Drew Angerer/Getty Images News

Apple stock

Apple (NASDAQ:AAPL) stock has fallen more than 17% year-to-date (YTD). And this is after a much-needed 8% rise last week. The rise may be because some optimism is creeping back into the market, or it may be short-lived. The market will likely continue to be tumultuous. I would not be surprised to see Apple stock retest its recent lows shortly, and many Seeking Alpha contributors are bearish. Even Michael Burry (of The Big Short) has hedged with Apple put options. But this is likely a short-term play.

What about the long-term investor?

Warren Buffett purchased another $600 million worth of Apple in the first quarter of 2022, so there is a little battle of the titans happening. Buffett mentioned that he would have purchased more, but the price rose. $600 million amounts to little more than a rounding error on Berkshire’s (BRK.A)(BRK.B) total Apple ownership of around $159 billion. But it offers a tremendous clue as to where he sees fair value in the stock. The Q1 2022 low price was just over $150 per share.

The backdrop

The investing conditions in 2022 have been fascinating and challenging. They have also offered investors terrific entry points on many stocks caught up in the general malaise. Many recently public stocks that were all hype in 2021 have returned to Earth just as quickly as they left.

The biggest culprit is obviously the sky-high inflation rate, leading the Federal Reserve (the Fed) by the nose into a rising interest rate environment. Prior failures by the Fed to recognize and respond timely to crises don’t inspire confidence, and some investors have long memories.

However, there is also good news. Many companies, like Apple, are releasing impressive earnings and producing gobs of free cash flow. Unemployment remains low, and demand is high. We have a supply problem, and it takes longer to smooth out than we would like.

As long-term investors, it can be challenging to keep perspective. And for some new investors who came to the market after the March 2020 crash, it can be even more problematic as it may be a first bear market experience.

The market takes a downturn, and we have another kind of race to the bottom. Who can write the direst headline and report it in the largest and boldest font? It’s 2000, no, it’s 2008, no, it’s the 1970s, and either way, we’re all doomed!

But fear and emotion, just like hope, aren’t long-term investing strategies and can lead to knee-jerk and, ultimately, money-losing trades. Hopefully, we have kept a percentage of cash on the sidelines to take advantage of such a downturn and see us through.

There is no one-size-fits-all investment strategy, but I have some suggestions.

Apple’s results, return of capital, and two concerning metrics

Apple continues to post records for revenue despite supply-chain headaches. Rumors of Apple’s potential supply-chain problems persist, yet the company’s all-star management team delivers. Apple also has tremendous leverage due to its size and importance to its suppliers.

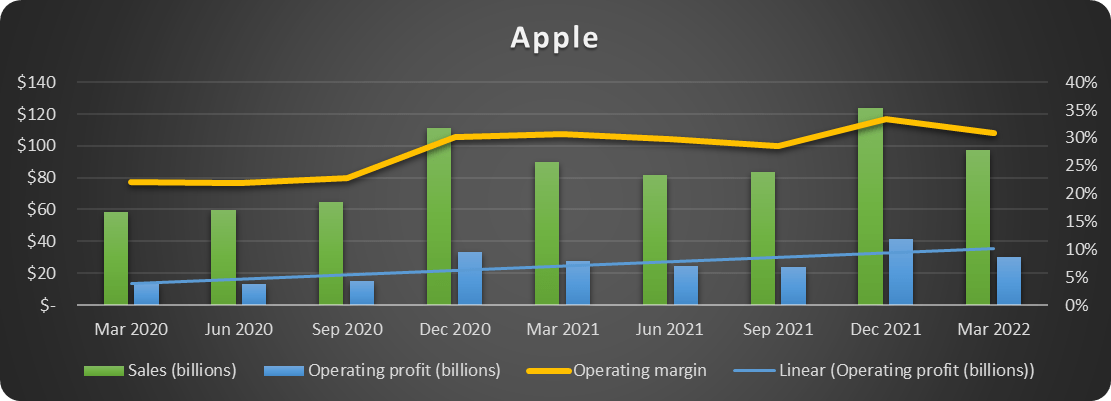

Q2 FY2022 sales rose 9% over the same period in 2021 to reach $97 billion. Services revenue is up 20% through the first two quarters of fiscal 2022, and iPhone revenues remain robust. Services revenue included advertising, the App Store, and cloud services.

Apple has increased its gross margin and operating margin year-over-year (YoY) through the first two quarters of fiscal 2022, as shown below. This is encouraging and a testament to strong management.

Data source: Seeking Alpha. Chart by author.

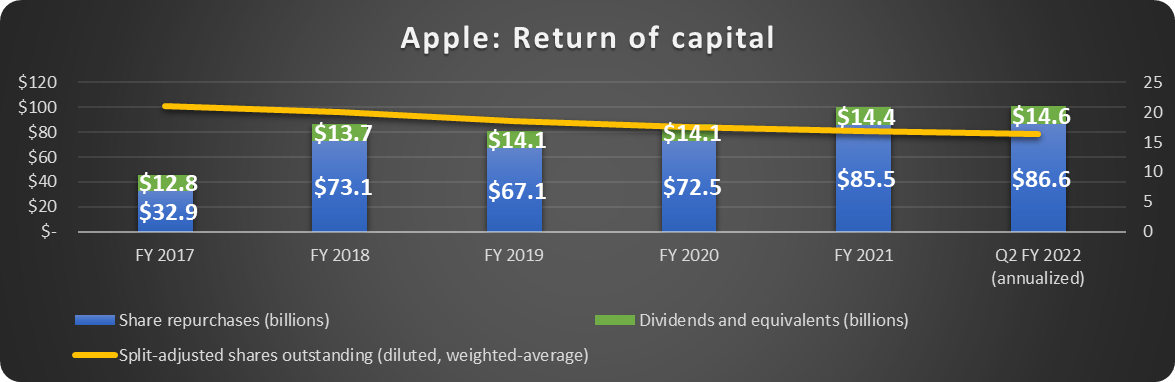

The return of capital to shareholders also continues in earnest. Apple has returned over $50 billion to shareholders between share buybacks and dividends through Q2 fiscal 2022. Apple is on pace to exceed last year’s brisk pace. Over $500 billion will have been returned to shareholders since fiscal 2017 by the end of fiscal 2022 if the current pace continues. This amounts to well over 20% of the current market cap.

Data source: Apple. Chart by author.

Share buybacks are a terrific vehicle for companies to support the share price during a downturn. The buybacks gain more leverage as the stock price drops since more shares can be repurchased and retired for the same dollar investment. This adds some weight to investor returns when the market is bullish again. It also helps long-term shareholders sleep well at night. If the price drops in the short-term, management will use the opportunity to retire more shares for us.

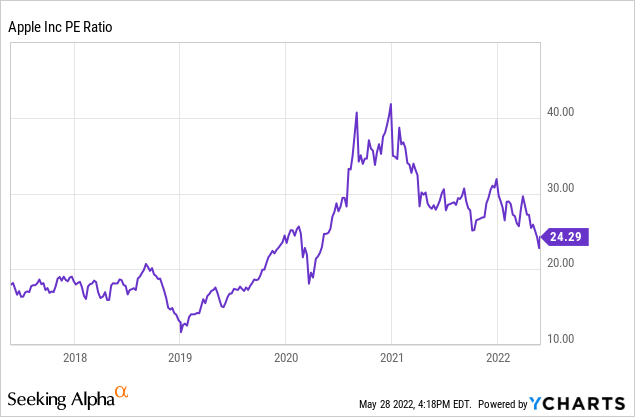

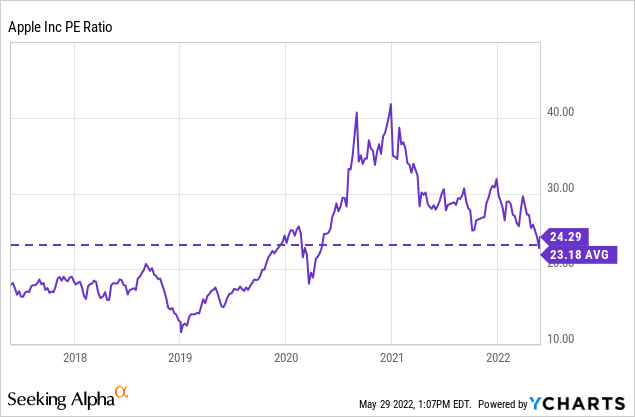

There are two concerns that stand out currently. First, Apple stock is trading at a price-to-earnings (P/E) ratio slightly higher than its recent historical pre-pandemic norm, as shown below.

This suggests short-term downside risk.

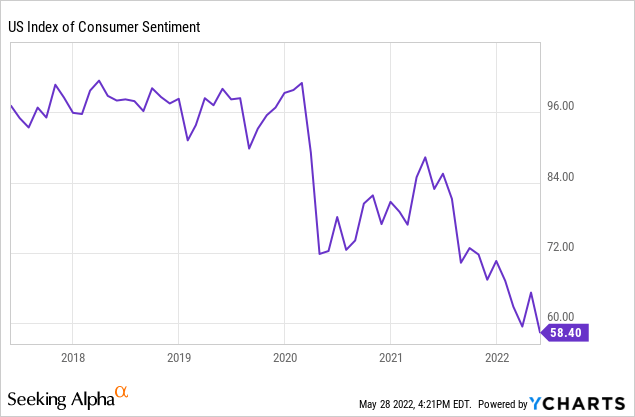

Another cause for concern is the cratering of consumer sentiment. Consumer sentiment is seen as one of the best barometers of consumer spending.

In early to mid-2021 it looked like sentiment was going to return to normal as COVID-19 waned. Then inflation hit, and sentiment plummeted. It is now far lower than during the worst of the pandemic. This is extremely concerning for companies that rely on discretionary spending. Apple has a vast, dedicated customer base that should provide some stability.

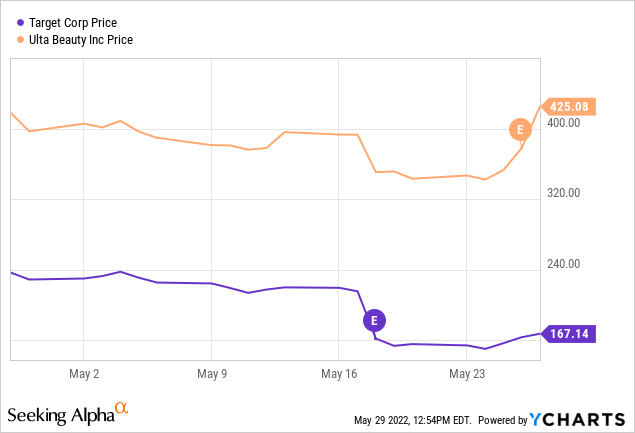

Target (TGT) in particular posted a disappointing quarter and more than 20% of its market cap was shaved off. This spooked the market. On the other hand, Ulta Beauty (ULTA), released excellent results and the stock went in the opposite direction.

Apple is reportedly working on a subscription model where users could pay for a device monthly. Subscription plans are optimal for a couple of reasons. First, it makes it easier for people to upgrade when times are tight. It also creates recurring revenue for the company. Partially moving to a “hardware-as-a-service” model is definitely intriguing.

More than one way to peel an Apple: 3 Strategies for investors

Dollar-cost averaging

Entering into a stock position through timed incremental purchases is known as dollar-cost averaging (DCA). In a choppy market and over a long timeline DCA is incredibly important. It allows the investor to avoid buying at a peak and take advantage of dips in a stock’s share price. It is ultimately a risk mitigation tool. Timing a market bottom is not possible on a consistent basis, DCA takes the uncertainty out of it.

An investor who began to purchase Apple stock on January 1, 2020 and purchased in equal allotments on the first day of every quarter would have an average purchase price of $122.90 despite buying on some of the recent peaks.

This is a disciplined way for long-term investors to continue to grow their portfolios over many years and capitalize on down markets.

A more active variation on this strategy is to purchase when the stock reaches a specific metric. Apple is flirting with its five-year average P/E ratio. This is an interesting short-term benchmark.

Covered call options

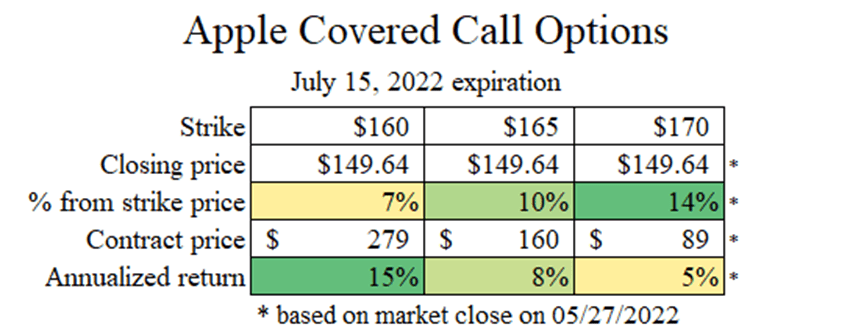

Some Apple stockholders are in a tough spot. They believe the stock is somewhat overvalued, but do not want to actively trade. Selling every time Apple becomes slightly inflated can create a massive tax bill and increases the risk of poorly timed trades. Selling out-of-the-money (OTM) covered call options could be a money-making opportunity as Apple stock trades at a P/E above historical averages and we are in a down market.

Selling an OTM covered call creates an income stream and is relatively low risk. The worst that can happen is that Apple stock rises above the strike price and the shares are called away at that price. Selling the option at a strike price at which the investor would definitely sell the stock anyway eliminates this concern. For instance, let’s assume that if Apple rises above $165 by July 15, it would be a strong sell.

Apple July 15, 2022 call options with a strike price of $165 per share are selling for $1.60 currently. Since options are sold in lots of 100 shares, this would net the seller a premium of $160. Provided Apple stock does not break out past $165 over the next 45 days, the seller will pocket a nice 8% annualized return.

Below are some other examples of current options and premiums from the market close on May 27, 2022. A higher return comes with a higher risk that the shares will be called away.

Market data: TD Ameritrade. Table and calculations by the author.

Options inherently carry risk and should only be used by investors with appropriate knowledge and risk tolerance.

Buy and Hold

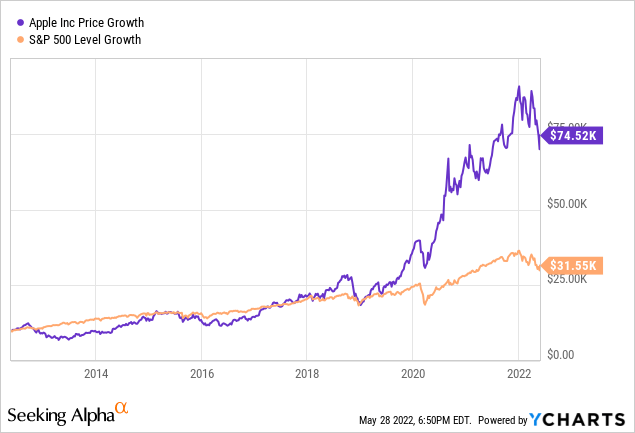

I know this idea seems incredibly boring, doesn’t it? After all, what will we fill our time with when we aren’t breathlessly waiting for the latest Fed meeting minutes to be released? But here’s the secret – it actually works. Buying great companies with outstanding management and holding them for years and years is a terrific way to increase wealth. Buy great companies, then get out of the way and let them do great things. This has certainly been the case for Apple over the last decade. Without buying or selling a single share, making an options trade, or even looking at an account statement, an investor with patience has been rewarded, as shown below. It worked for Warren Buffett, who began buying Apple stock in 2016.

Bear markets are hard on investors’ psyche. No one likes to see any of their hard-earned money melt away. Unfortunately, the stock market and economy don’t always cooperate. Each investor has a different timeline, financial goals, and situation. Still, long-term investors who prioritize time in the market over timing the market often come out on top.

Apple stock has come down substantially from its highs, yet the secular positive track for the company remains intact. There are large macro concerns that the company will need to deal with shortly. Management has a track record of outperformance and the resources to support shareholders. As the valuation comes back to Earth, investors have several options to capitalize on Apple’s success.

Read More: Apple Stock: Hope And Fear Are Not Strategies – But These Are (NASDAQ:AAPL)

{kind=link}