mixed. Net profits, for instance, totaled just $616 million in the first half of 2022. That compares to the $1.33 billion generated one year earlier. Operating cash flow, meanwhile, declined from $237 million to negative $656 million. But if we adjust for changes in working capital, the decline would have been more modest, with the figure dropping from $1.34 billion to $1.15 billion. Another metric that also experienced a slight drop during this timeframe was EBITDA, with it ultimately declining from $1.47 billion to $1.37 billion. Management provided no guidance for the company’s 2022 fiscal year. But if we analyze the results experienced so far for the year, we should anticipate operating cash flow of about $2.27 billion and EBITDA of around $2.88 billion. Due to how volatile earnings have been, I do not believe that valuing the company based on that would be ideal.

Author – SEC EDGAR Data

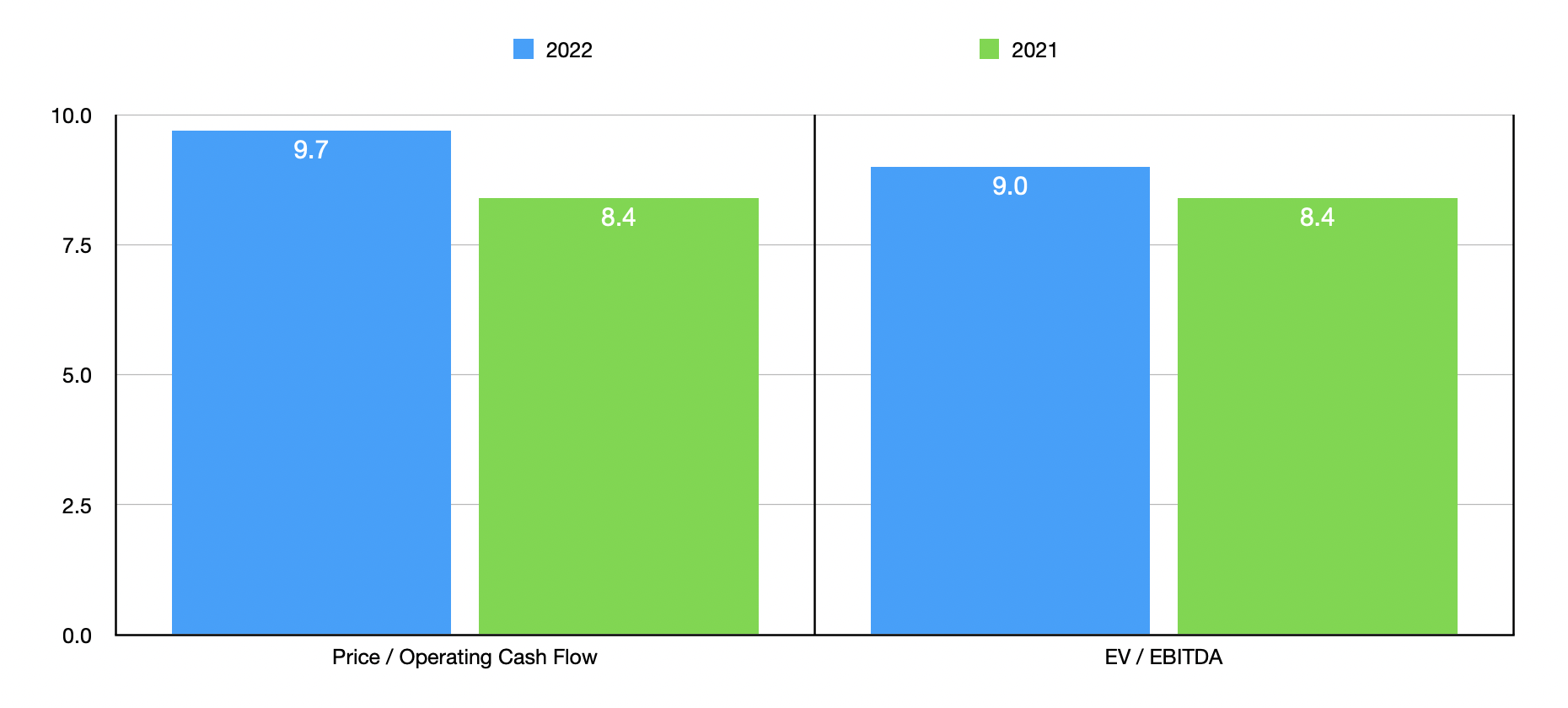

Taking all of these figures, we can effectively price the business. Using the 2021 results reported by management, we find that the firm is trading at a price to operating cash flow multiple of 8.4. This increases some to 9.7 if we use 2022 estimates. Meanwhile, the EV to EBITDA multiple for the company would climb from 8.4 this year to 9 next year. To put this all in perspective, I decided to compare the company to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 6 to a high of 25.1. Three of the five firms were cheaper than our prospect. Using the EV to EBITDA approach, the range was from 8.3 to 19.6. In this case, only one of the five firms was cheaper than Fox.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Fox Corporation | 8.4 | 8.4 |

| Nexstar Media Group (NXST) | 6.4 | 8.7 |

| Paramount Global (PARA) | 25.1 | 8.7 |

| TEGNA (TGNA) | 9.9 | 8.6 |

| Discovery (DISCA) | 6.1 | 8.3 |

| Sinclair Broadcast Group (SBGI) | 6.0 | 19.6 |

Takeaway

Based on all the data provided, I can say that, fundamentally, Fox looks to be a solid operator in its space. The business has a lot of valuable properties and management has done well to grow revenue and cash flows over the past few years. Shares of the company look to be on the cheap side, particularly on an absolute basis. So for those investors who care more about the numbers than the reputation, this may be a good long-term play to consider. Of course, the long-term success of the business will be determined by how many eyeballs the business can attract. And if we do see some continued long-term decline in subscribers for its Cable Network Programming segment, some of the firm’s potential could be mitigated.

Read More: Fox Corporation Stock: Fundamentally Appealing (NASDAQ:FOX)

{kind=link}