jetcityimage

Tesla (NASDAQ:TSLA) investors have been richly rewarded over the last few years. But as a Tesla long, we often think about and ask others their biggest fears when it comes to Tesla’s future. The list typically includes Elon Musk’s temperament, his frequent rubs with the Securities and Exchange Commission [SEC], and distractions like Twitter (TWTR). All these are valid concerns, but not our top three.

Our three big worries

- Competitive Landscape

- Sustainability – How much is too much?

- Valuation – Multiple Compression

Competitive Landscape

Tesla has so far enjoyed the lion’s share of the market thanks to being the first car manufacturer to crack the code of producing a novel and niche product profitably in mass. Seeing Tesla’s own struggle with profitability and how close the company was to bankruptcy in Elon’s own words, it is easy to be complacent that nascent competitors like Rivian Automotive (RIVN) and others may soon burn out. But, Ford Motor Company (F) and General Motors Company (GM) are two of the players projected to overtake Tesla and their pockets are much deeper than the key competitors so far. They have the distribution network to go with more affordable pricing plans ($30,000 range) to make a serious dent. This article just published by Time.com highlights some of these risks. The one that caught our attention the most is:

“Tesla’s electric vehicle market share is likely to decline from about 70% in 2021 to the “low teens” by 2025 as a result of the onslaught of EVs coming from other manufacturers, predicts John Murphy, the managing director and lead auto analyst at Bank of America Merrill Lynch.“

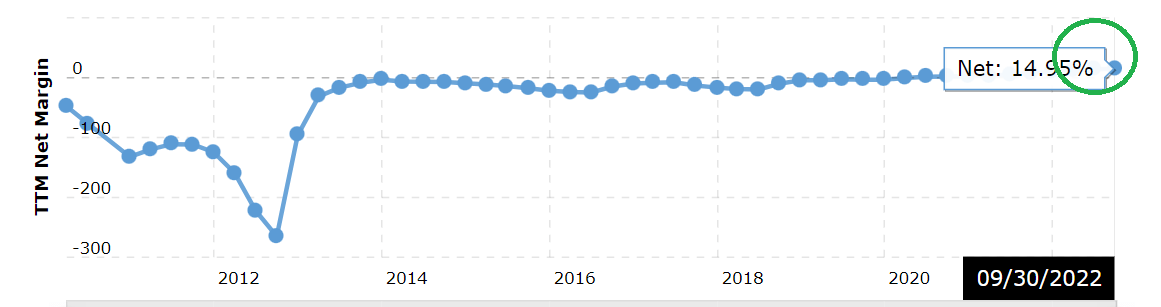

TSLA Profit Margin (www.macrotrends.net)

For the sake of simplicity, let’s assume the current EV market sells a total of 100 cars every year. Let’s assume Tesla’s average selling price is $50,000. With a 70% market share, that means Tesla generates $3.5 Million in revenue. With a profit margin of 15% [chart above], Tesla retains $525,000 in profit in this hypothetical market.

Since the global EV market is projected to grow at 24% per year, five years from now the EV market sells about 293 cars. If Tesla’s market share falls to “teens” as predicted, Tesla will be selling 55 cars. To reach the same $525,000 in profit, Tesla’s profit (in $) in the same hypothetical market falls by 22%.

To retain the same profit (in $) five years from now, Tesla’s profit margin should jump to 20%. This may seem within reach, but in a market with more competitors, the selling price is likely to be under pressure. Additionally, the prediction is for Tesla’s share to fall to “low” teens in three years, while the table below assumes the highest possible teen number in five years. Overall, the potential downside impact of a level playing field is clear.

Note: The table below is rounded off to not show decimals.

| Year | Market Size (In Units) | Selling Price | Tesla’s Share as % | Tesla’s Share in Units | Revenue | Profit % | Profit in $ |

| 2022 | 100 | $50,000 | 70% | 70 | $3,500,000 | 15% | $525,000 |

| 2023 | 124 | $50,000 | 46% | 56 | $2,821,000 | 15% | $423,150 |

| 2024 | 154 | $50,000 | 36% | 56 | $2,798,432 | 15% | $419,765 |

| 2025 | 191 | $50,000 | 29% | 56 | $2,776,045 | 15% | $416,407 |

| 2026 | 236 | $50,000 | 23% | 55 | $2,753,836 | 15% | $413,075 |

| 2027 | 293 | $50,000 | 19% | 55 | $2,731,805 | 15% | $409,771 |

Sustainability – How much is too much?

It is fair to say the market sees Elon as the face and brain of Tesla. Calls for the company to identify a number two has been floating around for too long. In fact, it may not be too farfetched to say Elon is the face of EVs. That’s great for the stock in the short to medium term, but how long can Elon power through 80+ hours a week? Apple (AAPL) is the closest comparison we can think of where a large, successful company was deemed to be a one-man show. As long term investors of Apple, we recall being worried about Apple’s ability to continue operating profitably post-Steve Jobs. But in hindsight, Apple differed from present day Tesla in many ways:

- Apple was enormously profitable and was already the most valuable company in the world when Jobs passed.

- If anything, Apple was largely undervalued, as opposed to Tesla’s lofty valuation.

- Jobs had Bill Gates as a well-respected contemporary almost from the get-go. Anyone with any sort of interest in Apple would have also named Steve Wozniak as a key, if not the key player. We’d bet more than half of the readers of this article will struggle to name someone significant at Tesla other than Elon.

- Even at the peak of his career, Jobs was the CEO of “just” two large (granted, public) companies at the same time, and he immersed himself fully at both. Outside of Tesla and SpaceX, Musk’s interest in Neuralink, OpenAI and recently Twitter are well documented. Although SpaceX is still private, it is valued at $127 Billion, which would place it in the top 60 largest companies in the US Stock Market.

- Last, acknowledging hindsight bias, we don’t believe Jobs was ever the poster child of computers in general as much as Musk is for EVs.

To be clear, the Twitter distraction by and of itself is not a problem. But Elon’s pattern of doing too many things as the poster child is a valid concern for Tesla investors, especially as he is now officially a quinquagenarian.

Valuation – Multiple Compression

Investopedia defines Multiple Compression as:

“Multiple compression is an effect that occurs when a company’s earnings increase, but its stock price does not move in response.“

In simpler words, Mr. Market has already rewarded the stock for future earnings and promises. And simply meeting the promised numbers or even slightly beating it won’t help the stock as much as it did in the past. Don’t believe this will happen to Tesla? Just ask Cisco (CSCO) and Intel (INTC) investors from the dot com days. Those two companies are hands down more profitable now than they ever were during the most profitable days for the stock. Granted, there is no guarantee that Tesla may face all the problems Intel and Cisco did, but there is also no guarantee that Tesla will not face similar or stiffer competition.

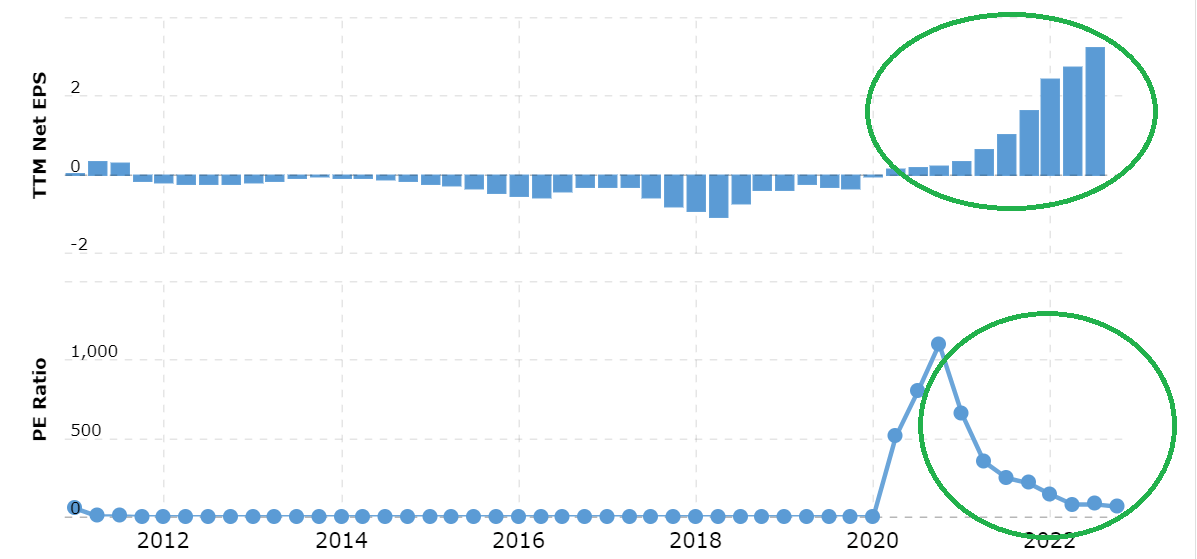

Still not convinced? Take a look at Tesla’s own charts below. Notice how the increasing earnings are starting to coincide with declining PE multiple. You can safely ignore the points where PEs were above 500, but the trend is still very evident. The larger point is, even if you believe there is no multiple compression yet, it is a question of when and not if.

TSLA EPS vs PE (macrotrends.net)

According to Yahoo Finance (and dozens of analysts),

- Tesla is expected to grow at more than 50% per year for the next five years.

- Current forward EPS estimate is $4.31.

- That gives Tesla a forward multiple of about 50 as it is trading at $215.

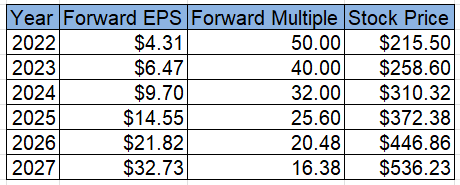

Let’s use those 3 numbers and our assumed multiple compression factor. Even if Tesla grows at the expected 50%, the market is not going to keep awarding a multiple of 50. So, let’s say the multiple drops by 20% each year. How will Tesla’s stock price look in five years from now? A pretty impressive $536 as shown below. In other words, a two and a half-fold increase. If you believe 20% compression is too far too soon, feel free to plug in your own number. But keep in mind during the current market selloff, many stocks got their multiples slashed by as much and more than 80%. Not to mention, in this scenario, EPS should octuple from about $4 to $32. So any unreasonableness in the 20% multiple slash is compensated by the generous 50%/yr EPS increase. Overall, a lot of things need to go right for this scenario to pan out.

TSLA at 20% PE Compression (Author)

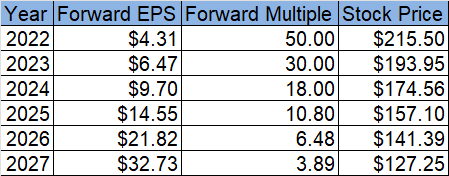

If you believe 20% annual compression is too less, then the table below is for you at 40% compression. Things are starting to look funny on the other side now, meaning too low a valuation. There is no way a company like Tesla is going to trade at 4 times earnings in the next five years.

TSLA at 40% PE Compression (Author)

Both the scenarios above assume that earnings still grow at 50% every single year for the next five years. Once again, we are talking about a nearly 8-fold increase in EPS in five years, which is too aggressive in our opinion and ignores competitive and economic challenges that apply more to companies like Tesla, which is still in an aggressive growth phase, than to established companies.

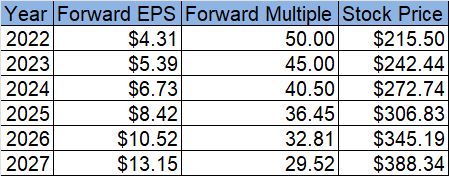

What if we use the “middle road” numbers and assumptions here. Let’s say Tesla manages “just” 25% increase YoY for the next five years and the market continues rewarding it with a premium multiple, but one that goes down by 10% each year. That gives Tesla a five-year price target of $388, which is an impressive 80% return overall compounded at 12% every year for five years. We will be glad about this return here on because the assumptions are moderately aggressive (25% earnings growth is still aggressive but within reach) while acknowledging that Mr. Market may not retain the lofty multiple. Tesla is right now trading at a multiple that will net satisfactory returns under the moderate assumptions above. This also aligns fairly well with our recommendation to consider buying Tesla at $200.

TSLA Mid Scenario (Author)

Conclusion

We’ve held Tesla profitably as an investment as well as made short-term trading gains on weaknesses. But we believe Tesla’s risks are real on all three fronts: competition, sustainability, and valuation. Tesla is still a Growth at Reasonable Price [GARP] stock for us, but the key word there is “reasonable”. What is reasonable is up to each individual. For us, a reasonable assumption is Elon being at the helm for at least a decade more. Reasonable is a forward multiple that is at best twice that of the market. Reasonable is buying a GARP stock at a PEG of 1, which is around $204 based on current forward estimates. In the present market conditions, Tesla at $200 or below is reasonable for us given our risk-reward appetite. But we are aware of the risks and acknowledge them. Do you?

Read More: Tesla Stock: Top 3 Worries As A Long (NASDAQ:TSLA)

{kind=link}