MAGNIFIER/iStock via Getty Images

Investing In Shipping Company Stock In 2022

Asia-U.S. shipping indexes are down approximately 20% to 30% from their peaks due to lockdowns in China and port congestion. There’s a ton of pent-up demand for dry bulk and maritime shipping, and consumers are absorbing price increases given the high amounts of inventory at ports.

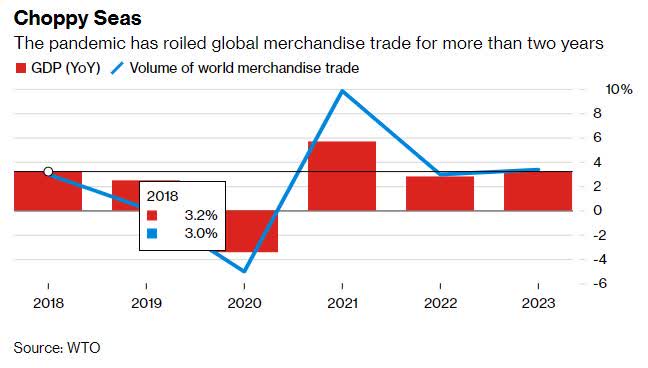

GDP to Volume of World Merchandise Trade (WTO)

Because supply chain disruptions and the backlog have to work themselves out on the heels of the limited supply of vessels, we believe shipping stocks are a buying opportunity.

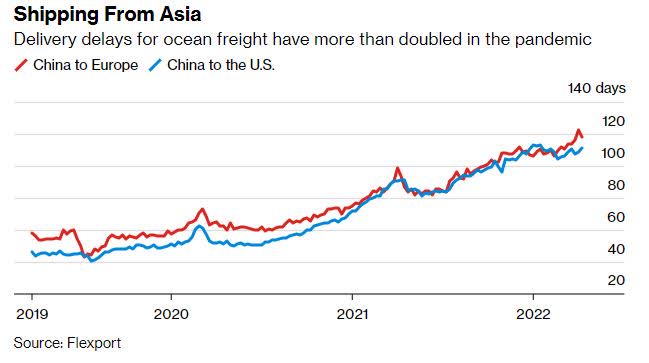

The global shipping crisis will take a while to work out, primarily when the world’s second-largest economy, China, whose abysmal healthcare is resulting in extended lockdowns. While delivery delays for ocean freight have substantially increased since the pandemic, continued lockdowns in Asia as countries cannot support the outbreaks, and the backlogs and shipping demand will continue to serve as core growth drivers for shipping companies going forward. Hence, this growth, combined with incredible valuation frameworks, provide an excellent opportunity to buy these stocks.

Shipping from Asia Delivery Times (Flexport)

Shipping Companies Are Setting Sail for A Rally

Shipping companies are price makers. Not only are GOGL, ZIM, and SBLK deep value stocks with excellent growth potential, the current environment should increase their revenue. Shipping companies can pass along costs to consumers, and the companies in need of goods will pay whatever it costs, including higher fuel prices, to receive their goods. It’s also why inflation will persist at high levels because the logjam will take a long time to work out, and therefore, prices will stay high. The Fed cannot fix supply chain disruptions prompted by a pandemic-related shutdown in China, the world’s second-largest economy, or resolve the supply chain disruptions from the war in Ukraine. Federal Reserve monetary policy and U.S. interest rates will do nothing to tame these issues. While the U.S. may see domestic demand curtailed due to a decrease in consumer spending, people still have to eat. When you have shortages of grain and other non-agricultural products, it’s going to take a long time to work that through the system, and therefore, shipping stocks stand to see superior growth potential in the future compared to average stocks.

“The change in Covid prevention policies in different cities has imposed an extraordinarily severe impact on logistics,” said Cui Dongshu, Secretary-General of the China Passenger Car Association. According to Bloomberg Shipping data, 230 cargo carriers off the coast of China are gridlocked, an increase of 35% from last year, with imported containers in Shanghai waiting an average of 12.1 days for pickup. And while a wave of imports is creating more backlogs in ports around Europe and the United States, inter shipping and delivery logistics are top of mind for nations searching for faster routes to offload containers and store inventory. While these “issues” may seem problematic, the three stocks we’re mentioning in this article are set to benefit, especially in this inflationary environment.

Golden Ocean Group Limited (NASDAQ:GOGL)

-

Market Capitalization: $2.77B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 5/17): 6 out of 583

-

Quant Industry Ranking (as of 5/17): 4 out of 25

Headquartered in Bermuda, dry bulk shipping company Golden Ocean Group Limited (GOGL) operates and transports vessels that contain bulk commodities like ores, coal, grains, and fertilizers. On a longer-term upward trend, GOGL has stellar momentum, giving investors a reason to continue actively purchasing shares, which is driving the stock’s price higher. Year-to-date, the stock is +56.12%. The company’s quarterly price performance below shows that GOGL outperforms its sector peers by two, three, and four times. In addition to excellent momentum, GOGL comes at a severe discount.

GOGL Momentum (Seeking Alpha Premium)

GOGL Valuation

This stock has an incredible valuation framework. With an A+ valuation grade, GOGL’s current P/E ratio of 5.97x is 64% below its sector peers. On a forward P/E basis, it also trades at a 75% discount to its 5-year historical average. The stock also showcases an excellent EV/EBITDA (TTM) of 6.31x and nearly 40% below its peers with a Price/Book (TTM) ratio of 1.53x.

GOGL Valuation Grade (Seeking Alpha Premium)

If the company’s price point is not enough to convince investors, let’s look at Golden Ocean Group’s growth and profitability.

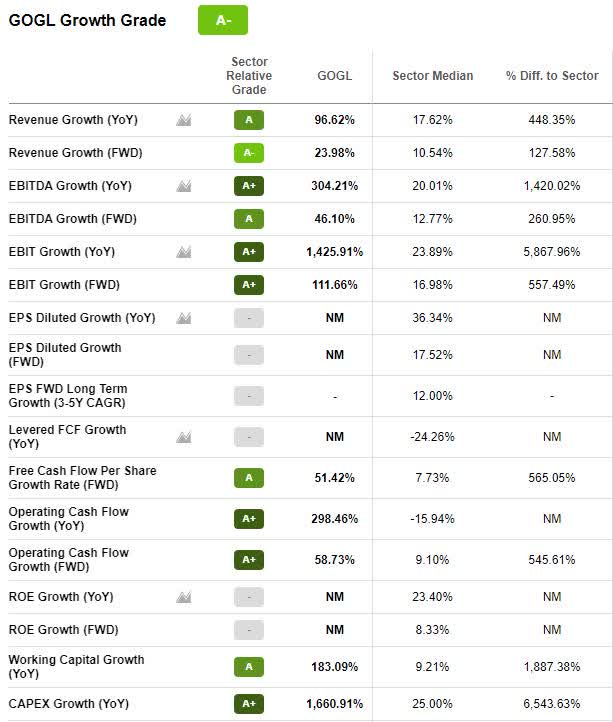

GOGL Growth And Profitability

Golden Ocean is experiencing tremendous growth, with tailwinds from increasing freight rates and expectations of dry bulk fleet demand outpacing its supply. For four consecutive quarters, GOGL has beat both top-and bottom-line earnings, with the most recent resulting in 4 FY1 Up revisions and an A- Revisions Grade. EPS of $0.98 beat by $0.15, and revenue of $312.87M beat by $15.34M, an increase of 148.69% year-over-year.

GOGL Growth Grade (Seeking Alpha Premium)

“We recorded an EBITDA just above $240 million, which translated into a net income of $204 million or $1.02 per share. This is the best quarterly result in the history of Golden Ocean…Iron ore prices are firming, demand from plants is also supporting while the energy crisis means demand for coal remains elevated. So, we remain very bullish for what lies ahead…we continue to pay out a significant portion of our net profit in dividend and that the supply and demand fundamentals remain in place for a sustained period of profitable markets” –Ulrik Andersen, GOGL CEO.

With its robust balance sheet and severely discounted valuation, GOGL is sitting pretty. Continued dry bulk demand and delivery logistics exceed supplies, benefiting shipping companies. Because Golden Ocean is a major coal and iron ore shipper, distant countries like South Africa and Australia, feeling the adverse effects of port jams, are in need. Those nations moving away from Russian supplies are also creating outsourcing opportunities for Golden Ocean’s Capesize and Panamax fleets, reporting rates between $29,635 and $39,304 per day. In the words of fellow Seeking Alpha Contributor Pearl Gray Equity Research:

“This stock is a tremendously well-placed value play. Golden Ocean illustrates tremendous efficiency with its Panamax and Capsize vessels carrying essential dry bulk in the coal and iron ore space. I think Golden Ocean’s gross margins illustrate its robust market position via economies of scale, which allows the stock to be a potential “best-in-class” pick in the current inflationary environment.”

We believe our next stock pick is in a great position as well.

ZIM Integrated Shipping Services Ltd. (NYSE:ZIM)

-

Market Capitalization: $7.62B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 5/17): 7 out of 583

-

Quant Industry Ranking (as of 5/17): 5 out of 25

Like GOGL, ZIM Integrated Shipping Services Ltd. (ZIM) is on a longer-term uptrend with a comparative strength that outperforms the S&P 500 by more than 80% over the last year.

ZIM vs. S&P 500 1-year price performance (Seeking Alpha Premium)

With its subsidiaries, ZIM provides container shipping and port-to-port transportation services, which bodes well for this company, given that container shipping rates are sky-high, with global spot rates more than quadruple pre-pandemic levels. And while rates are beginning to come down, ZIM continues to have stellar A+ Momentum, with the stock’s quarterly price performance substantially outperforming its peers.

ZIM Momentum Grade (Seeking Alpha Premium)

The stock is up 18% YTD and is trading below $70 per share. With a valuation in single-digit multiples, a Forward A+ P/E ratio of 1.8x, nearly 90% better than its sector peers, PEG GAAP (TTM) -99.34%, investors better add this stock at its current valuation fast before this ship sails!

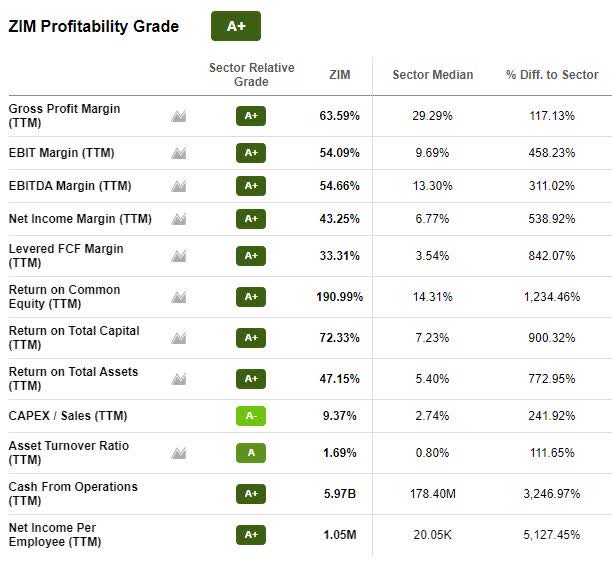

ZIM Growth And Profitability

In addition to the tailwinds outlined above, ZIM has stellar growth and profitability, translating into an excellent dividend yield to keep shareholders happy. Following another stellar earnings announcement, ZIM declared a $17/share dividend plus November’s $2.50/share dividend from November 2021, for a total annual dividend of $19.50.

After reporting record full-year and Q4 2021 results, Yair Seroussi, ZIM Board of Directors Chairman stated,

“2021 was a transformative year for ZIM. We kicked off the year with listing our shares on the world’s leading capital market in New York and have not looked back since. The many accomplishments of the past year and our remarkable performance, both financially and operationally, are the direct outcome of the unrivaled execution of our talented and dedicated management team and employees around the world, supported by the Board. In 2021, we took important steps to best position ZIM for long-term enduring growth and value creation for our shareholders. We remain focused on maintaining our strong execution and agility in 2022 and beyond, while advancing the highest standards of corporate governance and responsibility.”

ZIM Profitability (Seeking Alpha Premium)

Consistent with ZIM’s focus on profitability, shareholder’s equity increased to $4.6B, the full-year 2021 EBITDA margins were 61%, and the company continues to outperform freightliners’ industry averages. In addition to stellar profitability, the company’s EPS of $14.16 beat by $0.96 and revenue of $3.47B beat by $101.23M. With significant cash on hand and investment into equipment to continue its best-in-class growth, ZIM is a top shipping stock to keep in mind, along with our next carrier, Star Bulk.

Star Bulk Carriers Corp. (NASDAQ:SBLK)

-

Market Capitalization: $3.07B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 5/17): 9 out of 583

-

Quant Industry Ranking (as of 5/17): 7 out of 25

Star Bulk Carriers Corp. (SBLK), the global cargo shipping company that…

Read More: 3 Best Shipping Stocks: Inter shipping

{kind=link}