RomoloTavani/iStock via Getty Images

Thesis

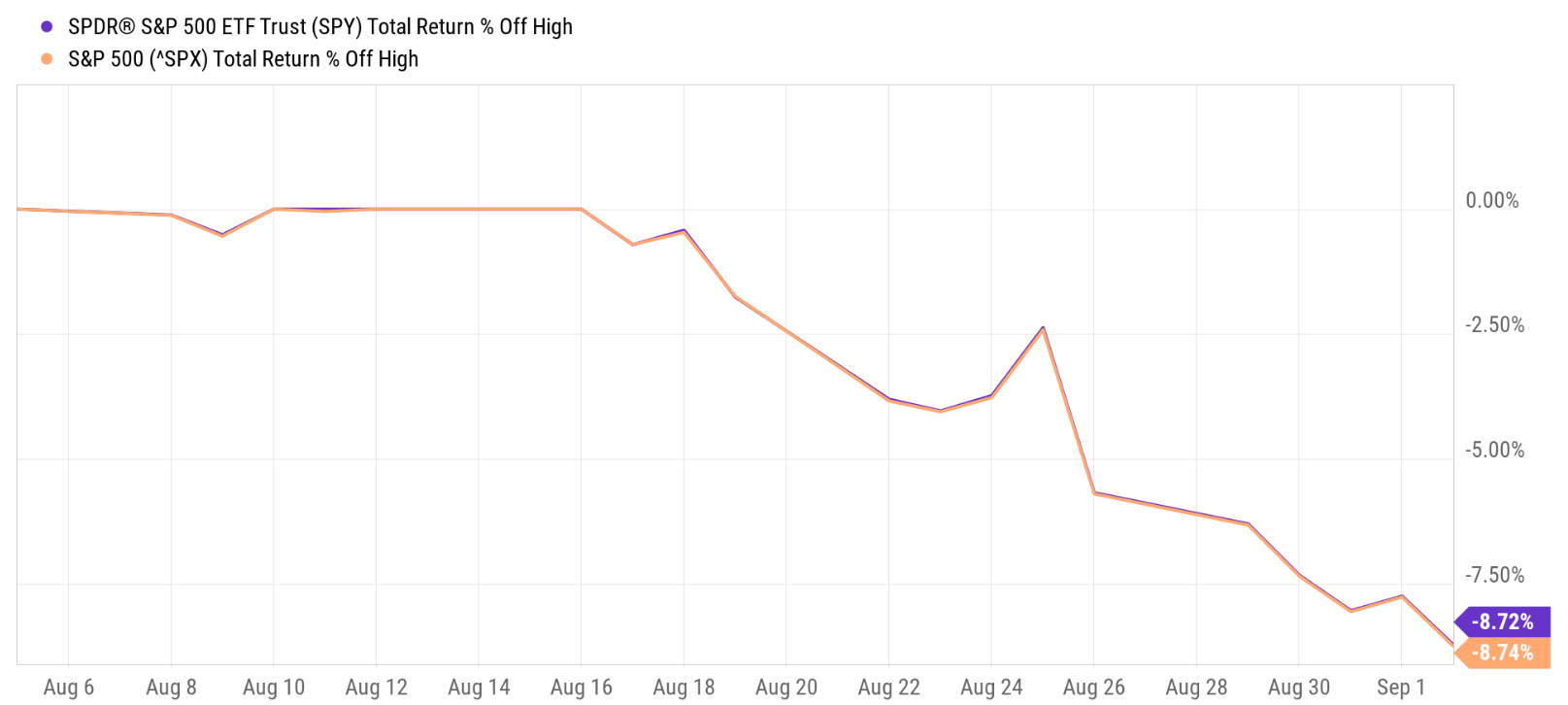

Lately, a frequently asked question in our Marketplace service involves the possibility of a recession. Our members are concerned about such a possibility, rightfully so, given the macroeconomic signals that appeared recently such as the inverted yield curve and GDP contraction. To add to the panic, the stock market has been sliding almost nonstop for three weeks as of this writing, with the S&P 500 losing about 9% from three weeks ago.

Source: Seeking Alpha

And therefore, I feel the need to share my thoughts on these popular signals, especially to point out their limitations, so that investors can make informed decisions suited to their individual risks profile. The main limitations to me are:

- The GDP contraction signal is more ambiguous and arbitrary and hence even less useful in my mind. For example, there’s a distinction between Gross Domestic Product (“GDP”) and Gross Domestic Income (“GDI”). And there has been an ongoing debate on which is a better representation of the overall economy. The debate is a moot point most of the time as they are usually close. But it becomes crucial when they are different, like what we’re experiencing now. To confuse things even more, the GDP and GDI data are currently not only different quantitatively but also directionally as you will see later.

- The inverted yield curve signal does not always work. There had been both false positives and false negatives from historical data as we will detail in a later section.

- And finally, even if the inverted yield curve or contracting GDP signals are reliable, they’re not too helpful for investment decisions because they are binary signals. As investors, it’s purely irrational to go out of equity when GDP contracted by 0.1% for two quarters in a row and to stay in equity when it expanded by 0.1% for two quarters in a row.

Due to these considerations, we’re currently still only making gradual adjustments based on our “business-as-usual allocation model.” And yes, we do have a “recession allocation model” as we hear a louder and clearer recession signal. We will share our action plan and trigger points that we monitor closely to decide when we should activate the recession allocation model.

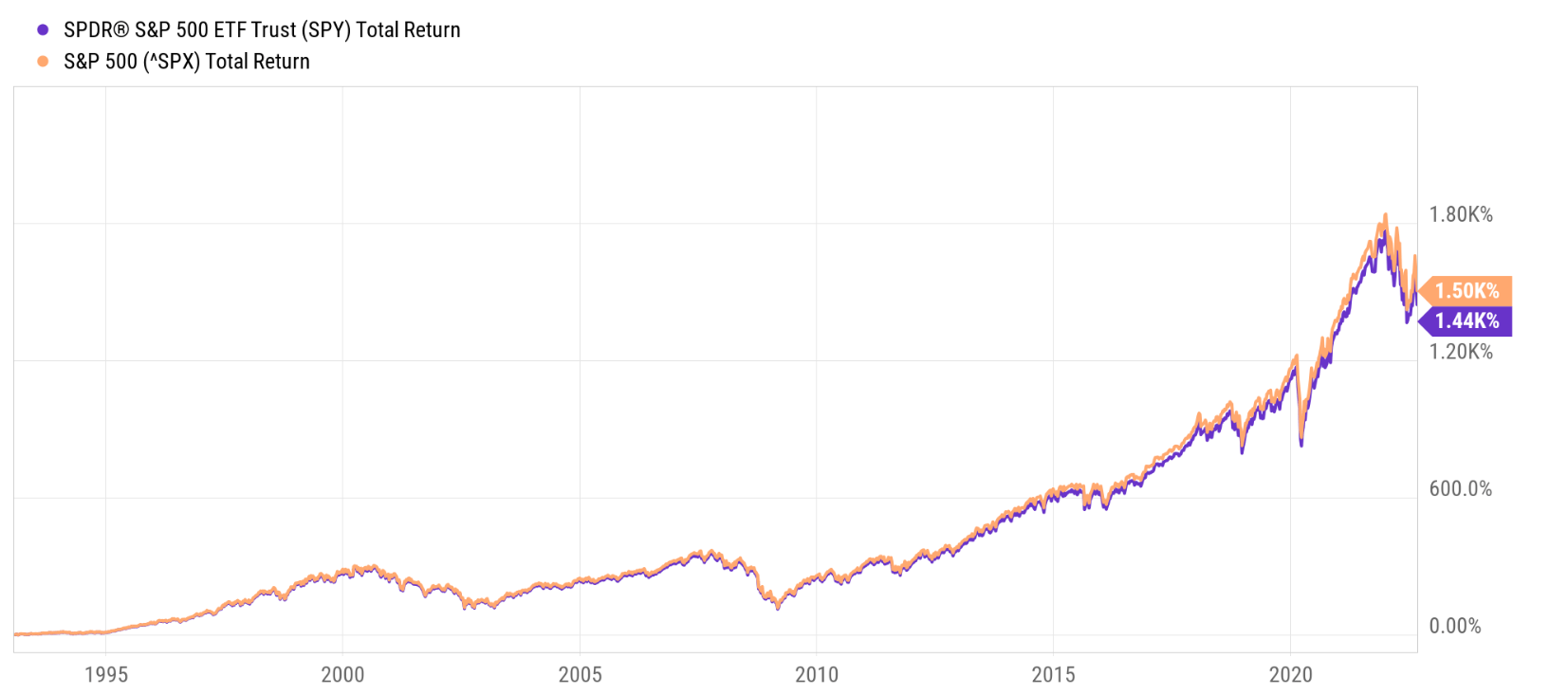

Before we dive in further, let me clarify that in this article, I will base my analysis on both the S&P 500 (SP500) and also the SPDR S&P 500 Trust ETF (NYSEARCA:SPY). Unless explicitly mentioned, this analysis will treat them interchangeably because the ETF does track the fund closely as we will see in the next section). And thus they provide the flexibility for me (and you also) to draw data from either the index or the EFT depending on which is easier and more accessible. Another advantage of basing the analysis on both the index and the EFT is that the ETF provides a more convenient vehicle for investors to express their views on the index.

SPY ETF vs. S&P 500 index

First, let’s establish the interchangeability of the S&P 500 and SPY. The goal of the SPY fund is simply to mimic the S&P 500 Index as stated in the fund description:

- The SPDR® S&P 500® ETF Trust seeks to provide investment results that, before expenses, correspond generally to the price and yield performance of the S&P 500® Index (the “Index”).

- The S&P 500 Index is a diversified large-cap U.S. index that holds companies across all 11 GICS sectors.

And thanks to its long history (it was launched in January 1993), it provides more than three decades of data publicly and is easily accessible to most investors. And from the following chart, you can see that despite issues like fees, dividends, and tracking errors, its price followed the index closely in the long term. Since its inception in 1993, the S&P 500 Index returned 1440%, and the SPY fund returned 1500%. The difference is only 60% after more than three decades of accumulation, translating into about 0.1% per year. Given this extremely small discrepancy, I will use S&P 500 or SPY data, whichever comes more convenient, in the rest of the analysis.

Source: Seeking Alpha

Ambiguity of the GDP and GDI data

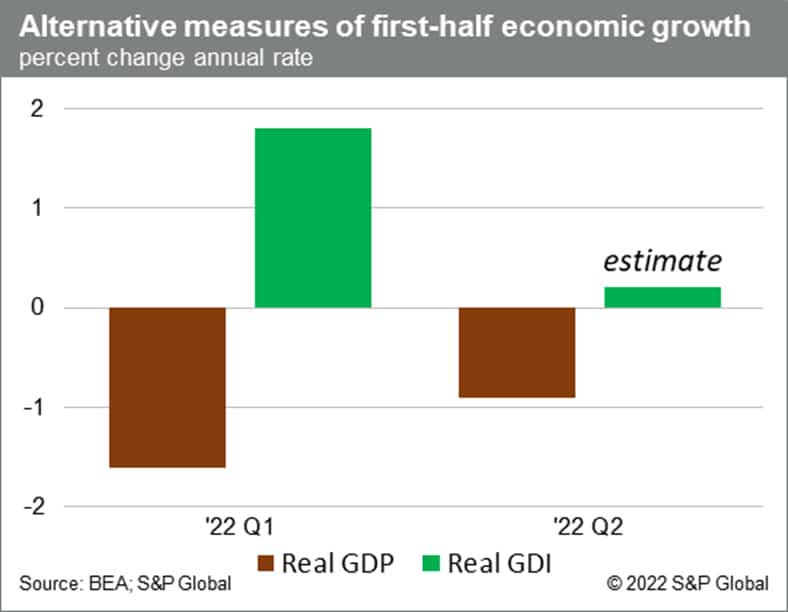

The Bureau of Economic Analysis (“BEA”) reported in July that U.S. economic output as measured by GDP shrank for two consecutive quarters in the first half of this year. To wit, real GDP fell by 0.9% in Q2, following a 1.6% decline in Q1. Two consecutive quarters of negative GDP growth meet the popular (though not official) definition of a recession. And then new data released since then, especially the GDI data, sent a different signal as you can see from the chart below. As measured by GDI, the economy expanded by about 1.8% in Q1 and is estimated to expand by another 0.1% in Q2.

A bit of background on GDP and GDI. They’re both common measures of economic output (even though GDP is more often talked about). And in theory, they should be equal because they measure the economy from two equivalent ends – for every $1 person A spent on a certain good or service, person A would be making $1. GDP reflects person A’s spending on the transaction, while GDI reflects person B’s income of the same transaction.

However, there’s always statistical error because the datasets and data sources used to compute GDI and GDP are different. Thus far this year, the statistical error has not been unusually large quantitatively but also different directionally as seen in the chart. And one of the main causes is the highly inflationary environment we are experiencing now.

Given such ambiguity, I do not see reasons for investors to panic because of the GDP data. The economy might be far away from a recession (and closer to stagnation). Furthermore, as aforementioned, even if contracting GDP data is conclusive and unambiguous, it won’t be too helpful for investment decisions because it’s a binary signal.

And so is the inverted yield curve signal as we will discuss next.

Source: BEA and S&P Global

Limitations of yield curve signal and alternatives

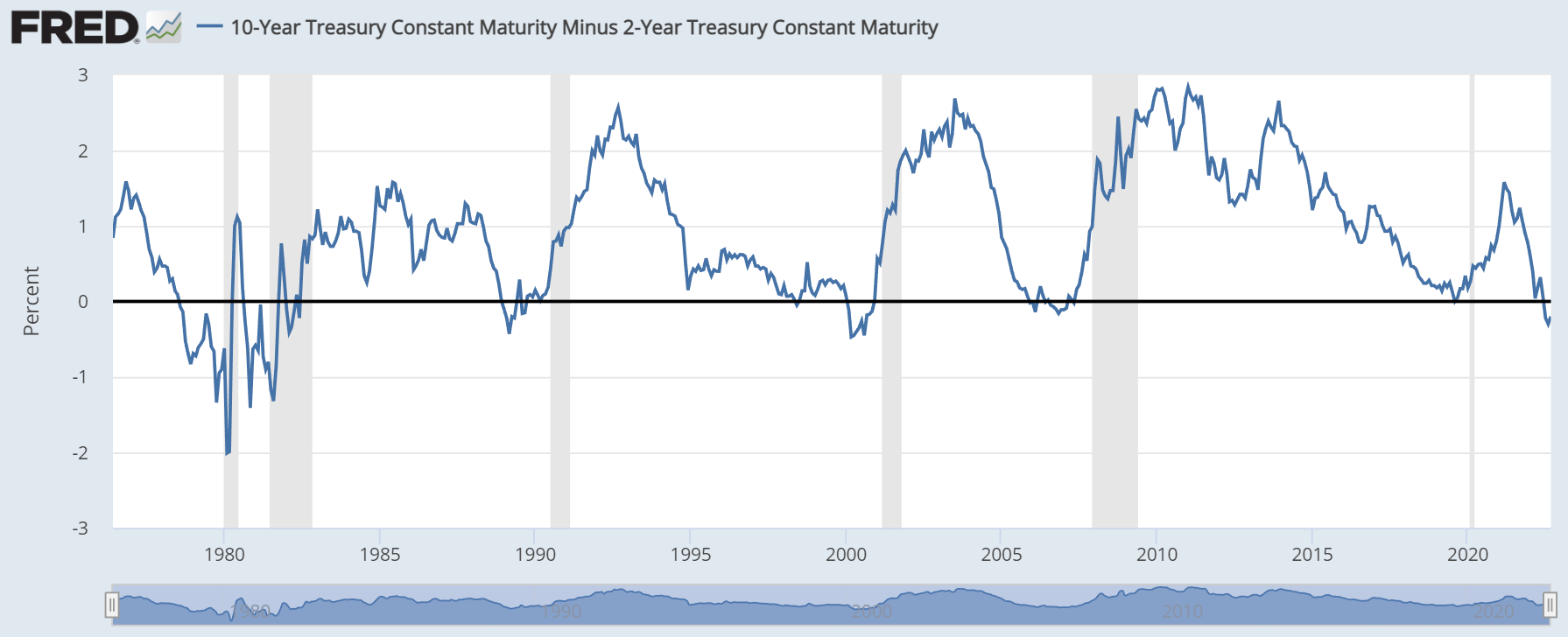

Most investors are familiar with the dreaded yield curve inversion as shown below (a plot of the spread between 10-year Treasury rates and 2-year Treasury rates). At first glance, you can see that since the 1970s, there were six recessions (highlighted by the great bars). And all six had been preceded by a yield curve inversion. So, the success rate of this signal is 100% in the past 50-plus years. And this dreaded inversion has happened repeatedly in the past few months. The yield curve inverted briefly back in April 2022 as the 10-year Treasury rates dipped below the 2-year Treasury rates briefly (so brief that you can barely see it in the following chart). Then the inversion occurred in earnest in early July shortly after the Fed announced its intention to continue its hawkish plan. The spread between 10-year Treasury rates and two-year Treasury rates has remained negative since July 5, reached a bottom of almost -0.5%, and currently stands at -0.20%.

Source: FRED

Given the popularity of the yield-curved signal and hence the heightened anxiety we’ve seen among our members, we feel timely to point out the limitations too. As detailed in an earlier article:

- The sample size of past recessions is too limited to be statistically significant. As mentioned above, there were only 6 recessions in the past 50-plus years. Expanding the timeframe broader, there were 19 noteworthy recessions throughout U.S. history.

- The signal does not always work. There had been both false positives and false negatives even among the limited sample set. Some recessions happened without a preceding signal, and vice versa.

- The signal does not tell you when a recession would happen. Many times, the equity market has staged substantial rallies after the signal occurs for an extended period of time. In the long term, missing out on such rallies hurts more than avoiding the recessions (even if you indeed manage to do so).

Finally and most importantly, just like the GDP signal, the signal is binary. As such, it offers little actionable guidance. Investors cannot go all-out of equity because the yield spread dipped below zero (like in April) and then come back to equity when the yield spread surfaces above zero a few days later.

Investors need a signal that provides more granularity. And we will describe two simple ones that you can obtain from publicly available data immediately below.

Alternative signal No. 1

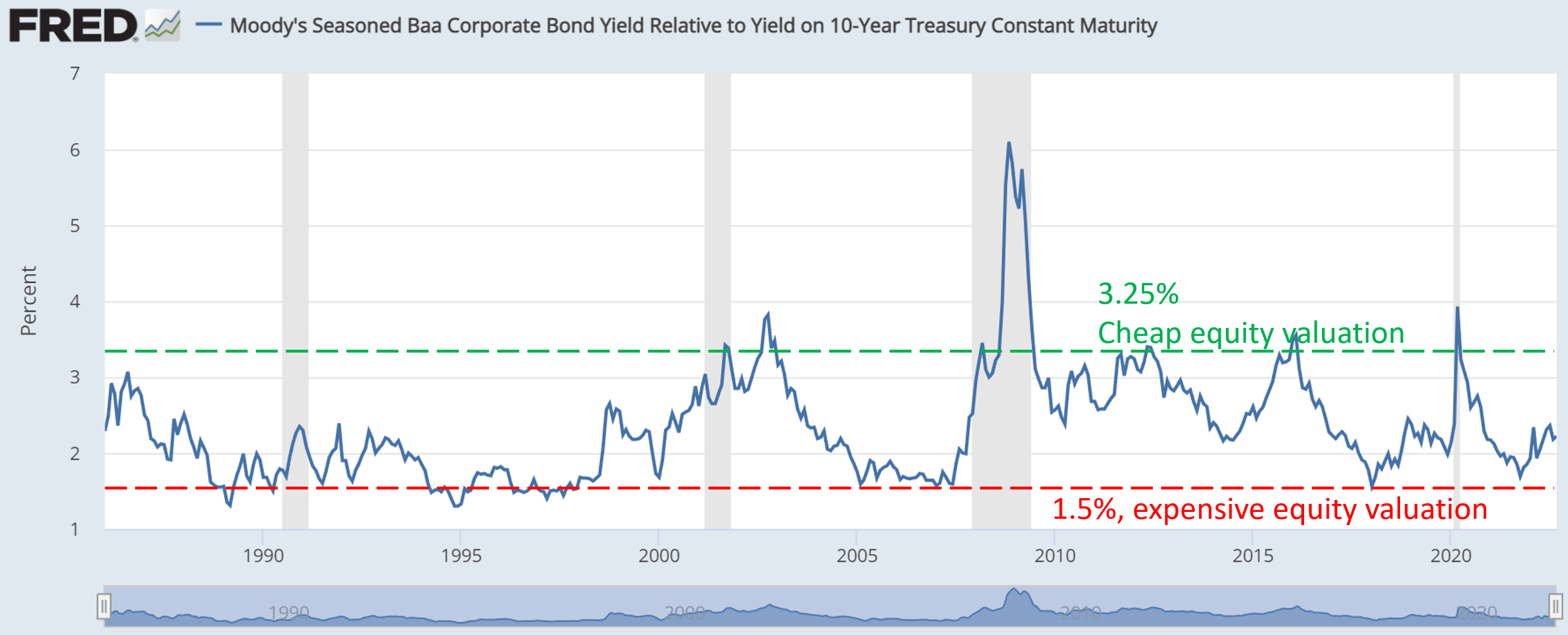

The first easy signal involves the yield spread between BAA corporate bond and risk-free rates such as the 10-year Treasury rates as shown below. Such yield spread tells how the market prices corporate bonds (which is a reliable indication of equity valuation) relative to risk-free rates. And since the bond market usually sniffs out problems more sensitively, this signal provides a more accurate indicator. The yield spread has been consistently tractable within a range of about 1.5% to 3.0% in the long term and thus provides investors with the granularity they need. It doesn’t only tell you whether equity is expensive or not. It tells you the degree of its overvaluation or undervaluation, so you can fine-tune your equity exposure.

Currently, the BAA yield is about 2.2% above 10-year rates. And the long-term historical average is around 2.34%. So the current yield spread between the BAA yield and treasury yields is a bit below the historical average (i.e., equity is a bit towards the more expensive spectrum). But the premium is totally within the normal range of historical oscillations, and I see no reason to panic.

Source: FRED

Alternative signal No. 2

The next signal is based on the yield spread between SPY and risk-free interest rates. As detailed in our earlier article:

- The common PE or Price/cash flow multiples provide partial and even misleading information due to the differences between accounting earnings and owners’ earnings.

- Dividends provide a backdoor to quickly estimate the owners’ earnings. Dividends are the most…

Read More: Recession Assessment And Action Plan Using S&P 500 And SPY Data

{kind=link}