SrdjanPav/E+ via Getty Images

Uber (NYSE:UBER) ticked up in August as a better-than-expected earnings report coincided with broader recovery among tech stocks. While many investors might still think of UBER as the same cash-guzzling entity that it was when it came public, the reality is that this company has come out of the pandemic as a leaner machine with a stronger focus on profitability. UBER has given ambitious 2024 guidance that projects strong growth and a continued push towards sustained profitability. With 2023 shaping up to be a strong year for the company, the stock is worth buying at current prices.

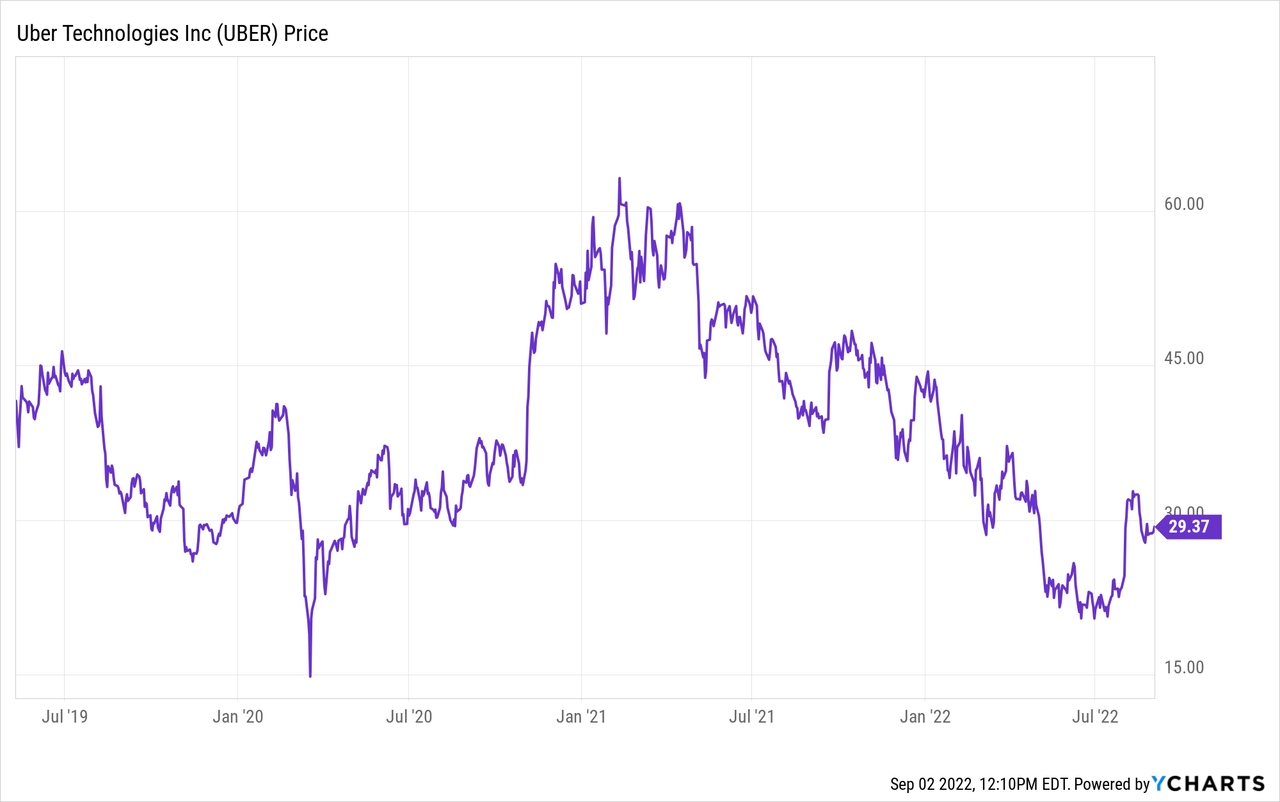

UBER Stock Price

After many periods of great volatility, UBER is now trading far below the $42 close on its first day of trading.

I last covered UBER in May where I compared it with Lyft (LYFT). Since then, LYFT has fallen over 20% whereas UBER has risen 30%, increasing the valuation discrepancy – though there remains important reasons to prefer UBER stock.

UBER Stock Key Metrics

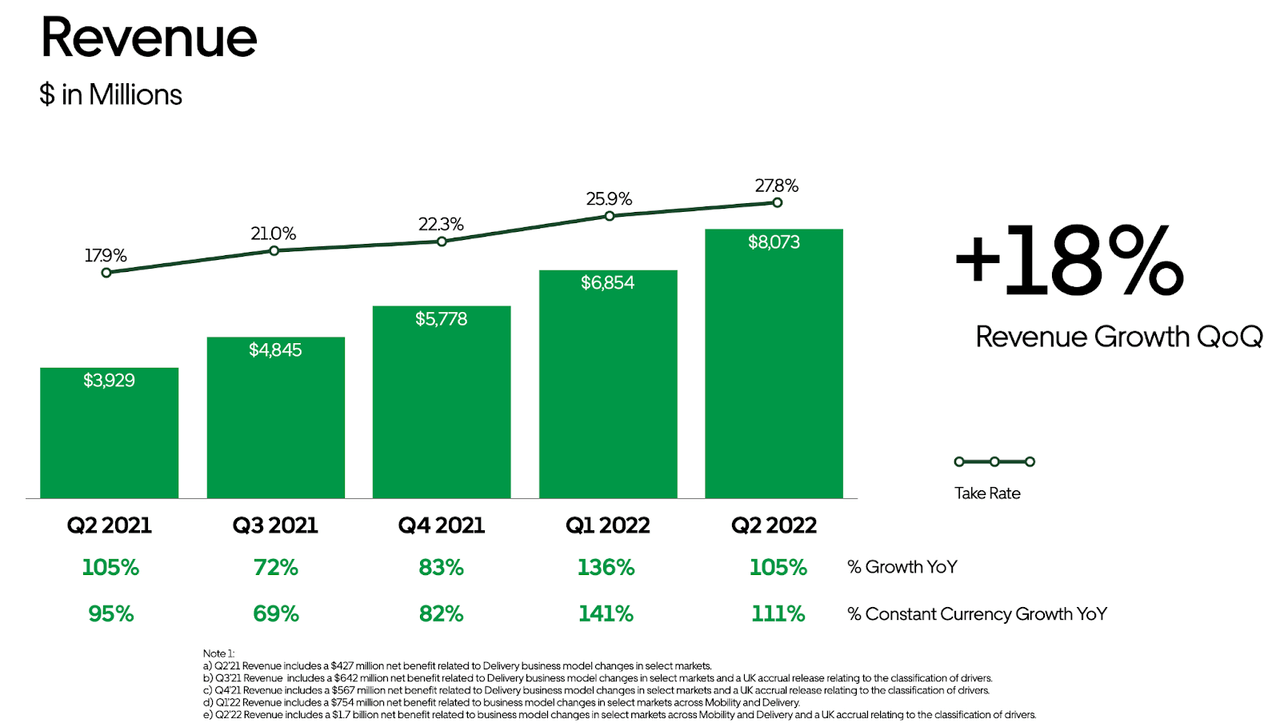

UBER’s latest quarter showed 111% year over year growth.

2022 Q2 Presentation

If you look at the above chart, you might think that this was due to take-rates expanding from 17.9% to 27.8%. In reality, the bulk of the “growth” was due to a $1.7 billion net benefit related to business model changes in various markets that was realized in the quarter. Excluding those net benefits, growth was around 82%.

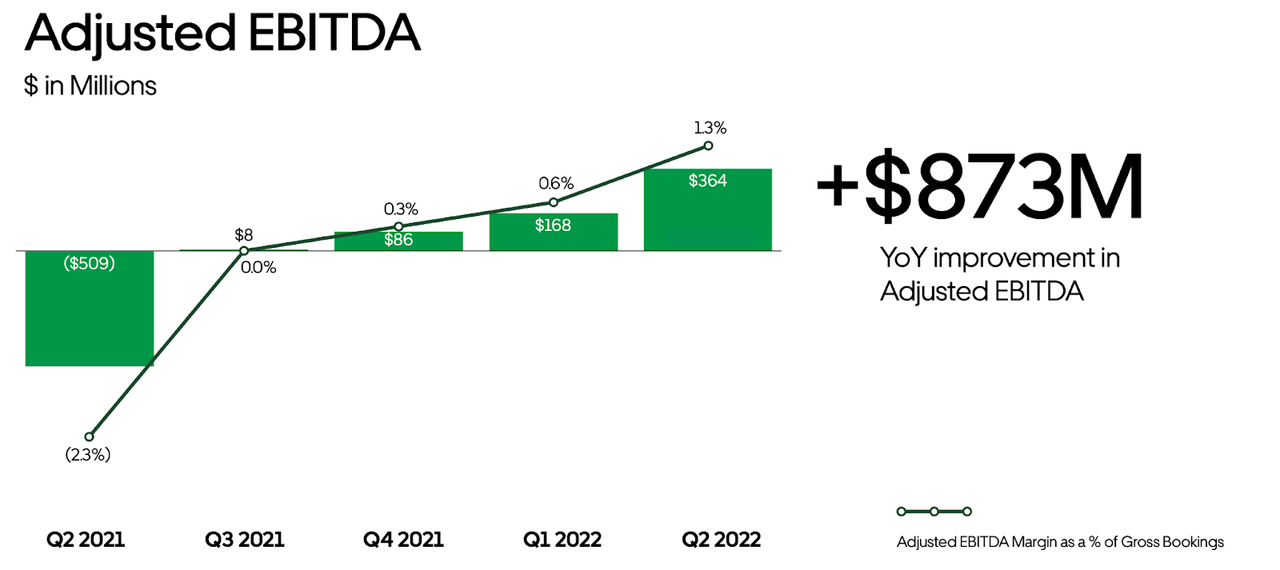

UBER did see adjusted EBITDA margins continue to expand, landing at 1.3% of gross bookings in the quarter.

2022 Q2 Presentation

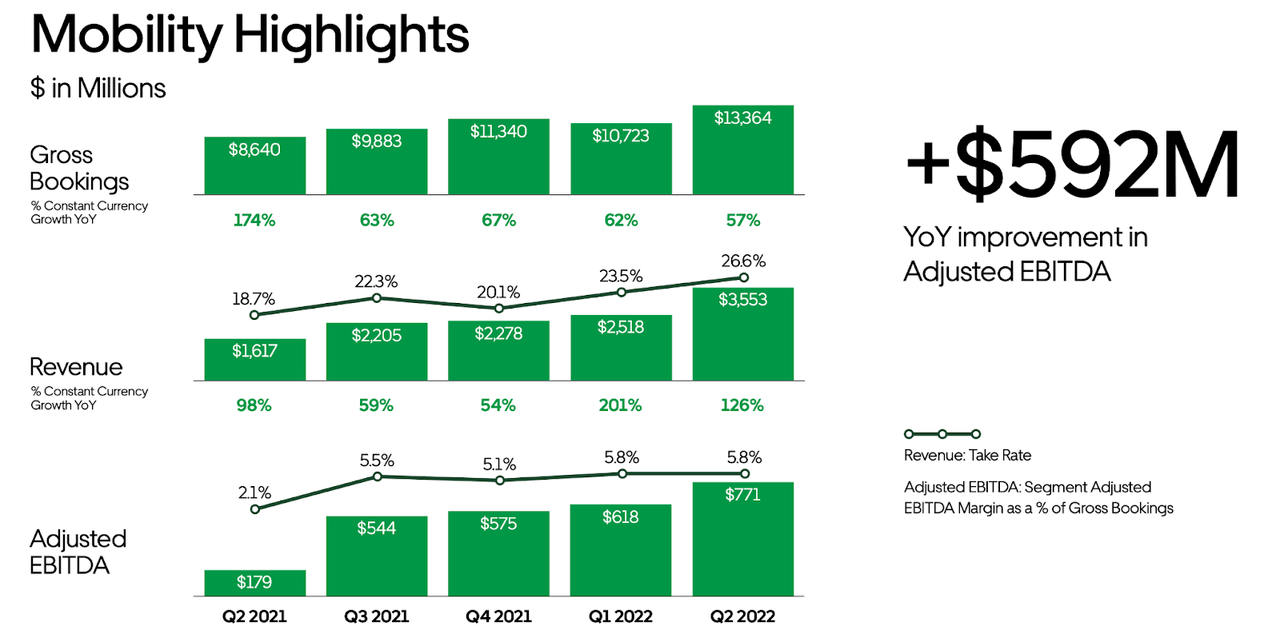

Recall that UBER primarily operates both its ride hailing mobility business and its food delivery businesses. Mobility revenues grew by 126% (it was the primary beneficiary of the aforementioned business model benefits) with solid 21.7% adjusted EBITDA margins (based on revenue).

2022 Q2 Presentation

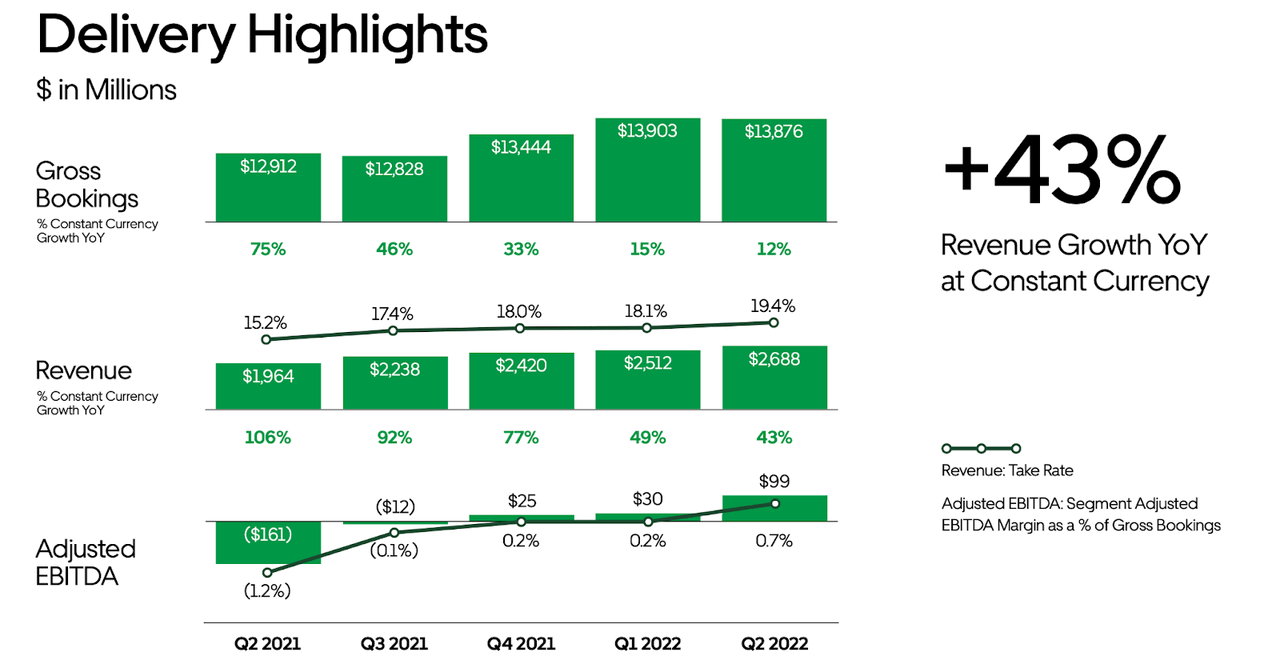

UBER’s delivery business delivered 43% year over year revenue growth – impressive considering that the company continues to lap tough comparables – though the adjusted EBITDA margin was lower at 3.7%.

2022 Q2 Presentation

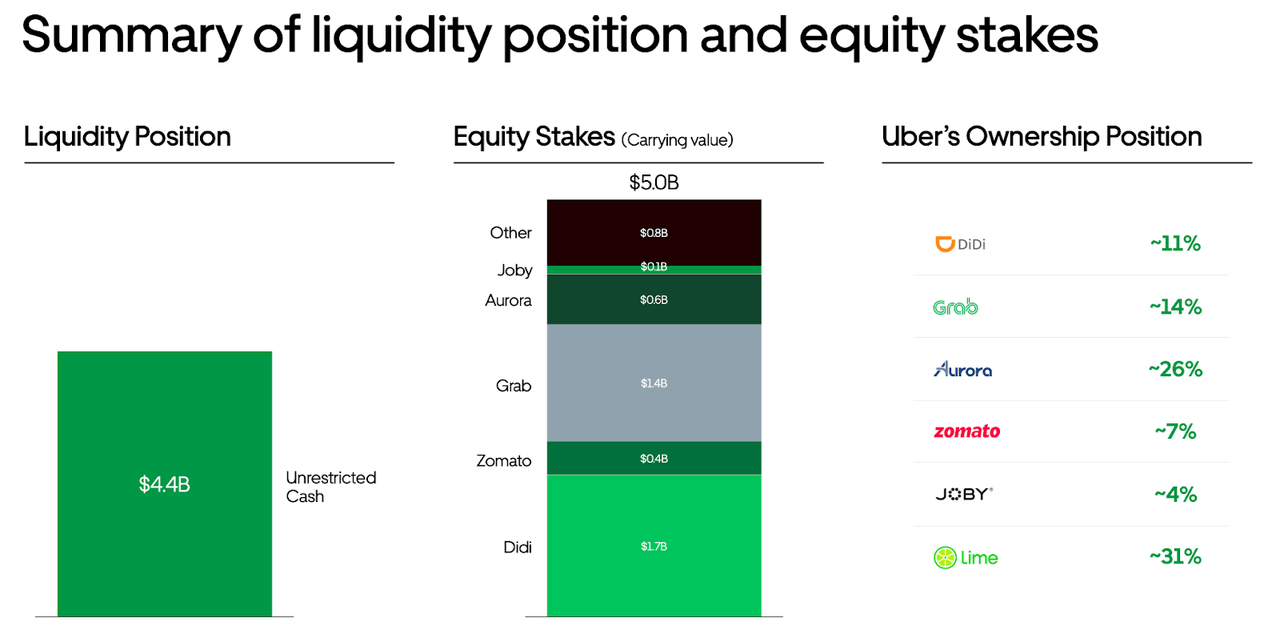

UBER ended the quarter with $4.4 billion of cash, $5 billion of equity stakes, and $9.3 billion of long term debt.

2022 Q2 Presentation

In a past life that would represent a precarious balance sheet position but that risk has dissipated with UBER now generating positive cash flows from operations.

Why Did Uber Stock Go Up In August?

It is possible that UBER rose in August due to the earnings report being stronger than expected, as perhaps some analysts were factoring in a larger impact from inflation. It is also possible that the stock rose alongside a surprise rally in the broader tech sector. In early August it was reported that longtime shareholder SoftBank has completely sold off its stake in the company – removing a potential overhang. UBER stock probably went up due to some combination of these three reasons.

Is Uber Stock Overvalued?

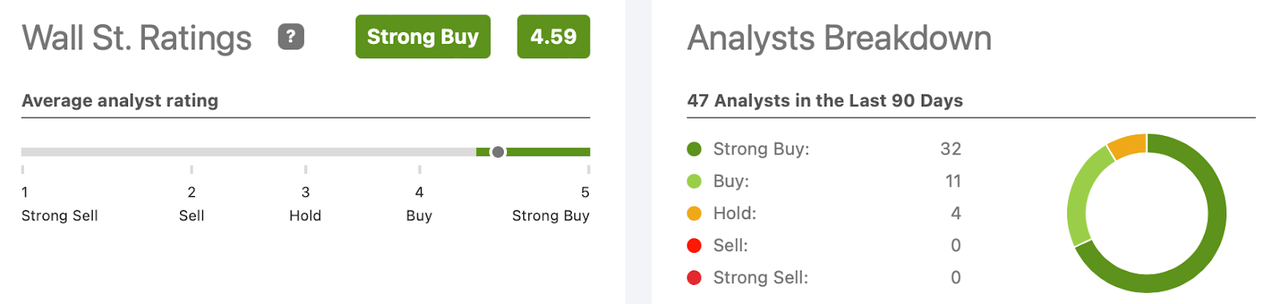

Even after the run-up, Wall Street analysts remain bullish on the stock, with an average 4.59 out of 5 strong buy rating.

Seeking Alpha

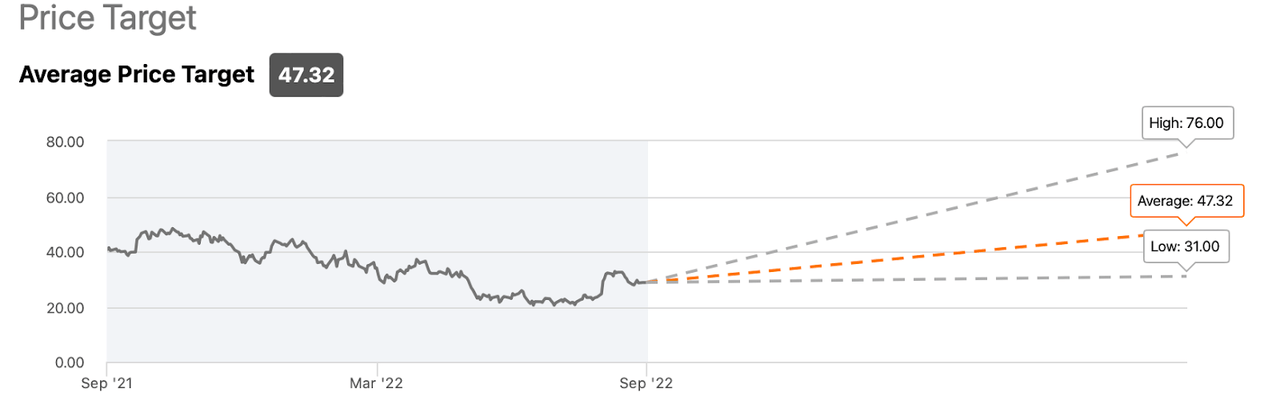

The average price target of $47.32 per share represents over 60% potential upside.

Seeking Alpha

What Should Uber Investors Consider?

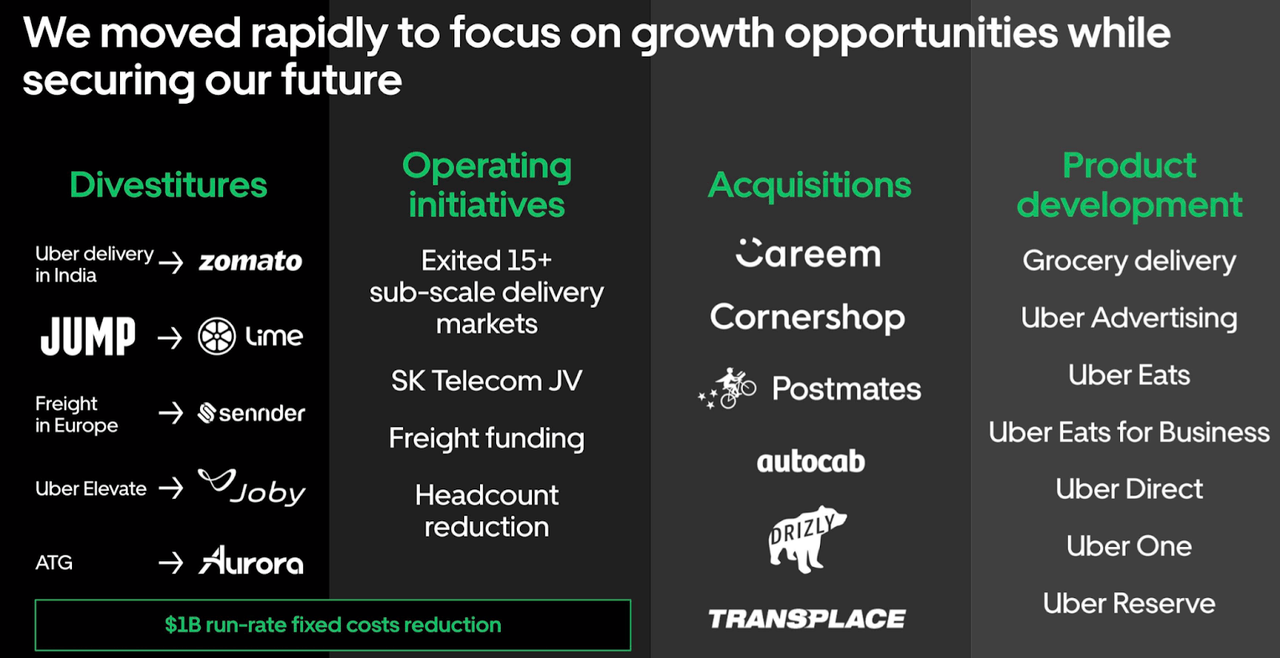

At this point, it is important to view UBER under the lens of its post-pandemic transformation. UBER had taken the pandemic as an opportune moment to critically examine its cost structure and priorities.

Uber Investor Day

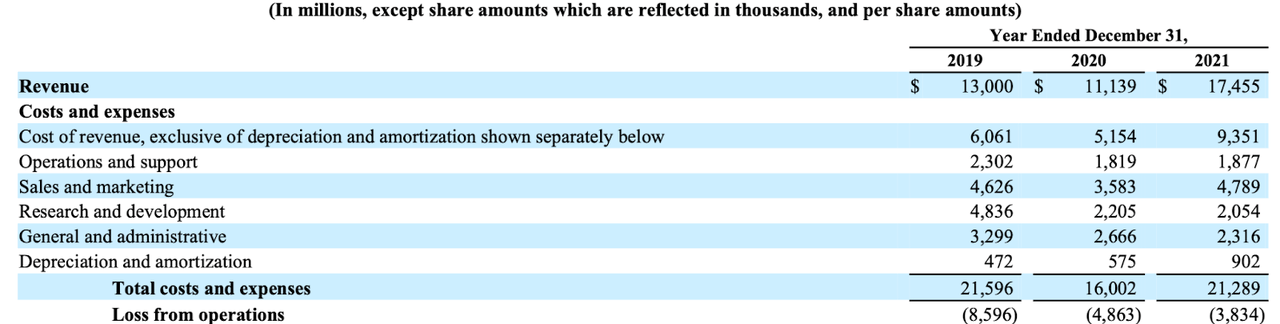

The net result was that the company was able to greatly reduce its fixed costs. Just compare the costs across the board between 2019 and post-pandemic – UBER has realized sizable cost savings in operations and support, research and development, and general and administrative.

2021 10-K

What Is Uber Stock’s Long-Term Prediction?

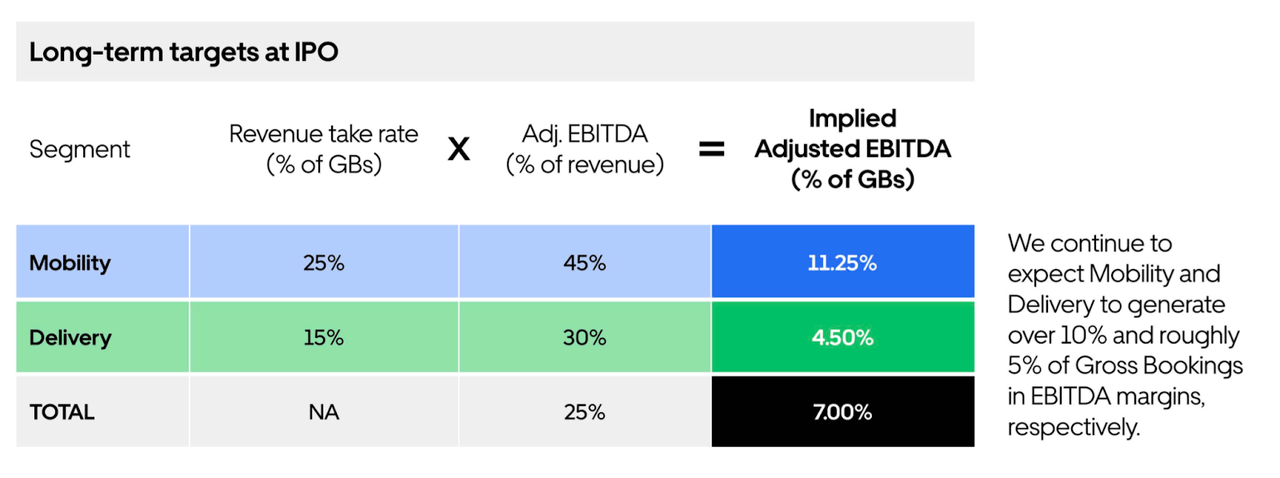

Over the long term, UBER has guided to over 10% EBITDA margins in Mobility and 5% margins in Delivery (based on gross bookings).

Uber Investor Day

That equates to roughly 40% margins and 33% margins (based on revenue) for mobility and delivery, respectively.

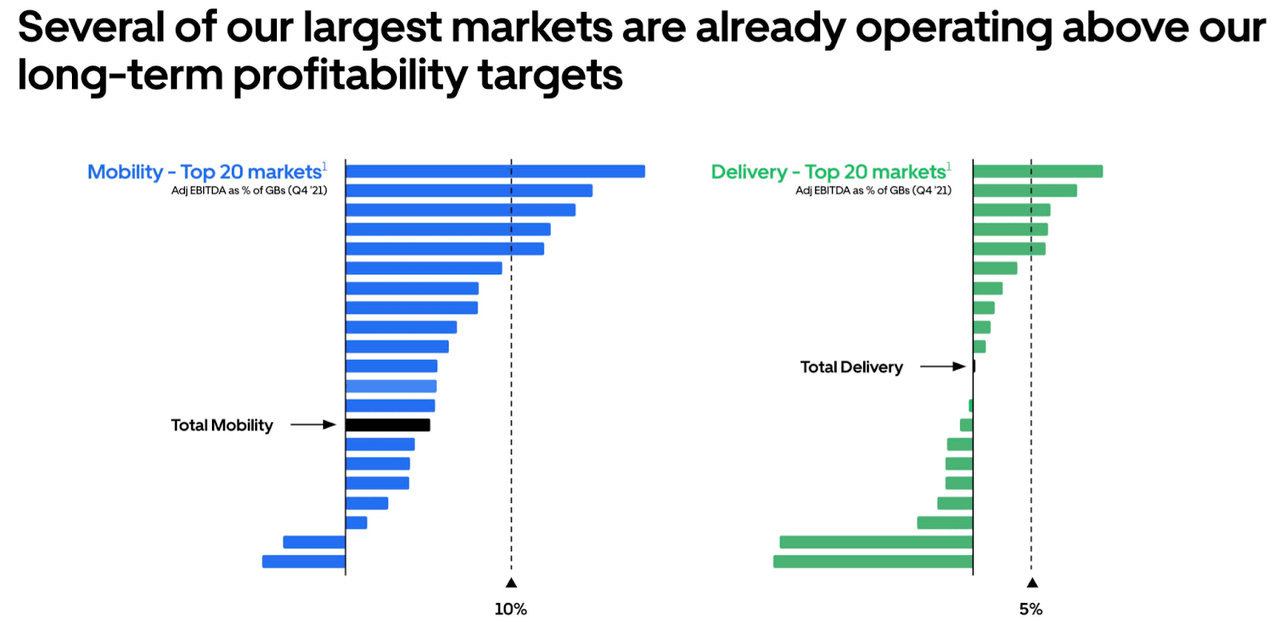

Those targets are arguably achievable considering that UBER is already operating above those long-term targets in some of their largest markets.

Uber Investor Day

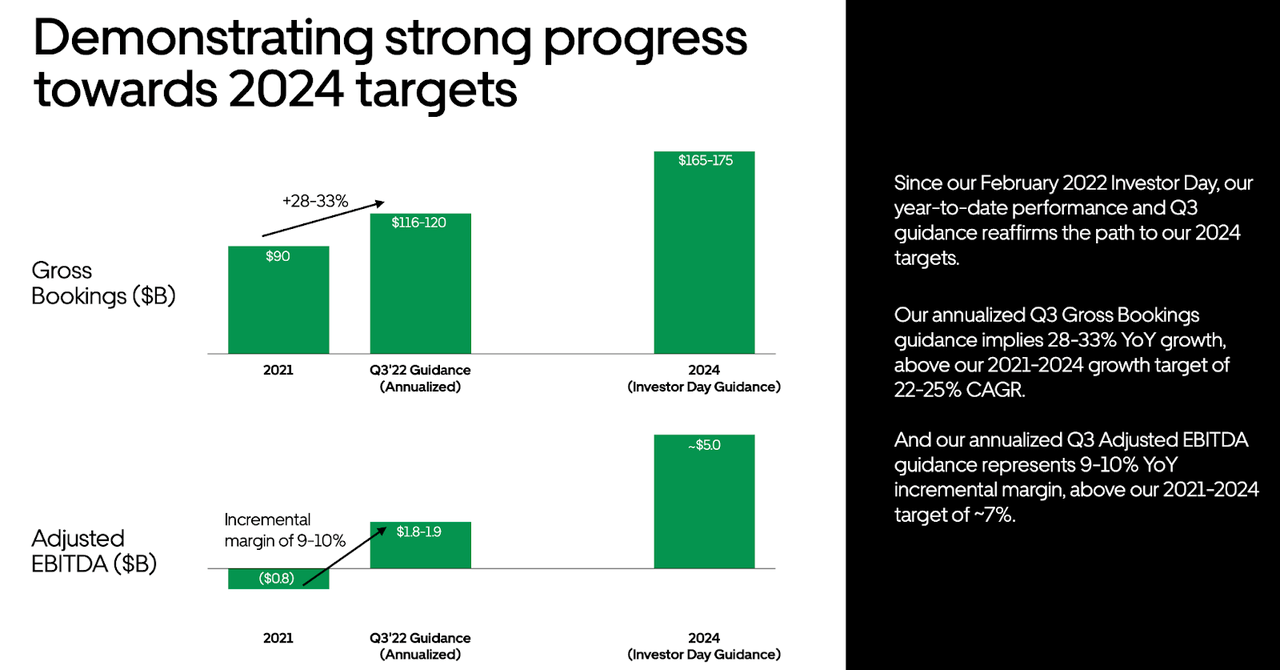

At its Investor Day, UBER gave ambitious 2024 targets for up to $175 billion of gross bookings and $5 billion of adjusted EBITDA, implying around 25% compounded revenue growth.

2022 Q2 Presentation

Is UBER Stock A Buy, Sell, or Hold?

That would have UBER earning around $47 billion in revenues by 2024. Consensus estimates are less optimistic, anticipating $44.5 billion of revenues.

Seeking Alpha

I assume that the company can achieve 20% net margins over the long term, far lower than the 33% to 40% implied by management. Applying a 1.5x price to earnings growth ratio (‘PEG ratio’), I could see UBER trading at 4.5x sales by 2024, equating to a stock price of $101 – far higher than current prices. Clearly, the projected upside hinges strongly on one’s margin assumptions and growth rates.

There are some key risks. While UBER has taken great strides to reduce its fixed cost structure, if another pandemic occurs, then it may face financial distress, especially considering that mobility remains its main profit driver. Another risk is that of competition. LYFT continues to grow rapidly as well and there remains the possibility that these two companies eventually compete on price, which would throw a wrench into long term margin assumptions. At the end of the day, it is very difficult to differentiate between the two services – at least that is just my anecdotal take. There is also the risk that local governments force UBER to treat its contractors as employees. UBER might be able to pass on some of the associated healthcare costs to the drivers, but even that may reduce driver demand. The stock is trading at compelling valuations here, even before accounting for the equity-rich balance sheet. I rate the stock a buy.

Read More: Why Did Uber Stock Jump In August? What’s The Future Outlook?

{kind=link}