krblokhin

It’s been a little over 5 months since I wrote my bullish article on Bed Bath & Beyond (NASDAQ:BBBY), and in that time, the shares are down about 68% (!) against a loss of about 12.75% for the S&P 500. The trade initially worked out very well, driven largely by rumours of a sale but from the end of March to the present, the shares have absolutely cratered. In my article, I acknowledged that the firm is very troubled, but I was intrigued by the insider buying that was then happening. In fact, it was the only bright spot I could find, and I bought in spite of that. I think my experience here offers investors an interesting cautionary tale: insider buying alone isn’t a sufficiently powerful reason to buy. Insiders know a business better than the rest of us, but they aren’t omniscient. I think this is relevant to people who are buying based on recent insider transactions.

Thankfully, I only bought a few hundred shares, but I’m also short puts that were at the time deep out of the money, but are now deep in the money, so it’s time to think about this investment again. I’ll comment on the most recent financial history here, and will also look at the stock as a thing distinct from the underlying business. Of course, I’ll also write about the puts because I think there are lessons to be had here.

Here comes my ubiquitous “thesis statement.” It’s here where I offer you the highlights of my thinking in a (hopefully) succinct nutshell so you won’t have to wade through 2,300+words of “Doyle mojo.” I think the financial performance here has deteriorated precipitously and rapidly. The capital structure in particular has gotten far worse in only three short months, with long term debt up dramatically, and cash down dramatically. In my view, the financial performance here has gone from “bad” to “appallingly bad” in a very short period of time. When I wrote my previous missive, I knew that the company was performing badly, but I took a small position because of the insider buying. My experience with this investment has caused me to think more deeply about insider buys. The number of failed startups demonstrates that just because someone knows the most about a given business doesn’t mean they’re right. This experience has shown me that we need some sort of confirmation that the people who are buying are making the right decision. We also need to look at what percentage of their wealth they’re putting on the line. If they’re only committing a tiny fraction of their own wealth, why should we not do the same, or simply avoid the stock?

Another lesson involves my short put strategy. I’ll be buying back the puts I wrote earlier at a loss. I wouldn’t be me, though, if I didn’t try to spin my trade in as positive a light as possible. Although I’ve lost about $4 per contract here, that performance has been far less bad than the $10 per share loss on my few hundred stocks that I bought at the same time. Given the life I’ve lived “less bad” is sometimes a win. Even in this very troubled circumstance, short puts were a superior, risk adjusted choice. Also, you may wonder if this episode makes me nervous about the idea of selling deep out of the money puts in future. Far from it, as this is the exception that proves (or “proofs” if you like to be archaic). Not to get too philosophical with a Seeking Alpha audience, but the existence of this exception offers further proof for the rule that selling deep out of the money puts offers a lower risk trade. I don’t even need to get too fancy with my rhetorical footwork here either. I did badly on my short puts, but I did very, very badly on my long stock position.

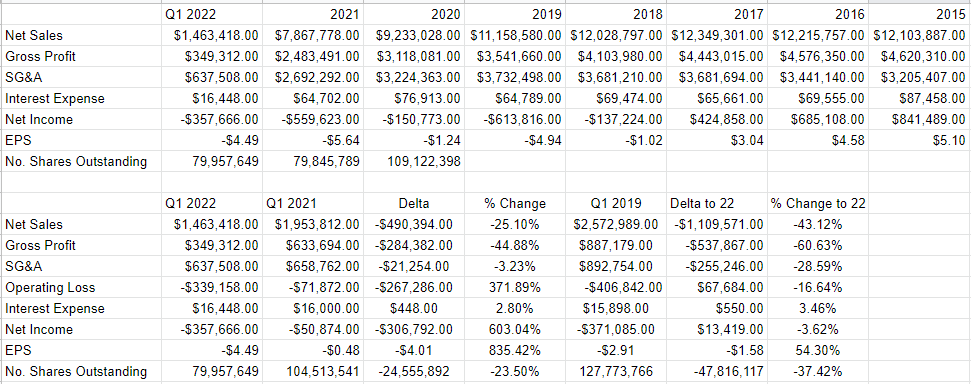

Financial Snapshot

The most recent financial results have been shockingly bad in my view. I’ll start with the bad news and finish with the very bad news. Sales and net income both deteriorated dramatically in the quarter relative to the same period a year ago. Specifically, sales were about 25% lower than they were in Q1 2021, and net income jumped from a loss of $50.8 million to $358 million. So revenue was down by a quarter, and net loss was over six times worse. I looked back in time, and found that 2021 wasn’t anomalously good, making comparisons to it particularly harsh. For instance, net income during the first quarter of 2022 was fully 43% lower than it was in 2019. In fairness, net income in 2022 was better by about $13.4 million, but that’s the consequence of the fact that in 2019, the company took impairment losses of ~$401 million. My regulars know that I’m not a fan of “adding back” non-cash losses like this, but we have to admit that in the absence of these writedowns, we would clearly see that performance in 2022 has been uniquely bad.

When we turn our gaze to the capital structure, things get noticeably worse in my view. Specifically, long term debt has grown by a net $197.3 million, or 16.7% over the year. At the same time, cash on hand has cratered, down just under $1 billion or 90% from the year ago period. Most of this deterioration happened during the first three months of the year. Although merchandise inventory is only about 2% higher than it was at the end of the year, it’s fully 12.5% higher than it was at the end of Q1 2021. Merchandise inventory sat at about $1.76 billion at the end of the quarter. Given the growing risk of recession, this obviously raises the spectre of an upcoming write-down.

In my previous missive on this name, I characterised Bed Bath and Beyond as “troubled.” I’ve modified my views somewhat. I would now characterise it as “very troubled.” That said, even the most troubled company can represent reasonable value at the right price. At this point, Bed Bath & Beyond may be what the great Ben Graham referred to as a “cigar butt.” I’ll take a puff of it at the right price.

Bed Bath & Beyond Financials (Bed Bath & Beyond investor relations)

The Stock

My experience with this stock demonstrates the truism that “what the market giveth, the market taketh awayeth.” For that reason, I’m more “gun shy” than usual when it comes to buying this stock. I need to remind readers that we’re seeking “risk-adjusted” returns, not simply returns. This is because the price returns we’ve generated from following the momentum of the crowd can be taken from us relatively quickly.

Anyway, my regulars also know that I consider the stock and the business to be very different things. If you’re new here, and you haven’t heard me drone on about this to the point of tedium, let me tell you now: I consider the stock and the business to be very different things. Specifically, every business buys a number of inputs like inventory for instance, performs value-adding activities to those like displaying them in an attractive venue, for instance, and sells the results. Hopefully, this results in a profit. Eventually. Anyway, in the final analysis, that’s what every business is. The stock, on the other hand, is an ownership stake in the business that gets tossed around in a market that aggregates the crowd’s rapidly changing views about the future health of the business. Additionally, the stock can move around because “stocks” as a class move in and out of favor. Thus, there’s often a very strong disconnect between the price of the stock and what’s going on at the business. We all believe this, otherwise, we wouldn’t be on this platform. All of this can be frustrating, but also potentially profitable. We can make money if we spot the difference in expectations about the company embedded in the current price, and subsequent reality. So, if the market carries the stock of a company with poor results aloft because of “market up”, that discrepancy creates a potential profitable trade.

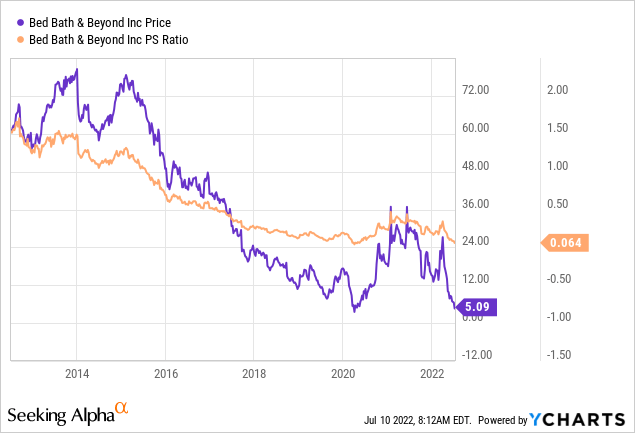

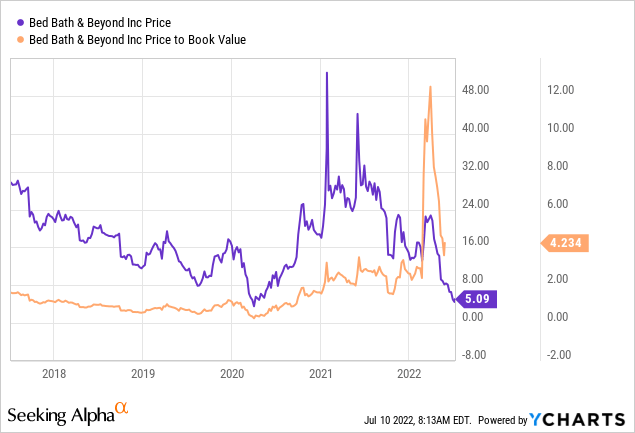

I should also point out that it’s typically the case that the lower the price paid for a given stock, the greater or “less bad” the investor’s returns over time. This idea shouldn’t need any explanation or elaboration. I measure the relative cheapness of a stock in a few ways ranging from the simple to the more complex. On the simple side, I like to look at the ratio of price to some measure of economic value, like earnings, sales, free cash, and the like. I like to see a company trading at a discount to both the overall market, and to its own history. In my previous piece on this name, the market was paying about $.20 for $1 of sales, and the shares were trading at a price to book of ~2.9 times. Fast forward a relatively short period of time, and the market is now paying about 6 ½ cents for a dollar of this company’s sales per the following:

At the same time, the price to book ratio has risen dramatically as book value has evaporated.

Given the above, I can’t recommend adding at current prices. Although I think there’s generally a disconnect between stock and business, I am compelled to suggest that people avoid this name until there’s some sign of a turnaround. I was seduced earlier by the strong insider buying and won’t make that mistake again. That brings me on to my next topic.

Insider Buying Activity

As I stated above, the market seems to have gotten excited about the fact that there have been three insider buys recently. In particular, recently Sue Gove, Harriet Edelman, and Jeff Kirwan bought 50,000, 10,000, and 10,000 shares, respectively. They paid between $4.61 and $4.90 per share for these purchases. I like to see such trades, obviously, because I like being on the same side of the table as people who know this business better than anyone else. At the same time, though, this experience has taught me that insider buys are not a sufficient precondition to take a position in a stock. There must be other identifiable positives, because there’s a risk that such activity is simply a means to goose the stock price higher.

It might also be interesting to start gauging the strength of…

Read More: Taking Lumps On Bed Bath & Beyond Stock (NASDAQ:BBBY)

{kind=link}