PonyWang/E+ via Getty Images

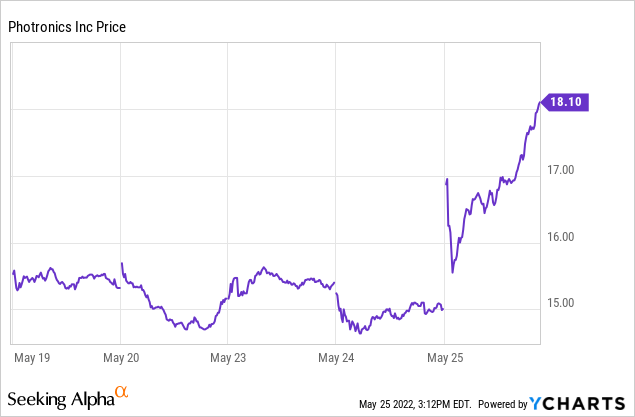

Photronics (NASDAQ:PLAB), a global leader in semiconductor masks and flat-panel displays, released a very strong Q2 EPS report this morning (Wednesday, May 25th) that was a big beat on both the top- and bottom line. Not surprisingly, the stock responded very positively and has rallied sharply today (see graphic below). However, despite a big move higher, PLAB still represents excellent value in my opinion. That’s because the company is performing even better than expected, has increased forward guidance, is cash rich, and has signed some favorable long-term supply contracts. PLAB is a BUY.

Investment Thesis

Photronics was founded in Connecticut in 1969 and has evolved into a global leader in photomask manufacturing technology. The company has 11 facilities across North America, Asia, and Europe. Photronics is also a leading manufacturer of flat-panel displays (“FPDs”) – both LCDs and AMOLEDs. “AMOLED” stands for “Active Matrix Organic Light Emitting Diodes”.

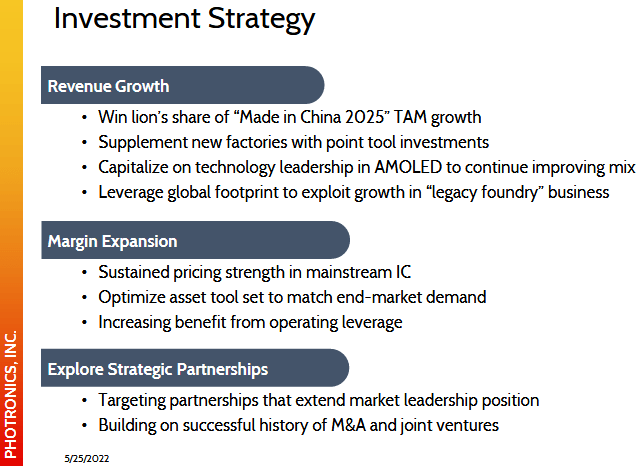

Photronics’ growth strategy currently revolves around two brand-new facilities in China in order to win the “lion’s share” of the “Made In China 2025” initiative:

Photronics

However, note that it isn’t just about increasing revenue – it’s about margin expansion and building strategic partnerships for the future.

And before American investors get upset about PLAB doing business in China, note that PLAB’s technology is not especially rocket science – and nowhere near delivering top-tier semiconductor manufacturing technology like that from the likes of Applied Materials (AMAT) or Lam Research (LRCX). That being the case, I find it highly doubtful that PLAB would come under any kind of “critical technology” government sanctions, although these days I suppose it is possible.

So let’s see how Photronics is performing on its business strategy.

Earnings

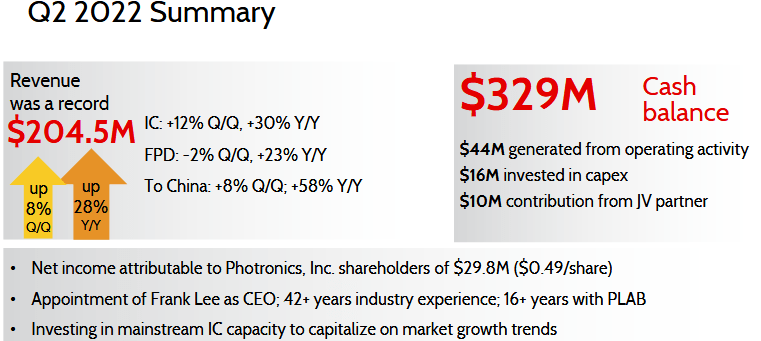

As mentioned previously, the Q2 EPS report was a home run and a beat on both the top (by $12 million) and bottom-lines (by $0.14/share):

Photronics

As shown in the graphic above, both of PLAB’s operating segments (IC and FPD) exhibited strong yoy revenue growth while overall revenue growth in China was up a whopping 58% year-over-year.

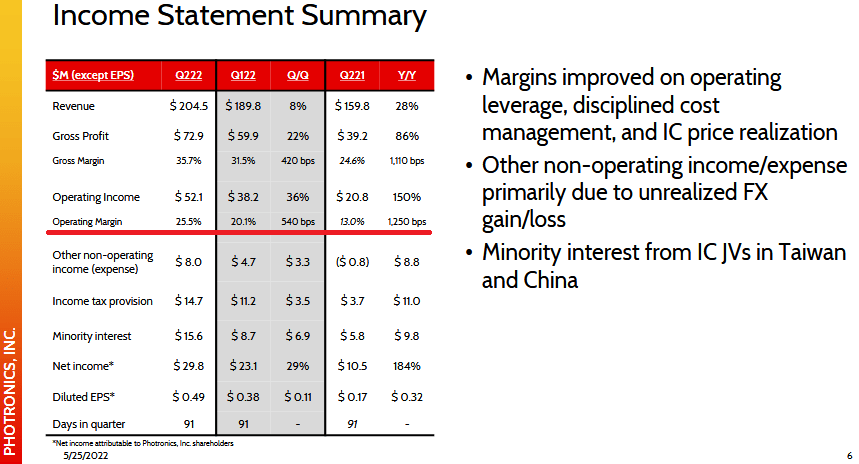

Net income zoomed to $0.49/share – almost triple the $0.17/share in Q2 of last year. That is because operating margin for the quarter was 25.5% – up from 20.1% on a sequential basis, and up a whopping 12.5 percentage points year-over-year:

Photronics

The quarter was driven by strong demand, increased price realization across the IC segment, and continued ramp-up of PLAB’s new production facilities in Xiamen and Hefei.

Photronics ended the quarter with $329.3 million in cash and long-term debt of only $89.4 million. That equates to a net-cash balance of an estimated $3.93/share based on 61.1 million average fully diluted shares at quarter’s end. That’s up significantly from the estimated $2.66/share in cash I reported in my first article on PLAB in January (see Undervalued Photronics Makes Precision Photomasks For Semiconductors).

To sum it up, PLAB demonstrated growing revenue, growing margin, and a very strong balance sheet (i.e. cash rich).

Going Forward

During the Q2 conference call, CEO Frank Lee reported:

We are building partnerships with several key customers and we also signed many long term purchase agreements, so-called LTPAs with our key customers. This kind of approach serves us very well to make critical investments and it helps us to quickly get return on our investment.

In my opinion, these long-term purchase agreements de-risk PLAB’s revenue going forward and is yet another reason the stock is undervalued. As Lee said on the conference call, PLAB is on track to deliver the best year in company history.

EVP and CFO John Jordon also commented during the conference call on why margins are so strong:

We have based our investment plans on that expectation and we anticipate that the increased margins will be sustained by the demand-supply imbalance due to limited trailing edge capacity.

Later on in the conference call, and in response to an analyst question, Jordon expanded on the issue of margins:

… we have long term purchase agreements with many customers, some of which we’ve kind of renegotiated, and there were others coming up for renewal, some are one year, some are longer than one year, and as they come up for renewal, the prices–you know, the opportunity is still there to continue the price increases. A lot of our locations are at capacity, so where the operating leverage is outstanding from those locations and then the opportunities created by the business environment to improve pricing, we expect to continue well into the future.

On cap-ex, Jordon reported $16 million during Q2 and that PLAB received a little over a million in government subsidies for investments made in China. PLAB’s total cap-ex for the year (net of subsidies) is $33 million and the company still expects cap-ex of $100 million for full-year 2022 as it continues to invest in increasing its mainstream IC capacity and to increase the size of its facility in Taiwan.

The company’s guidance for Q3 was as follows:

- Revenue in a range of $205-$215 million

- EPS in a range of $0.45-$0.55/share.

Note that the midpoints of the guidance, revenue of $210 million and EPS of $0.50/share would be a slight sequential increase as compared to Q2, but would be up significantly on a year-over-year basis (Q3 of last year: revenue $170.6 million and EPS of $0.28/share).

Risks

Photronics is not immune to the macro-environment: specifically the global pandemic as it relates to potential shut-downs in China as well as high inflation, rising interest rates, and the threat that broken energy & food supply chains as a result of Russia’s invasion of Ukraine pose to the global economy.

There is always the potential that the US/China trade war could become more hostile and governmental export sanctions impacting PLAB are a possibility. That said, much of PLAB’s business in China is supported by facilities located there in China.

Summary & Conclusion

PLAB is currently growing both revenue and margin as a result of strong end-market demand and being in a very good position to negotiate favorable (and long-term) contracts due to demand being greater than supply. The company is cash-rich and continues to ramp-up capacity at its two new facilities in China. With a forward P/E of only 10x, this stock is a real value and is a BUY.

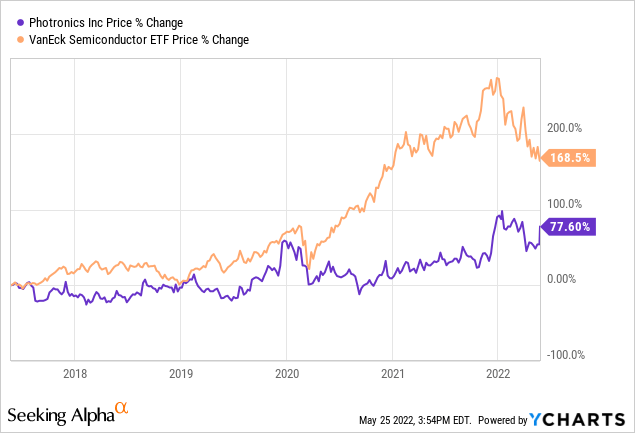

I’ll end with a five-year chart of PLAB’s stock price and note that it has severely lagged the over-all semiconductor industry as represented by the VanEck Semiconductor ETF (SMH):

Read More: Photronics Stock: Extreme Value In The Semiconductor Sector (NASDAQ:PLAB)

{kind=link}