KanawatTH/iStock via Getty Images

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on May 13th, 2022.

Clough Global Opportunities (NYSE:GLO) is a fairly unique fund. It invests in both U.S. and foreign equities and bonds. The fund even has the ability to go short on investments, but that is generally a smaller sleeve of the portfolio. Additionally, they have various derivatives that they implement to varying degrees.

These derivatives include swaps, futures, and options. Overall, they are a hybrid fund that is basically unconstrained to invest wherever they’d like. That can make it a bit of a “black box” type of investment. Due to not having daily positioning available for investors to see in the CEF structure, you just never know exactly what they might be holding at any one time.

I often apply that black box label to PIMCO funds. Except, they take various derivatives to the next level with just about every sort of instrument you can think of, especially with their PIMCO Global StocksPLUS & Income Fund (NYSE:PGP). The main strategy behind PGP is the futures and options contracts that give the fund a hybrid style of exposure to equities while holding primarily a fixed-income portfolio.

I believe the lack of knowing exactly how they might be positioned makes them more of a black box. With other CEFs, you have a general idea of the types of stocks and bonds they might be holding in a given period and how they might be impacted due to different circumstances. The sheer number of different interest rate swaps and forward foreign currency contracts means that it can be a bit harder to follow when taken all together.

I wanted to make sure to expand on that subject, as my last PGP article seemed to spur some pushback from ADS Analytics in an article shortly after. Admittedly, well-deserved criticism. I should have been more thorough in the point I was trying to get across when saying “black box.” Constructive criticism is always appreciated as it pushes us to be better investors.

This type of flexibility can be a great thing for a fund manager if they can be successful with it. Unfortunately, with GLO, they had an incredible year in 2020 but have seemingly faltered since. 2021 was a strong year, for the most part, separate from growth investments that started to take a turn for the worse towards year-end.

Combining their poorer performance with a fund that often trades at a bit of a premium, I don’t find this a compelling investment option at this time. PGP might be a better option with similar flexibility as a hybrid fund, providing a better track record.

The Basics

GLO

- 1-Year Z-score: 0.44

- Premium: 1.29%

- Distribution Yield: 14.45%

- Expense Ratio: 2.20%

- Leverage: 35.23%

- Managed Assets: $730.1 million

- Structure: Perpetual

GLO’s investment objective is “to provide a high level of total return.” The fund attempts to achieve this by “applying a fundamental research-driven investment process and will invest in equity and equity-related securities as well as fixed-income securities, including both corporate and sovereign debt.” They also include that the fund will “invest in both U.S. and non-U.S. markets.”

The fund’s expense ratio comes to 2.20% and climbs to 2.78% when including leverage expenses. The interest expenses will climb as they are based on three-month LIBOR plus 0.70%. The managed assets and leverage were as of the latest Fact Sheet they provided. Since then, managed assets would have come down, which means leverage would have increased since then.

PGP

- 1-Year Z-score: -2.64

- Discount: 2.99%

- Distribution Yield: 10.64%

- Expense Ratio: 1.66%

- Leverage: 39.53%

- Managed Assets: $158 million

- Structure: Perpetual

The objective of PGP is to “seek total return comprised of current income, current gains and long-term capital appreciation.” They attempt to achieve this through an “innovative StocksPLUS approach, pioneered by PIMCO…” They will “build a global equity and debt portfolio by investing at least 80% of the fund’s net assets in a combination of securities and instruments that provide exposure to stocks and/or produce income.”

As we highlighted above, most of the equity exposure comes via future contracts, but the “fund’s stock exposure may be obtained through stock holdings and/or through index and other derivative instruments that have economic characteristics similar to U.S. and non-U.S. stocks.”

This just makes the fund mostly a hybrid fund, but they take a different route than compared to some other hybrid CEFs we are more familiar with.

The fund’s expense ratio comes to 1.66%, when including the leverage comes to 2.03%. The fund’s leverage is also going to be subject to a negative impact with interest rates rising. They use largely reverse repurchase agreements. These often have short maturities and will increase as rates rise.

The total amount of managed assets and higher leverage can be one of the negatives for PGP. It makes it a smaller fund, which can potentially cause liquidity issues with a lower average daily trading volume.

Performance Comparison

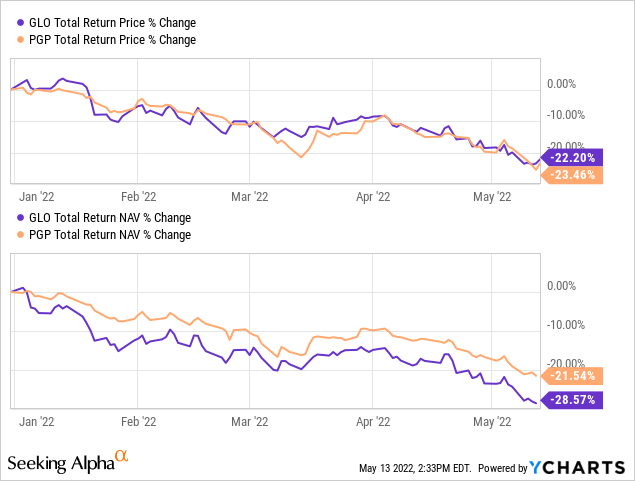

I brought up PGP because I think it could be a fairly attractive option at this time over GLO if one wants this type of flexibility in their funds in the first place. Here is a look at the YTD performance of these funds so far. As we can see, both funds on a total share price basis have performed similarly. At the same time, PGP has held up better overall on a total NAV return.

YCharts

That isn’t to say that there aren’t differences between these funds, just that they also have similarities. While at the same time, I believe that PGP is a fairly better potential option in terms of performance going forward.

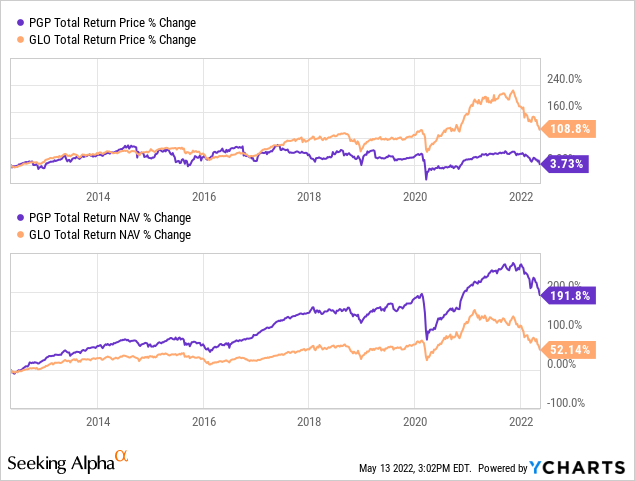

Over the last decade, it hasn’t even been a close competition between these two funds. PGP wins hands down on a total NAV return basis. The total price return is reflecting the extreme premium that PGP once traded at.

One of the benefits is the lower expense ratio, to some small degree. However, the higher leverage would have likely been playing a role too. Just to look back at the YTD, though, it still held up relatively better despite having the higher leverage. For a down year, that is saying something.

YCharts

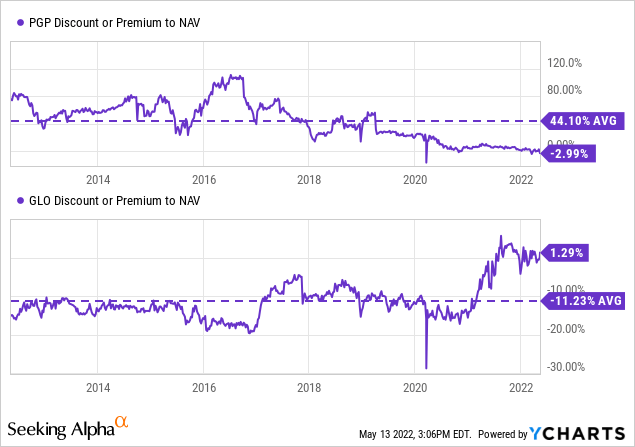

Finally, when it comes to the valuation, PGP is a significantly better deal, relatively speaking. The GLO premium of 1.29% might seem like it isn’t too big of a deal compared to the 2.99% discount of PGP. However, CEFs are more than just their discounts and premiums. The relative discount and premium can have a bigger impact.

That’s why we see a 1-year z-score of -2.64 for PGP and a positive 0.44 for GLO. Looking back historically, we get an even better deal for PGP.

YCharts

I’m not saying we get to the lofty premiums that PGP had traded at frequently previously, but GLO typically traded at a deep discount over the last decade. Even if PGP remains flat from this point and GLO reverts to its historical range, an investor would be better off with PGP.

Distribution

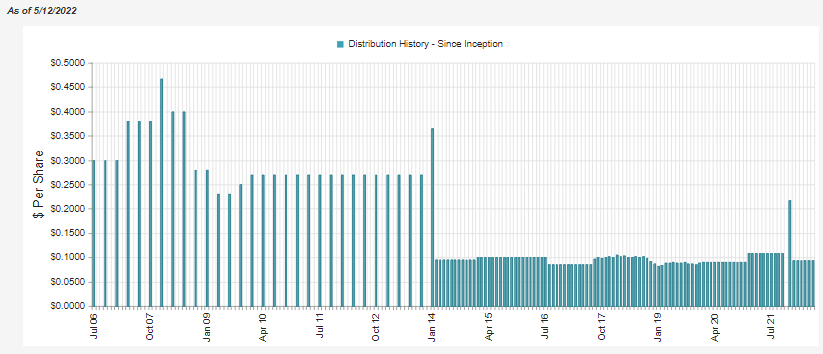

GLO might win in terms of the raw distribution yield, but GLO’s payout is managed to be reset annually. GLO’s latest distribution yield comes to 14.45% based on the $0.0943 paid monthly for this year.

GLO Distribution History (CEFConnect)

GLO’s distribution is based on 10% of its NAV and resets annually based on the last five business days prior to the calendar year-end. If it were reset today, the monthly distribution would drop to $0.0656 based on the average NAV coming to $7.872 over the last five trading days.

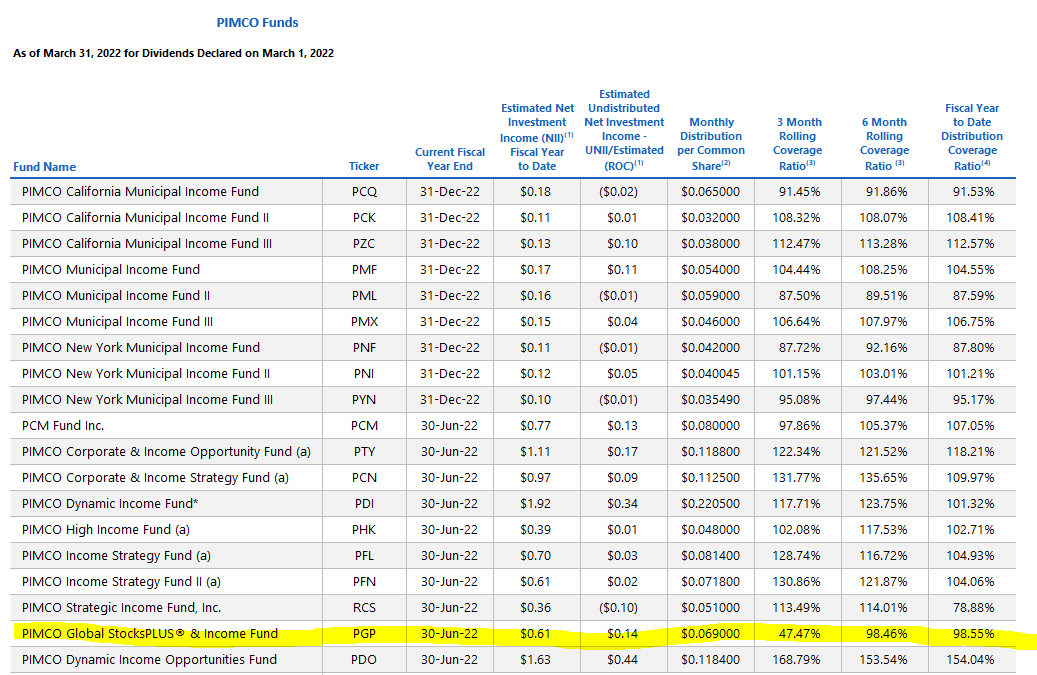

PGP’s distribution isn’t guaranteed, but given the coverage over the last six months, it has a good chance of being maintained. PIMCO has also shown resiliency in cutting its distributions for all its funds. Often, we have seen coverage increase as we get closer to their fiscal year-ends.

PGP Distribution Coverage (PIMCO)

PGP isn’t any stranger to distribution cuts, though, either. They have implemented several going back to around 2016.

PGP Distribution History (CEFConnect)

I have nothing against a managed distribution policy. In fact, I believe that it can provide predictability even for what it takes away from sustainability.

So while GLO’s distribution yield comes in as significantly higher at this time, it is also guaranteed to reset. PGP’s is lower, and while not guaranteed to remain at the same level, isn’t guaranteed to change due to policy.

A Look At GLO And PGP’s Exposure

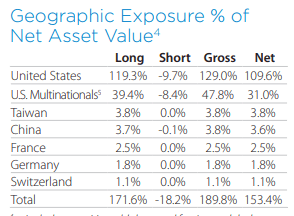

Taking a quick look at the broader view of the portfolio on these funds shows us just how diverse these funds can be. For GLO, we can see that they are short U.S. stocks but still well overweight in U.S. exposure overall.

GLO Geographic Breakdown (Clough)

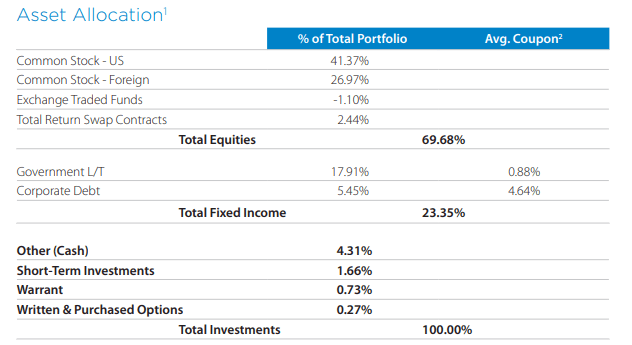

When looking at the asset allocation, it is quite clear that GLO also tends to favor the equity side of the equation.

GLO Asset Allocation (Clough)

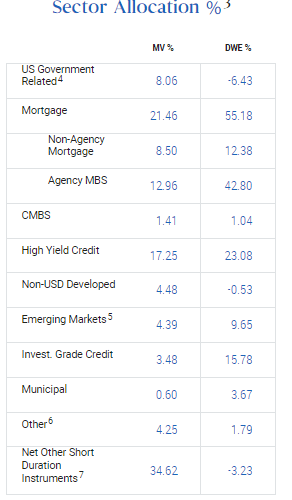

When looking at the sector allocations of PGP, one could be a bit confused at first. On the surface, it would appear it is simply one of its other multi-sector bond funds.

PGP Sector Allocation (PIMCO)

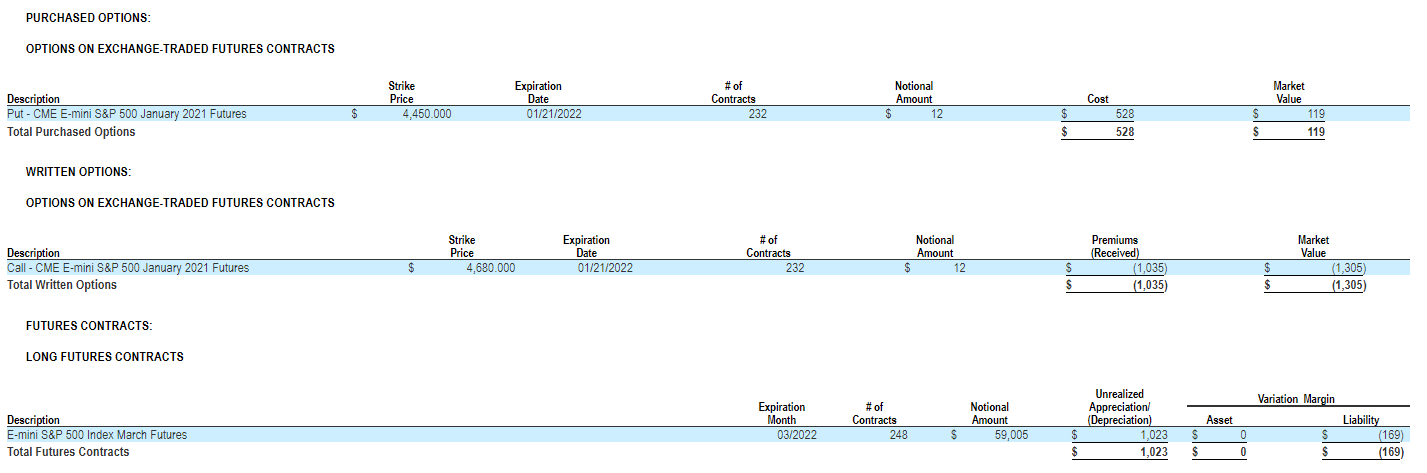

We have to go a bit deeper into the Semi-Annual Report to see where the equity exposure is coming in from. As we can see below, we have the fund buying puts and selling calls – at the same time, they are long futures of the E-mini S&P 500. Buying puts and selling calls, in more simple terms, is implementing a collar strategy.

This is a very defensive strategy as it is buying downside protection through the puts. Then collecting some premium when selling the calls. Selling options provides some downside protection on its own because the breakeven is reduced by the premium collected.

PGP Semi-Annual Report (PIMCO)

Another fund that investors might be familiar with that utilizes a collar strategy is the Eaton Vance Risk-Managed Diversified Equity Income Fund (ETJ). That fund often does relatively better during times of selloffs but does end up lagging when the market rallies too.

I…

Read More: GLO And PGP: PGP Might Be The Better Flexible Fund At This Time

![Just released: the 3 best small-cap stocks to buy right now [PREMIUM PICKS]](https://thedailystock.news/wp-content/uploads/2023/01/GardenFun-350x250.jpg)

{kind=link}