William_Potter/iStock via Getty Images

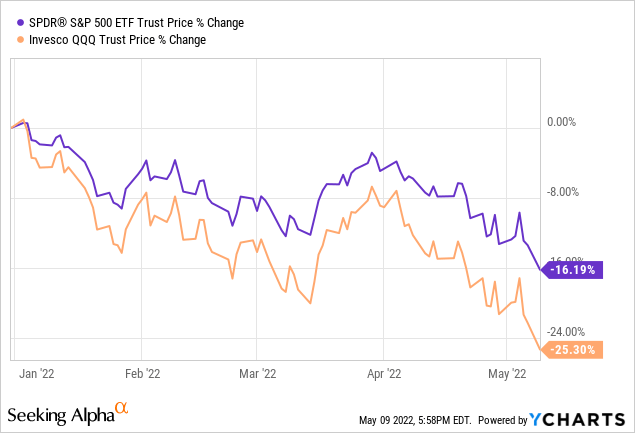

Fears of a recession are soaring, pushing stock prices and bond yields lower. Public figures ranging from Bill Gates to billionaire Leon Cooperman have recently signaled that a global recession may be on the way in short order. In fact, the United States might already be there given that GDP shrank in Q1 and China is certainly reeling from its aggressive COVID-19 lockdowns in highly productive cities such as Shanghai.

As a result, the stock market has been in panic mode lately, with the S&P 500 (SPY) and Nasdaq (QQQ) getting pummeled:

Whether or not we actually slide into recession is not something we are prepared to take a position on as we generally refrain from making macroeconomic predictions. However, we do believe that the market appears to be overly pessimistic on certain stocks.

In particular, we are bullish on triple net lease REIT STORE Capital Corporation (NYSE:STOR), as we believe it offers bond-like income through recessionary periods, while also providing greater yield and growth than bonds.

Bond-Like Income Security

While bonds are obviously generally very secure sources of income due to their seniority in the capital stack, we believe STOR’s dividend payout is almost as safe.

First and foremost, STOR’s dividend payout did not suffer a cut despite its business model being tested severely during the COVID-19 lockdowns. In fact, the REIT continued to grow its dividend at a mid-single-digit (4.4%) pace during 2020 and has since accelerated that growth rate to 4.9% in 2021. It is expected to grow at 6.2% in 2022. If STOR could grow its dividend at a more than token rate in 2020, it will likely take a very severe depression to force STOR to cut its dividend.

Another evidence for the safety of STOR’s dividend is the performance of peer REITs like Realty Income (O) and National Retail Properties (NNN) during the Great Recession. In 2008, O grew its dividend by 6.5%, and in 2009 it grew its dividend by 2.7%. In 2010 and 2011, it grew its dividend by 0.9% each year before the company saw dividend growth accelerate in the years following. NNN, meanwhile, grew its dividend by 5.7% in 2008, in 2009 it grew its dividend by 1.4%, and in 2010 and 2011 it grew its dividend by 0.7% and 1.3%, respectively, before the company saw dividend growth accelerate in the years following. If similarly structured REITs with weaker balance sheets at the time than STOR has today could sustain their dividend growth during those extremely lean periods, we have confidence that STOR could do so today as well.

A big reason why these investment grade triple net lease REITs held up so well during the Great Recession and COVID-19 lockdowns, and will likely do so again, is due to their conservative business models. STOR benefits from immense diversification with 573 customers spread across 121 industries. Its top customer contributes only 3% of its total base rent, and its top 10 customers only contribute a combined 18% of its total base rent.

Additionally, the leases are senior in the obligation stack, so companies essentially have to go bankrupt before they break their leases, and – with 4.7x rent coverage – it is highly unlikely that a large percentage of STOR’s tenants will default during a downturn.

Finally, these leases are set for lengthy terms, with the weighted average lease term on new investments at 17 years.

With an investment-grade balance sheet that affords STOR plenty of financial flexibility and a dividend payout ratio for 2022 expected to come in at just 71.5%, on top of the very conservative business model, the dividend looks very safe.

Higher Yield Than Bonds

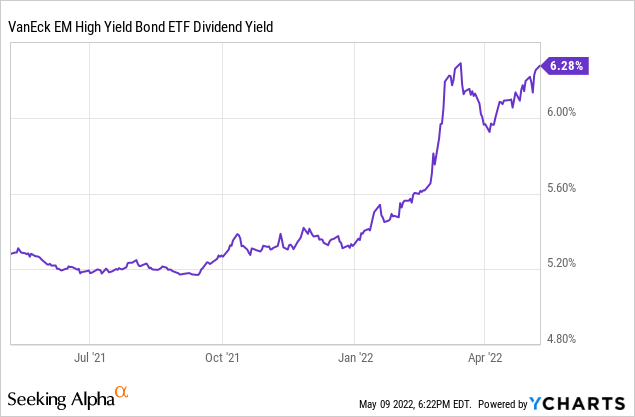

On top of the income safety afforded by STOR, its yield is also very attractive at 6%. This yield puts it on par with that offered by an emerging markets junk bond index fund (GBFAX):

From a risk perspective, we feel much more confident in the safety of a well-diversified portfolio of U.S. commercial real estate with the additional safety components afforded by the triple net lease structure and an investment-grade balance sheet than we do in emerging market junk bonds. Yet, today you can get a similar yield by purchasing shares of STOR as you would by investing in emerging market junk bonds.

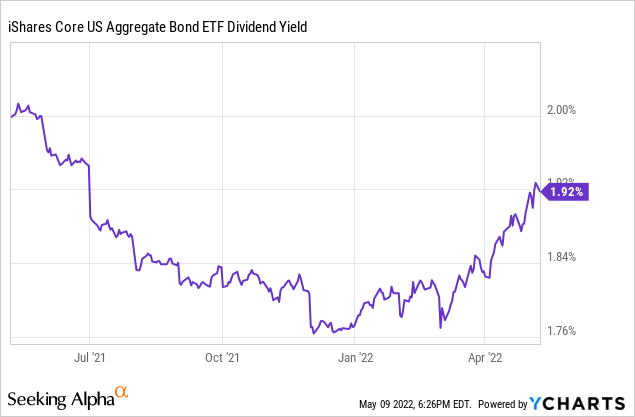

When comparing to U.S. bonds, the yield gap becomes quite stark:

Greater Growth Than Bonds

Last, but not least, not only is STOR’s income stream bond-like and its current yield on par with or superior to most bond funds, but its growth potential is vastly superior. While bonds offer zero growth potential, STOR has grown its dividend per share at a 5.9% CAGR thus far and expects to continue generating mid-single digit annualized growth for the foreseeable future. As a result, its value proposition as a recession-proof high yielder looks even more valuable, especially when compared to bonds.

Investor Takeaway

While the market is in panic mode over the rising risk of recession, it appears to be irrationally throwing out recession-proof dividend growth stocks at increasingly attractive prices.

While some retirees may panic and buy bonds for income to ride out the storm, they might want to consider STOR instead. With a proven battle-tested business model and real estate portfolio, a very attractive current yield, and solid growth momentum that should help mitigate some of the negative impacts of inflation on purchasing power, STOR is an ideal bond substitute during these stagflationary times.

Read More: Our Top Pick For Stagflation: STORE Capital Stock (NYSE:STOR)

{kind=link}