Editor’s note: Seeking Alpha is proud to welcome Mario Silva as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Justin Sullivan/Getty Images News

There is a very good opportunity to buy Amadeus IT Group (OTCPK:AMADF)(OTCPK:AMADY) at the current price. The stock fits well with the “buy and hold” strategy used by Warren Buffett when he bought Coca-Cola (KO), Apple (AAPL), and American Express (AXP). He did that when these companies faced a “temporary setback” that pushed their stock prices down temporarily. Amadeus could be a similar situation for long-term investors, and I’ve used the different rules established by the “Oracle of Omaha” to see if the odds are in our favor. Let’s see why this stock is a long-term opportunity.

Background

Amadeus, with headquarters in Madrid, Spain, was founded in 1987 by Air France, Iberia, and Scandinavian Airlines Systems. It is the biggest player worldwide that has a huge network that connects travel agencies and tour operators with airline companies, rental cars, hotels, and cruise lines. The company has developed other technological services that have a greater amount of digitalization and more efficiency within the travel and tourism sector. Amadeus is a leader in terms of its two business lines: distribution and IT solutions. As of 2022, the company has more than 40% market share of the world market in distribution, an increase from 36.7% in 2010. The company’s other competitors are Sabre (SABR) and Travelport, with the latter having more exposure to the U.S., and Sabre being the second largest airline distributor in the industry after Amadeus.

First Buffett rule – industry recovering gradually (a “temporary setback”)

Before COVID, according to the International Air Transport Association (IATA), the number of air travelers was expected to double in 20 years across the world, reaching 8.2 billion people traveling. That’s an increase of 3.5% compound annual growth rate (CAGR) since 2019. During COVID, the industry was significantly impacted and, as such, new estimates for the short term were required, although the long-term estimates should not change materially. IATA estimates that the number of travelers could reach 4 billion in 2024, surpassing pre-COVID levels and rising to 103% of the 2019 levels.

In February 2022, the IATA provided a new update for the next five years:

-

In 2021, overall traveler numbers were 47% of 2019 levels; this is expected to improve to 83% in 2022, 94% in 2023, 103% in 2024, and 111% in 2025.

-

In 2021, international traveler numbers were 27% of 2019; this is expected to improve to 69% in 2022, 82% in 2023, 92% in 2024, and 101% in 2025.

In other words, most of the travel and tourism sector is expected to recover its pre-COVID levels in 2024.

Again, as per IATA:

The biggest and most immediate drivers of passenger numbers are the restrictions that governments place on travel. Fortunately, more governments have understood that travel restrictions have little to no long-term impact on the spread of a virus. And the economic and social hardship caused for very limited benefit is simply no longer acceptable in a growing number of markets. As a result, the progressive removal of restrictions is giving a much-needed boost to the prospects for travel.

Business Model

Among its main services the company offers technological services and platforms for distribution for travel agencies and tour operators, connecting them with travel providers such as airline companies, hotel chains, cruise lines, and rental cars. To fulfill this goal, and as part of the distribution business line, Amadeus offers the Global Distribution System (GDS). That is a platform of networks containing travel-related information such as schedules, fares, and related services that also enables automated travel-related transactions between travel providers and travel agents.

Another type of distribution offered by Amadeus is the New Distribution Capability (NDC), which enables the airline companies to share information and sell their own products and services directly to the travel agencies, corporations, and passengers without the need of the GDS services. Using the NDC, the airline companies have much better flexibility to launch more personalized promotions to differentiate its services from those of the competitors, marketing products more quickly than traditional distribution channels, like the GDS, and responding faster to the possible shifts in consumer trends.

Amadeus has another business line: IT solutions. The company offers a wide range of technological services to its different customers. One example of these kind of services is the supply of technological management systems for airlines companies to manage their prices according to the season, helping them in maximizing their efficiency and profits. There are other value-added services such as the customer experience enhancement, data integration, consulting services, support for passenger processing, and so on.

Taking both business lines together, the company is providing solutions to 474 airline companies, 132 airline operators, 29 cruise and ferry lines, 133 ground handlers, more than 1 million hospitality providers and hotels, 21 insurance provider groups, and 90 rail operators, as well as corporations, travelers, business travel agencies, online travel agencies, and retail travel agencies.

Revenue Breakdown

The evolution of the different business lines in the last five years indicates that the IT solutions business line is opening up new possibilities for future growth, offering more value-added technological services with higher margins. Revenues from the IT solutions business have been increasing in the last few years:

Amadeus Annual Report

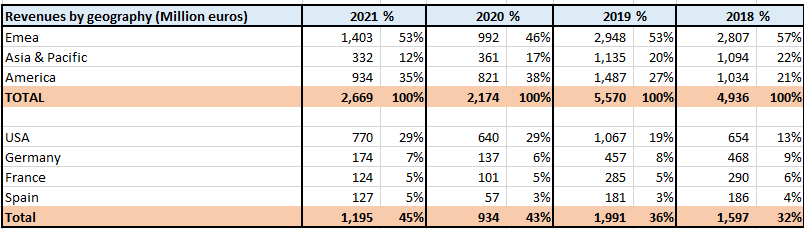

In terms of geographical diversification, Amadeus is well-diversified and is seeing increasing participation in America post-COVID in 2020. On the other hand, the U.S. is the country with the highest participation individually in the total revenues of the company. In the following table, we see the participation by geography and the participation of the top four countries with the largest portion of the pie:

Amadeus Annual Report

Second Buffett rule – excellent, shareholder-oriented management

Luis Maroto, CEO of Amadeus, has been working at the company for more than 20 years. Maroto has successfully led all of the acquisitions made by the company in the last 10 years. One example is the acquisition in 2018 of Travelclick, which is a hotel technology company that offers business intelligence and operational services. This acquisition enabled Amadeus to reinforce its hospitality solutions business, which has been another source of cash generation for the company in the last years. Amadeus paid $1.52 billion, a price that was only three times Travelclick’s revenues in 2017 of $373 million, and 17 times its EBITDA in the same year.

To put things in perspective, Adobe Systems (ADBE) recently paid more than 50 times sales for FIGMA, a subsidiary that is expected to have revenues of $400 million in 2022. The multiples paid for Travelclick shows that Amadeus’ management doesn’t like to overpay for acquisitions.

Also, Maroto has been responsible for the launch of the NDC as a response to a challenge issued by the IATA. In 2015, the IATA decided to launch its NDC to support airline companies with respect to avoiding a total reliance on the Amadeus GDS platform. In response to that challenge, Amadeus launched its own NDC platform to offer another alternative to the airline companies. As of 2021, Amadeus has signed up more than 20 airline companies for its NDC platform; in this way, Amadeus offers a wider range of services with its GDS and NDC. Maroto turned a threat into an advantage, since the NDC was launched by the IATA as a potential substitute for the Amadeus GDS, and now Amadeus offers interesting complementary services with both its GDS and NDC.

Maroto seems to have prepared Amadeus for the very long term given that he wanted to protect the business from the entrance of the big U.S. tech companies into the industry. In this way, Amadeus has signed very long-term contracts with airline companies and other players within the travel and tourism sector to reinforce its long-term relationship with them. Integrating Amadeus’ systems with those from its clients makes it very difficult for potential powerful competitors to disrupt Amadeus’ technological services.

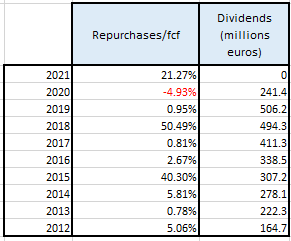

In regard to capital deployment, management has not been consistent in its repurchases of its own shares since it prioritizes its investments in growing organically and through acquisitions, without taking on much debt. Furthermore, management has shown a higher ratio of repurchases/FCF when the stock dropped significantly in 2018 due to the trade war between U.S. and China, and in 2021 due to COVID. This indicates that management does not like to overpay for its repurchases, unlike many other companies.

Since 2013, the company has made very important acquisitions that have reinforced its leadership position in the industry – including Travelclick in 2018, Premier Inn in 2017, Itesso in 2015, IHG in 2014, etc. On the other hand, the company stopped paying dividends in 2020 and 2021 in order to accumulate more liquidity due to COVID. However, the company has announced that it will pay dividends again in 2023. In the last 10 years, before COVID, the dividend yield was between 1% and 2% and grew year-on-year from 2012 to 2019:

Amadeus Annual Report

Third Buffett rule – strong competitive advantages relative to its…

Read More: Amadeus: A Great Stock In Travel And Tourism (OTCMKTS:AMADF)

{kind=link}