Udomkarn Chitkul/iStock via Getty Images

Emergent BioSolutions’ (NYSE:EBS) stock has spiked up over the past week as a monkeypox outbreak begins to spread in Europe and North America. Unlike with COVID-19 we already have approved vaccines that can work for monkeypox. Emergent has a smallpox vaccine branded ACAM2000, which is expected to be effective against monkeypox due to its close relation to the variola virus that causes smallpox. Furthermore, Emergent recently announced that they have made a $225M deal with Chimerix (CMRX) to acquire the exclusive global rights to their smallpox antiviral, Tembexa. The appearance of a potential new pandemic could be an occasion for Emergent to showcase their portfolio and regain a bit of credibility to respond the global health emergencies. Therefore, I am declaring EBS as my top pick for the monkeypox outbreak.

I intend to review the company’s products that could be deployed against monkeypox and will discuss how Emergent BioSolutions can be a major contributor to combating the virus. In addition, I take a look at the company’s valuation and will discuss how it impacts my investment strategy.

Emergent’s Monkeypox Options

ACAM2000 is the company’s second-generation cell-cultured smallpox vaccine that was developed under contract with the CDC. ACAM2000 was approved by the FDA back in 2007 and has 200M doses in the U.S. Strategic National Stockpile. Although ACAM2000 is a smallpox vaccine, it is expected to work against monkeypox because the monkeypox virus is closely related to the smallpox virus.

In addition to ACAM2000, Emergent has acquired the rights to Tembexa (Brincidofovir), an oral antiviral for all ages that was approved for the treatment of smallpox in 2021. Tembexa is a prodrug of cidofovir that allows for higher intracellular and lower plasma concentrations of cidofovir, thus increasing its activity and permitting oral bioavailability. In December 2021, BARDA delivered a request to procure up to 1.7M treatment courses of Tembexa. Chimerix believes that the BARDA procurement contract could occur as early as this quarter.

Discussing The Opportunity

Is there a risk? Well, the fact the virus has infiltrated multiple continents does present the risk of a long-term battle to contain the spread and prevent a mass outbreak. What is more, Monkeypox has a 3%-6% fatality ratio, whereas COVID-19 is estimated at 2%-3% worldwide, so, we can say that monkeypox is a significant threat if we fail to contain the outbreak. Sadly, I believe public health organizations might have a big issue if they are unable to rally the world’s population for another viral threat and convince people to be inoculated after the COVID-19 vaccine fiasco.

Who is at risk? Indeed, we eradicated naturally occurring smallpox through a vaccination campaign back in the 70s and officially eliminated it in 1980. That success means the majority of the world’s population does not have substantial immunity against monkeypox. What is more, the older adults who are already vaccinated against smallpox might have a small amount of protection, however, that protection has most likely weakened over time. Essentially, the entire population is at risk of catching monkeypox.

Can Emergent Contribute? It is also important to note, that, unlike COVID-19, we already have monkeypox vaccines from Emergent and Bavarian Nordic (OTCPK:BVNKF), thus, if a mass vaccination campaign is going to happen they are going to be the first two in line for additional vaccines. Moreover, Emergent and SIGA Technologies (SIGA) have approved antivirals that could be deployed to treat patients. Again, Emergent makes a vaccine and has an antiviral, so there won’t be a big pharma arms race to fight for government contracts. Therefore, Emergent has a chance to redeem itself by being a principal producer of vaccines and their newly acquired antiviral for monkeypox.

Tempering Expectations

One cannot deny there is an opportunity for Emergent to see a resurrection after a report from the US House select subcommittee discovered that about 400M COVID-19 vaccine doses were potentially discarded owing to cross-contamination at the company’s Baltimore plant. However, it is possible that this monkeypox outbreak could be contained rather quickly as health organizations begin to contact trace and work to isolate the infected. Historically, monkeypox has never amounted to more than an exotic event. In fact, monkeypox has been around since 1958, and yet the first human case wasn’t reported until over a decade. The US experienced an outbreak back in 2003, after getting a delivery of animals from Ghana, which was quickly contained. In view of that, we can expect that this monkeypox outbreak is likely to be quickly squashed and there will be no need to roll out a widespread vaccine campaign to contain the current outbreak.

Even if a small number of the world’s health organizations start a vaccination campaign, Emergent is not the only smallpox/monkeypox vaccine player on the market. As I mentioned earlier, Bavarian Nordic has their vaccine, Jynneos. What is more, BARDA is paying Bavarian Nordic $119M to add Jynneos to the stockpile with options for an additional $180M worth of doses through 2024 and 2025.

It is possible that in the end, the outbreak will be quickly contained and the government will not need to use the stockpile. Even if the government does decide to unload a portion of the stockpile vaccines, it is possible Emergent does not sign any contracts for monkeypox products, and other smallpox/monkeypox companies are selected.

Still Focused On Valuation

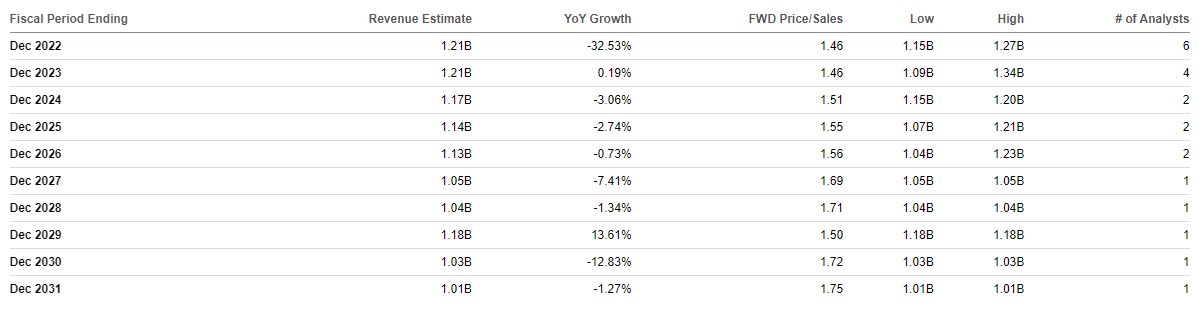

At this point, my bull thesis is centered on the company’s valuation discount valuation. At the moment, EBS is trading at a 1.46x forward price-to-sales for 2022 which is substantially under the industry’s average of 5x price to sales.

Emergent BioSolutions Analyst Revenue Estimates (Seeking Alpha)

When we look at a few valuation models, we can see the intrinsic value for EBS is much higher than it’s currently trading at. The DCF growth 5-year exit values the ticker at $46.68 per share and the growth 10-year is $55.71. The P/E multiples have the ticker at $59.54 per share and the earnings power value has EBS at $58.48. What is more, the EV/EBITDA multiples are pointing to an intrinsic value of $97.78. So based on a number of standard valuation models, EBS has a 32% to 178% upside from its current value. In fact, the Seeking Alpha Valuation gives EBS a B+.

Focusing On Value

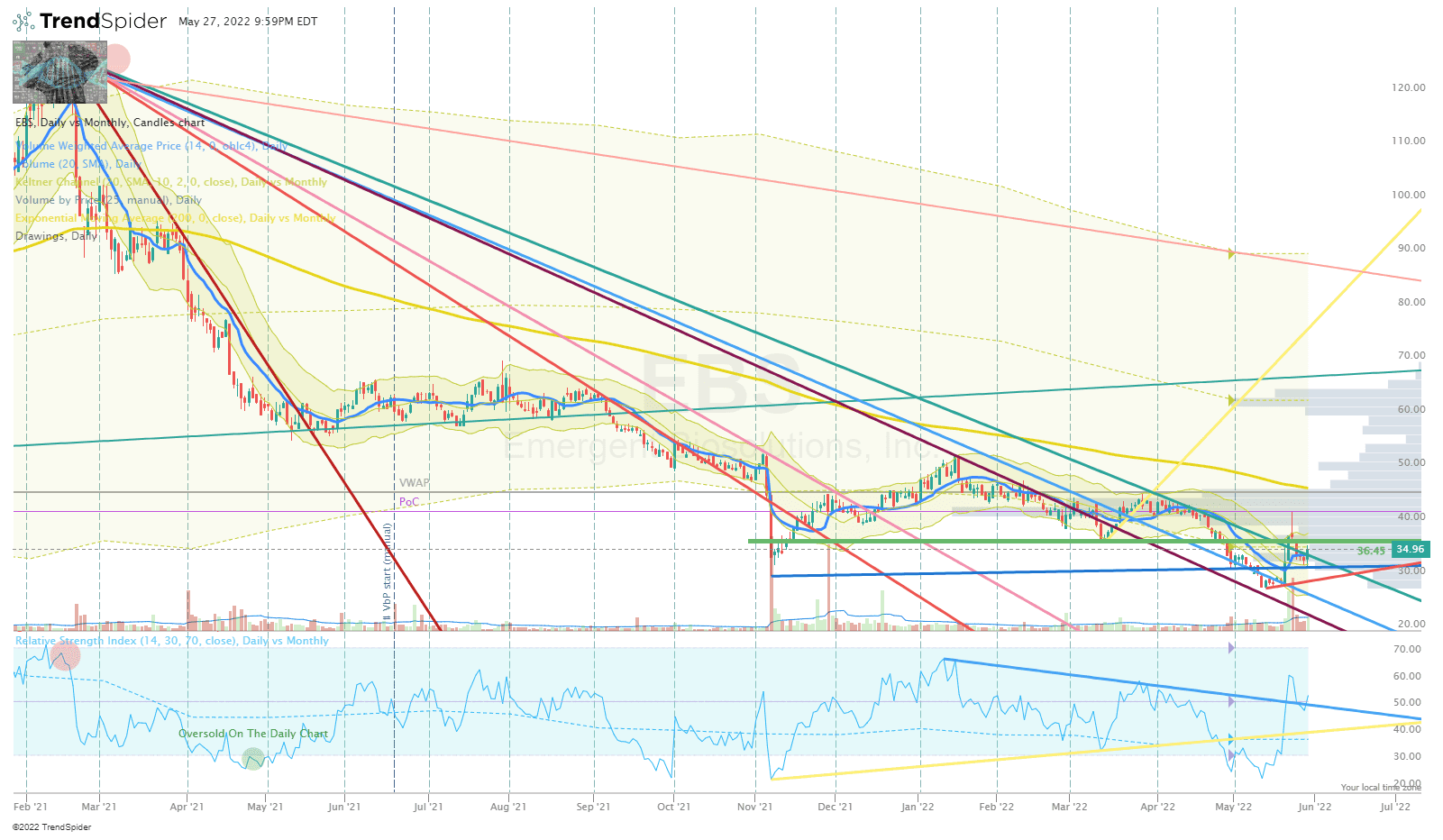

Emergent has been catching a lot of flak over the past year and the share price shows the damage. EBS has lost roughly 40% over the past year and has struggled to sustain a rally for more than a few days.

EBS Daily Chart (Trendspider)

EBS Daily Chart Enhanced View (Trendspider)

Indeed, small and mid-cap healthcare stocks have struggled since February of 2021, and EBS was not immune to the relentless sell-off. However, I must admit that Emergent’s near-term prospects are not as promising as it was a couple of years ago as COVID-19 vaccine demand subsides. Accordingly, we have to expect the decrease in earnings will weigh on the share price in the near term. However, the weak earnings are still expected to be positive earnings and are projected to report EPS growth in the coming years.

Emergent BioSolutions Analyst EPS Estimates (Seeking Alpha)

We can see that EBS is expected to report a forward EPS of $4.35 in 2024, which is a forward P/E of 8.10. Considering the industry’s average P/E is ~21x, we can say that EBS is a discount for their projected future earnings.

Keep in mind, that none of these projections are factoring in any potential revenue from monkeypox-related government contracts. Clearly, this could have a dramatic impact on the company’s near-term performance. Remember, the vast majority of the world’s population does not have immunity to monkeypox, which means the world could need millions if not billions of vaccines if things were to get out of hand.

Not only does Emergent have monkeypox products to help with a potential pandemic, but they also have the manufacturing capacity to supply these products on a mass scale.

Considering the points above, I am still bullish on EBS at these prices. Indeed, Emergent has a few downside risks, including potential consequences from the COVID-19 vaccine debacle. As a result, I am looking to take a conservative approach to add to my dormant EBS position.

I have set my Buy Threshold at $35 per share, which is essentially the most I am willing to pay for EBS at this point time. My game plan is to make one upsized addition in the near term and will start to make small periodic investments over the remainder of 2022. If the share price drops below $25 per share, I will be increasing my sizing to take advantage of the discounted valuation.

Indeed, I will look to book profits in order to get my position into a “house money” state. By removing my initial investment, I will de-risk my position, which in turn will allow me to hold a speculative position for at least 5 more years in anticipation that Emergent will be able to find additional opportunities for M&A as part of their 2024 growth plan.

Read More: Emergent BioSolutions Stock: A Top Pick For The Monkeypox Outbreak (NYSE:EBS)

{kind=link}