David Ramos/Getty Images News

Author’s Note: This is the free version of a premium article posted on iREIT on Alpha in June of 2022.

Dear readers,

In this piece, we’re going to take a look at European telco giant Vodafone (NASDAQ:VOD). The company is a world-leading telco operator with one of the largest bases of customers on earth (close to 600 million combined in Europe, the Middle East, Africa, and Asia, with around 375 million in India).

We’re going to talk about the history and foundations of the company and look at where the company is going. Also, and most importantly, we’re going to see what we can make by investing in the company at this valuation – or at what valuation we should be starting to invest in Vodafone.

Vodafone – Looking at the company

When looking at Vodafone, we want to begin by understanding the company’s history – because it’s a relevant one. The company, along with its joint ventures, offers telephone, mobile, and broadband services to over 550 million customers worldwide.

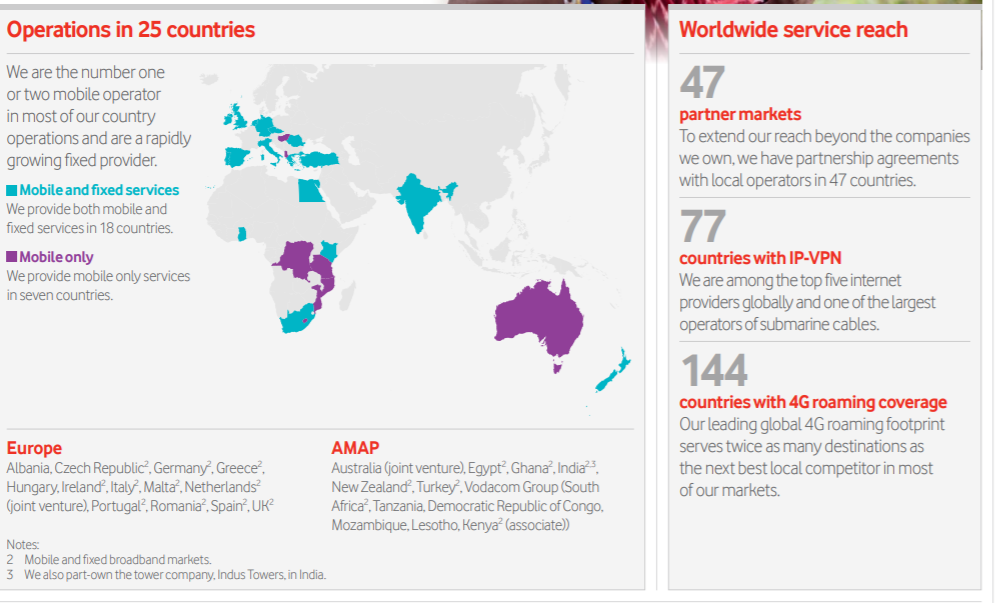

Vodafone operations (VOD IR)

Some of Vodafone’s main markets include Germany, Italy, and the UK, which together account for roughly 50% of its group revenue. The company’s plans for this exposure are quite clear – they aim to diversify into further markets in India, Africa, and other nations/continents in order to decrease their dependency on Europe as a market, which is now in the middle of its execution. Vodafone as an entrant into the Indian market has seen some success, and they currently have over 375 million subscribers in India alone. These subscribers will double as a result of Vodafone’s merger with Idea Cellular, which was closed in mid-2018.

Vodafone Presentation (VOD IR)

Before 2014, Vodafone owned a large (45%) stake in the US telecommunications giant Verizon (VZ). This was sold as a part of the company’s restructuring plan. The stake was sold for $130B, and the asset sale that Vodafone has undergone as part of its plans to “cut the cord” in pay-TV and similar ventures is part of what’s depreciated the stock’s nominal value over the past few years.

Vodafone’s strategy over the past few years has included the M&A of smaller wireless and telecommunications companies and the development of its services into a full-range suite of communication plans for customers worldwide (with a core focus on Europe). The acquisition of Liberty Global is the latest feather in the company’s now-extensive cap of transactions.

Vodafone’s historical and current stance on India as a market is that it represents an important driver for future growth (hence the fight for almost a billion customers), and they continue to plan to grow in the country.

Vodafone also manages several 5G initiatives across Europe, among other things, in the complete company rollout of the new communication standards across the continent. This is much alike the plans of AT&T (T) and other global/American telecommunications giants, which are all currently facing the CapEx-intensive prospects of expanding already existing 4G networks into 5G.

Vodafone Presentation (VOD IR)

However, all is, of course, not well in the Indian market. Tough competition, which has heated up even more insistently since the launch of Jio back in -16. It’s also fair at this point to say that the promised windfall and “growth” story has turned into a ball-and-chain around Vodafone’s corporate ankle. In summer 2020, the Supreme Court ruled that Indian operators definitely have to pay the untold (zillions, not yet estimated) amount of rupees of the historical spectrum and license fees to the government that this same Court had decided to impose in the previous autumn. Who was the most affected by the ruling?

Vodafone. The winner of the ruling is Jio, which not only owes very little money but already is an Indian market leader. Vodafone’s degree of loss and issues here is hard to overstate, given that Vodafone chose to give out a 35.8% stake in its company to the government of India rather than paying out the interest owed to the government.

Thankfully, VOD is a primarily European player, despite its hundreds of millions of Indian customers. You may get the picture that Vodafone is not an especially well-managed company, but this is not entirely true. Management made extremely smart plays that have been overlooked by the broader market. What I am speaking about is the company’s Post-VZ cash-long state, where Vodafone took advantage of telco Europe to buy several EU cable operators.

The Kabel-Deutschland bid in 2013 allowed Vodafone to enter the German quad-play communications market, while the strategic M&A of Ono allowed it to strengthen its position in Spain. Vodafone acquired Liberty Global’s operations in Germany, the Czech Republic, Hungary, and Romania for €18.4bn back in -18. From a fundamental viewpoint, this operation was excellent for Vodafone. In Germany, by buying the cable operator Unitymedia, Vodafone built a converged national challenger to Deutsche Telekom, bringing the fixed-side Gigabit connections to 25m German homes (62% of total German households) by 2022, and the company has been leveraging its capabilities since. The current share price and view on Vodafone often do not reflect this, and viewing many of the articles published on Seeking Alpha, it’s my view that this is an often little-known fact about the company.

In one of its main markets, Germany, Vodafone is now one of two giants, with the other one being Deutsche Telekom (OTCQX:DTEGY). By that, I mean operators that offer both fixed and mobile communications, which most peers do not. The group will be a key utility there, a cash machine that offers good visibility for at least 30 years.

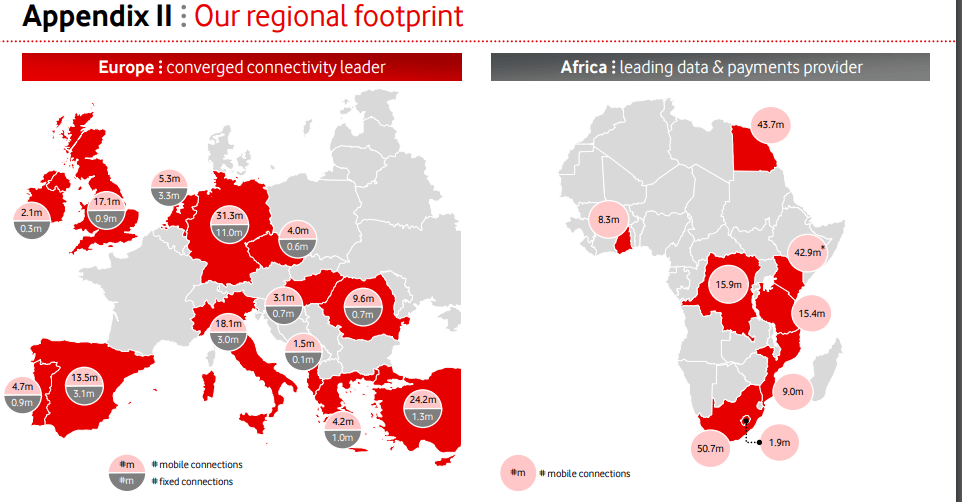

In the Czech Republic, Hungary and Romania, Vodafone was primarily active in the mobile segment of these markets (with 15.8m mobile customers) and has no meaningful presence in each country’s fixed-line or TV segments. In these markets, it’s a tertiary operator with a quarter of market share or thereabouts, with the exception of Romania, where it has nearly a third.

Liberty Global is primarily a fixed-line and TV operator (with 1.8m broadband and 2.1m TV customers) with little or no mobile activities in these countries. So the key point that I’m trying to make in this article as to these operations is that this transaction allows and accelerates the availability of converged fixed, mobile, and TV services in the Czech Republic, Hungary, and Romania.

Vodafone Presentation (VOD IR)

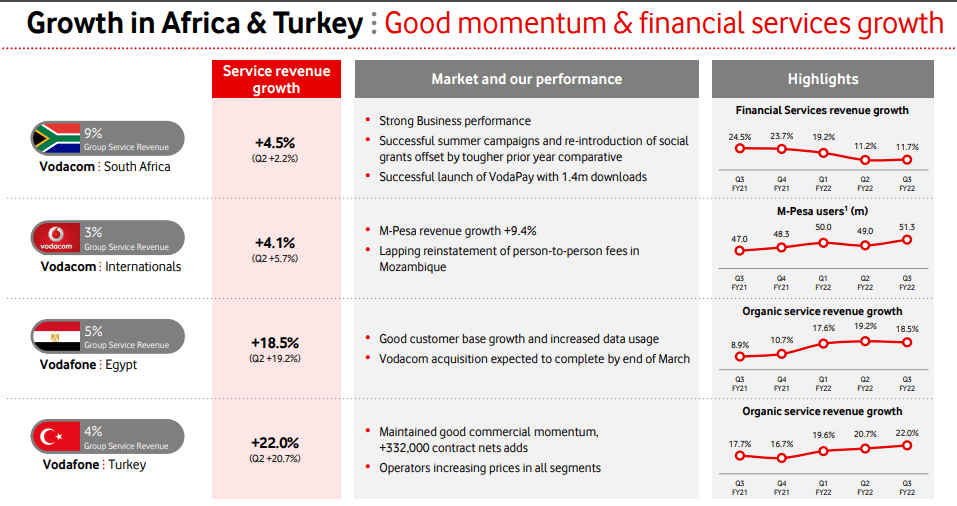

The company’s non-EU operations in Egypt, South Africa, and other things are of significant interest as well, having turned into an African powerhouse. I’m of the camp that believes Africa to be a very significant future player in global economics, so I’m always looking for new ways to gain exposure to the continent.

COVID-19 wasn’t good for Vodafone. The company suffered from lower roaming revenues, especially as travel trended down, but has been returning to growth since then. In particular, Vodafone can focus on its fixed activities as part of its resurgence of profitability. In the company’s main revenue generator Germany, the growth is actually solid in terms of trends, even though VOD is still mostly struggling in geographies like Italy.

The company reported FY22 not that long ago, which included annual revenue growth of 4%, which was more or less according to overall expectations. EBITDAaL was up 5% as long, in line with expectations as well.

The good news was that FCF actually beat expectations, and Vodafone showcased just what a quality telco can do in terms of free cash flow generation when things are working – the negative news was a dividend stuck at 9 cents (though it wasn’t really expected to grow here) per share, as well as a relatively modest FY23 guidance, which is likely to overhang the company’s compressed/pressured share price here.

Still, the company has very conservative leverage, at around 2.7X net debt/adj. EBITDAaL, and intends to continue to push CapEx in order to improve its overall assets – good news, all things considered. We look at Vodafone like we look at most telcos – EBITDA less CapEx cash flow generation.

The problem is that the market does not see Vodafone growing enough considering its impressive assets, which is why the market is punishing the company. This doesn’t reflect the conservative safety Vodafone actually seems to be offering and the integration that seems to be ongoing. Vodafone is indeed continuing to make good progress on integrating Unitymedia, with the rebranding and TV portfolio harmonization now complete, and the organizational integration completed. The broadband customer base has reached nearly 11M, with 23.8M households now able to access Gigabit speeds.

Elsewhere in Europe, the UK sees good momentum (EBITDA up by 3.3% YOY), competitive Spain experiences a return to very slight revenue growth and Italy, the toughest market of the group with continued price competition, is declining less, and EBITDA is stabilizing. In short, everything Vodafone is seeing is growth, with the one exception of Vodafone India.

Risks to Vodafone

As you might expect, India is one of the biggest risks that bear mentioning here – though I will say that with Vodafone leaving a significant stake to the Indian government, the issue here should be all but over. Aside from its Indian issues, there are a few things that will weigh on Vodafone in the near future, as I see the risks.

First is the CEO. Nick Read probably has done some good things – but the list of utter catastrophes under his watch is long. From missing opportunities in Italy with Iliad, Spain with the Orange-Masmovil Merger, and with the Vantage story where Brookfield and Global Infrastructure Partners made a €14.5B unsolicited offer for a majority stake in the unit, but Vodafone would prefer to make a deal with a telco (likely Orange) rather than financial investors. A mistake, as I see it – and he continues to make them. Management, specifically…

Read More: Vodafone – Pan-European Telco Safety (NASDAQ:VOD)

{kind=link}