Antony Keetthawee/iStock via Getty Images

Investment Thesis

Since our last analysis on Enphase Energy, Inc. (NASDAQ:ENPH), the stock had risen by 14.96% from $173.05 on 9 March to $198.93 on 3 June 2022. It is evident that the company demonstrated stellar execution in FQ1’22 and provided excellent FQ2’22 guidance, despite the ongoing supply chain issues. In addition, with ENPH’s entry into the EV charging market, we anticipate a vast potential for adoption and growth in the future, given that the EVs still constitute the minority in comparison to ICE vehicles. As a result, it is evident that ENPH remains a solid tech and green energy stock for any interested investors in the coming decade.

Nonetheless, looking at its elevated valuations and stock price, we recommend some patience for investors looking for a comfortable margin of safety. We are also of the opinion that the ENPH stock could potentially retrace to January 2022 lows of $120s, given the overly bearish market and a potential recession. That would give interested investors a better entry point and trading gap to consensus estimates’ price target of $238.83.

ENPH Continues To Deliver Stellar Execution

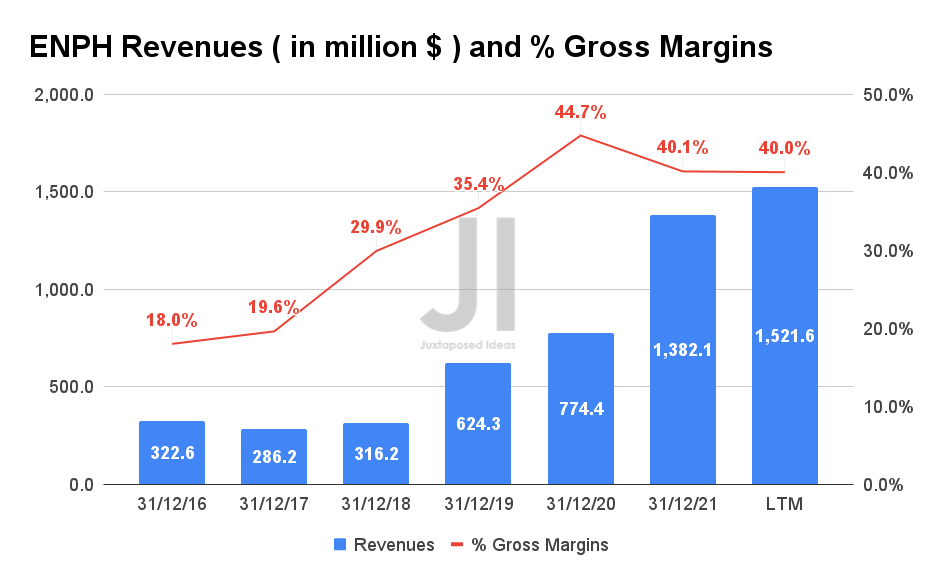

ENPH Revenue and Gross Margin (S&P Capital IQ)

It is apparent that ENPH has been recording tremendous growth in the past two years, while sustaining elevated gross margins of over 40%. In FQ1’22, the company reported revenues of $441.3M and a gross margin of 40.1%, representing a remarkable revenue increase of 6.9% QoQ and 46.2% YoY. ENPH also shipped 2.83M of microinverters and 120.4 megawatt-hours of IQ Batteries in FQ1’22, representing an excellent increase of 15.5% YoY and 286.6% YoY. Furthermore, the company guided an increase of 16.2% QoQ for up to 140 megawatt-hours of IQ Batteries in FQ2’21. As a result, it is evident that ENPH’s revenue is gated by the global supply chain issues, given the robust consumer demand and a 16-week lead time for its products.

Given that ENPH had expected over 40% QoQ growth in its revenues in the EU for Q2’22, it is evident that the company had also grown its investment strategically in Germany, France, Belgium, and the Netherlands. Furthermore, we expect its new markets in Italy, Spain, and Portugal to perform well, since the company aimed to triple its operating expenses in the region moving forward.

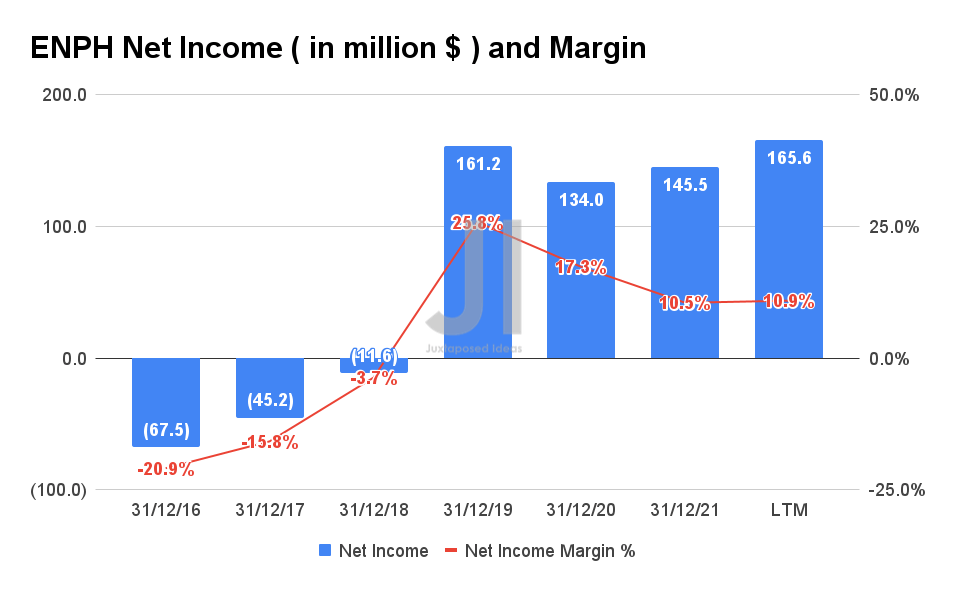

ENPH Net Income and Net Income Margin (S&P Capital IQ)

In addition, ENPH also recorded a net income of $51.82M and a net income margin of 11.7% in FQ1’22, representing a tremendous increase of 63.4% YoY and an improvement by 1.2 percentage points YoY. As a result, investors can rest assured that the company will be able to maintain its margins moving forward, since it was able to pass on rising raw material costs to its consumers.

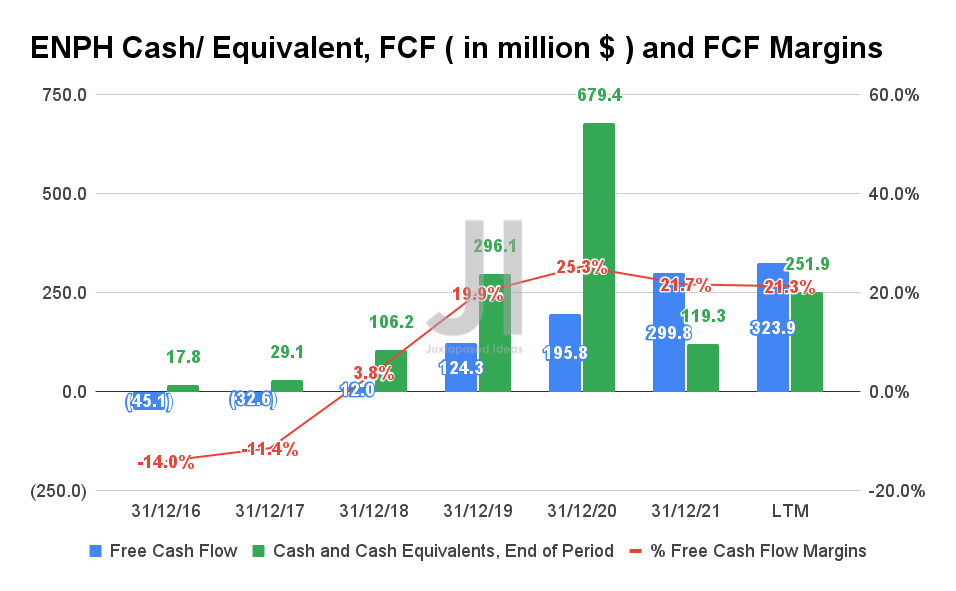

ENPH Cash/ Equivalent, FCF, and FCF Margins (S&P Capital IQ)

Furthermore, given ENPH’s net income and Free Cash Flow (FCF) profitability, investors need not be concerned about its expansion in multiple geographical territories, manufacturing capacity, and product offerings moving forward.

ENPH Will Remain Relevant For A Long Time To Come, Especially In The Burgeoning EV Market

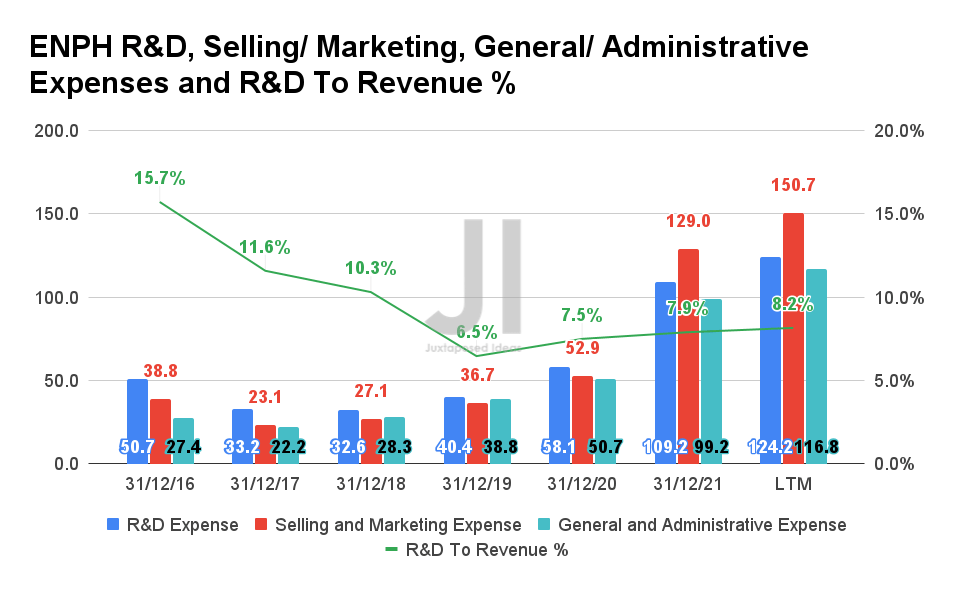

ENPH R&D, Selling/ Marketing, General/ Administrative Expenses, and R&D To Revenue % (S&P Capital IQ)

ENPH more than doubled its operating expenses in the past year, from $161.7M in FY2020 to $391.7M in the last twelve months (LTM). In addition, the company also sustained its R&D expenditures with regard to its annual revenues at an average of 7.86% in the past two years. Furthermore, ENPH also grew its microinverter contract manufacturing capacity by 28% YoY, from approximately 3.9M in FQ1’21 to over 5M in FQ1’22. As a result, we can naturally expect increased sales moving forward, since the company is also further expanding its capacity to nearly 6M quarterly by Q1’23.

Therefore, it is evident that ENPH is aggressively reinvesting into the business to expand its product offering and capacity, while remaining competitive in the global solar market, projected to grow from $197.2B in 2021 to $368.6B in 2030, at a CAGR of 7.2%. Furthermore, through the previous ClipperCreek acquisition, the company also aims to expand into other energy management products, such as EV chargers, which will remain highly relevant for a long time to come, since the global EV market is expected to grow from $163B in 2020 to $823.7B in 2030 at a CAGR of 18.2%.

With ENPH’s entry into one of the leading EV markets in the world, namely the EU, we can be assured of its massive growth moving forward. In 2021, the EU reported 14% of EVs market share for all new auto sales, in comparison to China at 9%, the US at 4%, and globally at 6%. In April 2022 alone, there were a total of 158.6K EVs sold in the EU, comprising 83.5K of BEVs and 75K of PHEVs. Though these numbers represent a 1% decline YoY, it is also important to note that the delivery of EVs in April was gated by supply instead of demand, given China’s Zero-COVID Policy and the ongoing semiconductor shortage globally. Since the EU reported BEV and PHEV sales of 423.25K in Q1’22, representing approximately 18.8% of total auto sales for the quarter, it is apparent that ENPH possesses a massive runway for growth in the rapidly developing EV market there.

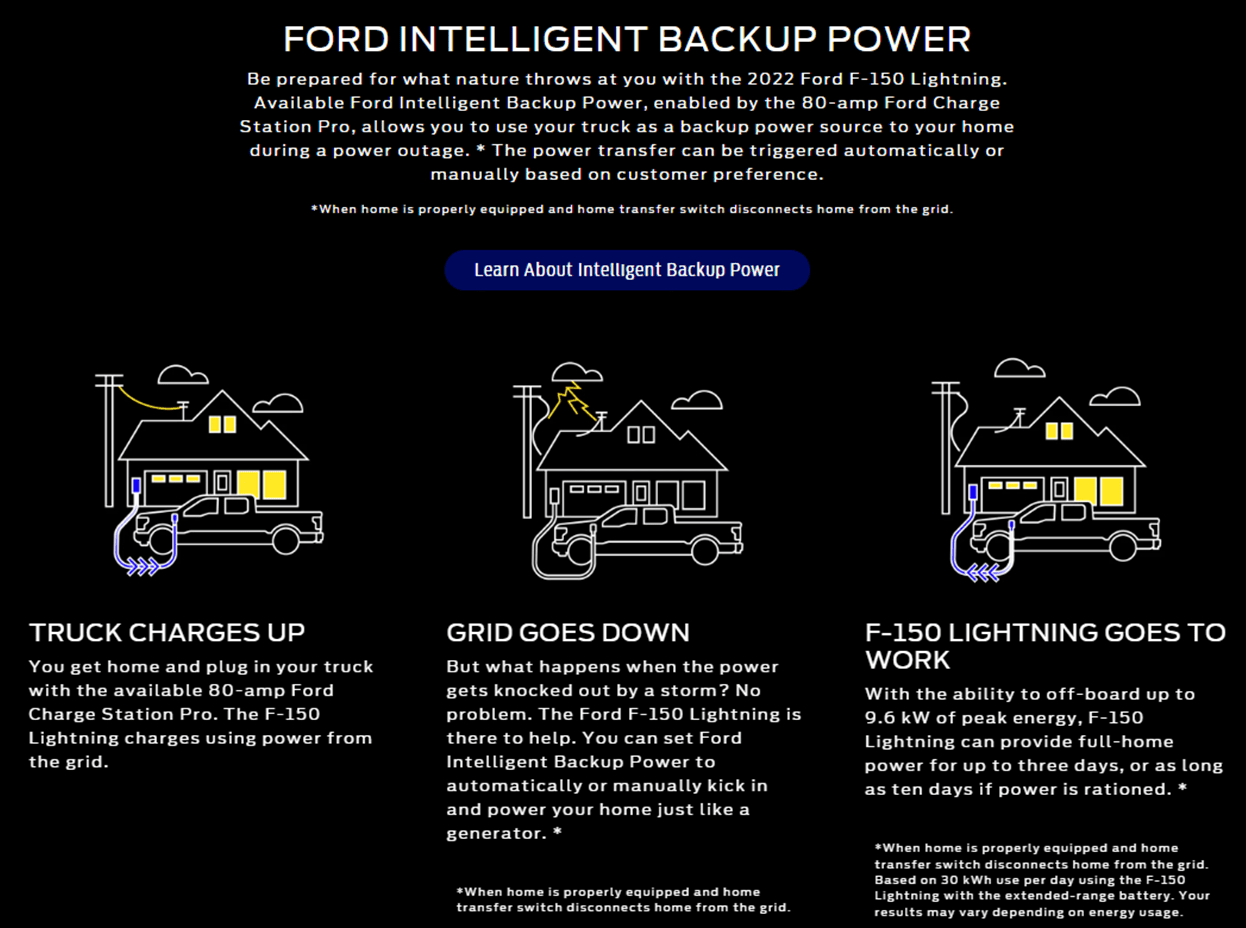

Ford Intelligent Backup Power (Ford)

Furthermore, assuming multiple partnerships with major automakers/ solar installers, such as Ford (F) and Sunrun Inc (RUN), we may expect rapid adoption in the US moving forward. Ford previously announced its partnership with Sunrun, the leading solar installation company in the US, in May 2021. ENPH also has had a long-standing partnership with Sunrun for its previous IQ7 Microinverters since November 2019. It is also interesting to note that Ford is among the first few automakers to offer a bi-directional charging option in the F-150 Lightning EV battery as a home backup energy source. It would be interesting to see how things develop moving forward, given that Ford has started deliveries for its EV truck.

As a result of increasing EV adoption, it is not far-fetched to picture a complete closed-loop solar panel system, featuring ENPH’s IQ8, reliable energy storage systems, home EV charging, and an EV capable of bi-directional charging, given the frequency and severity of natural disasters in the US in 2021. The reason why ENPH’s IQ8 Microinverters are critical here is that it provides backup power even in the absence of batteries, making restarting home energy systems possible after a prolonged grid outage. As a result, we are bullish about ENPH’s potential in the solar and EV market, given the massive possibilities in the future.

Though Tesla’s (TSLA) Powerwall could prove to be a strong adversary for ENPH, we do not expect many issues in the short term, given that the latter has a relatively smaller success for its solar segment, compared to its EV and energy segments. In addition, TSLA does not allow bi-directional charging and has been known to void warranties in the past. Nonetheless, we expect that ENPH would face temporary headwinds from the California NEM 3.0 and the federal tariffs on solar imports, though improvements seem possible, given the massive pressure from the solar industry. We shall see.

ENPH’s Long Runway For Growth

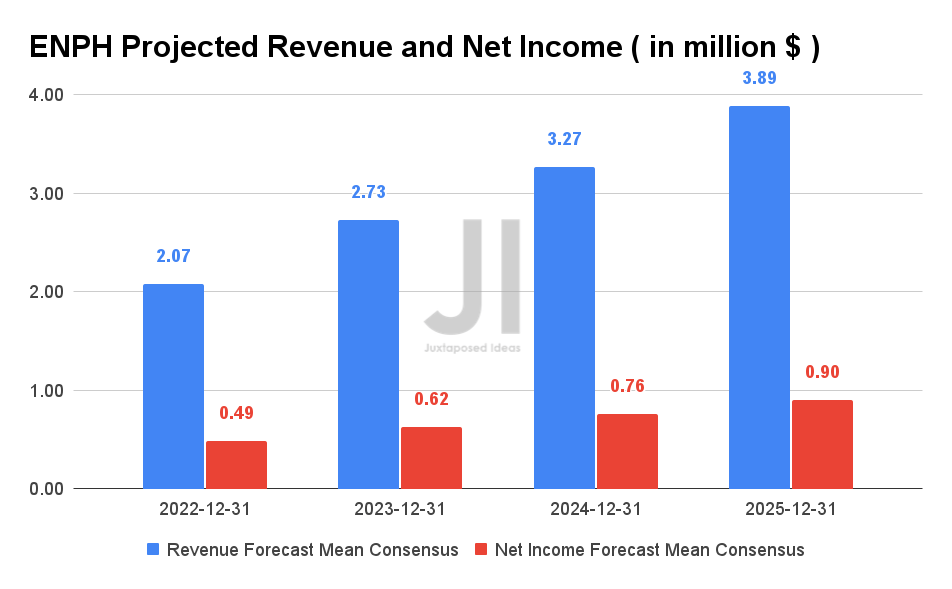

ENPH Projected Revenue and Net Income (S&P Capital IQ)

Since our previous analysis in March 2022, ENPH’s projected revenue growth has remained mostly in line, at a CAGR of 29.57% over the next four years. However, it is notable that the company is expected to grow its net income at an excellent CAGR of 59.23% over the same period of time. It is evident that consensus estimates are confident of the company’s capability in expanding its net income margin, from 10.5% in FY2021 to a projected 23.1% in FY2025.

In addition, ENPH is expected to report revenues of $2.07B and net income of $0.49B in FY2022, representing impressive YoY growth of 50% and 337.9%, respectively. Furthermore, the company guided FQ2’22 revenues of up to $520M with a sustained gross margin of up to 40%, representing an exceptional increase of revenue by 17.8% QoQ and 64.5% YoY.

As a result, it is evident that more have come to realize the strength of ENPH’s product offerings in the current macro issues, including the Ukraine war, rising gas/oil prices, and climbing utility bills. These have resulted in a surge of consumer demand for renewable energies for home use and EV charging, especially in the US and EU. Therefore, ENPH’s future looks very bright indeed.

In the meantime, we encourage you to read our previous article on ENPH, which would help you better understand its position and market opportunities.

- Enphase Energy: Massive Adoption Expected In The EU, Thanks To Russia

So, Is ENPH Stock A Buy, Sell, or Hold?

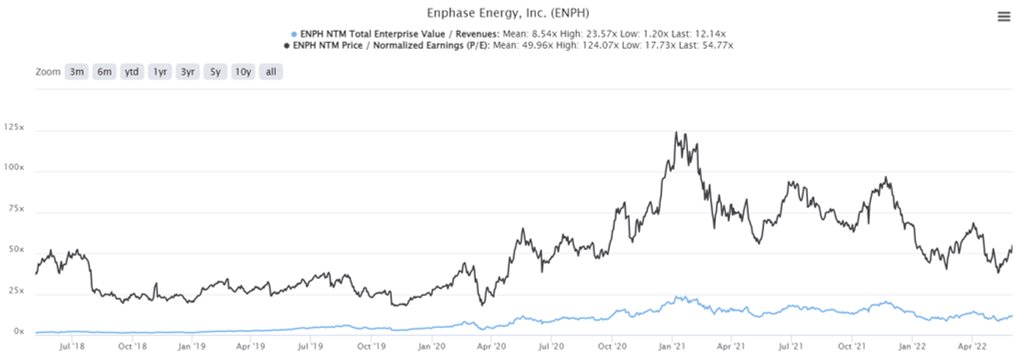

ENPH 5Y EV/Revenue and P/E Valuations (S&P Capital IQ)

ENPH is currently trading at an EV/NTM Revenue of 12.14x and NTM P/E of 54.77x, slightly higher than its 3Y mean of EV/Revenue of 10.88x and though lower than its 3Y mean of P/E of 56.96x, respectively. The stock is also trading at $198.93, down 29.5% from its 52-week high of $282.46, though at a premium of 75.4% from its 52-week low of $113.40. It is evident from the valuation and stock price charts that ENPH’s stock had grown tremendously during the COVID-19 pandemic in the past two years, with its P/E valuations rising almost threefold and stock price nearly fourfold, even after the drastic market correction in November 2021.

ENPH 5Y Stock Price (Seeking Alpha)

Given its massive potential in the clean energy market, consensus estimates also rate ENPH stock as a strong buy with a 20% upside to the price target of $238.83. Nonetheless, given the recent spike in mid-May 2022, ENPH stock is currently trading above its historical 50-day moving average of $178.17, giving interested investors a lesser margin of safety. As a result, we recommend patience while awaiting a deeper retracement before adding more exposure.

Therefore, we rate ENPH…

Read More: Enphase Stock: Smashing The EV Market, Patience Recommended For Now (NASDAQ:ENPH)

{kind=link}