Bill Pugliano/Getty Images News

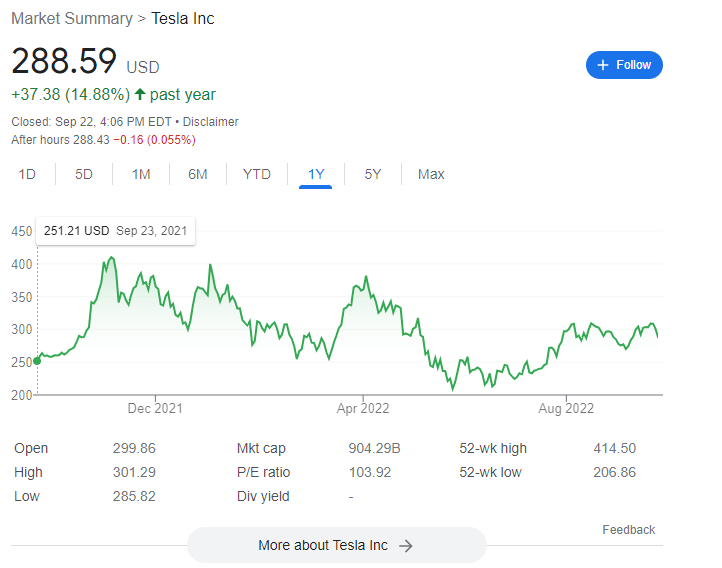

TSLA has had a great run over the last 5 years and despite the sell-off YTD, if you had invested 1 year ago you would still be up 20%. Strong leadership from Elon Musk combined with retail fervor and growing institutional acceptance have led to TSLA vastly outperforming the market for several consecutive years. While I am a fan of Musk and a believer in his vision and TSLA as a company long-term, I think the current macroeconomic environment presents substantial headwinds and TSLA stock is primed to underperform.

Google Finance

Commodity Prices / Macro

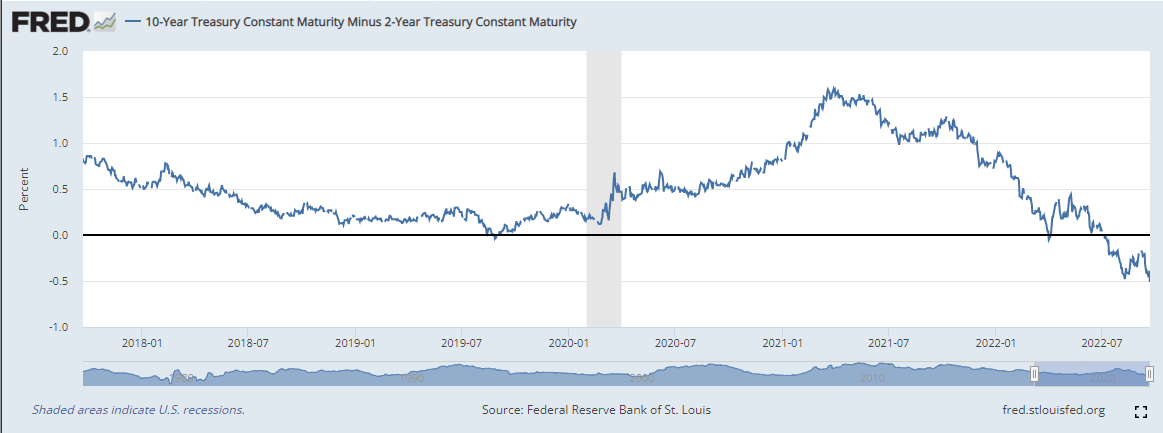

I’ll start off this section with one of my favorite charts that continues to get more bearish – 2s/10s spread.

FRED

As I’ve detailed in other articles (see: A Recession Is Inevitable, Don’t Get Fooled By Bear Market Rallies), the 2s/10s spread inversion has a 100% track record of predicting a recession in the US since the 1970s and after Chair Powell’s continued hawkishness this week, it is likely that the curve will become more inverted.

Bloomberg

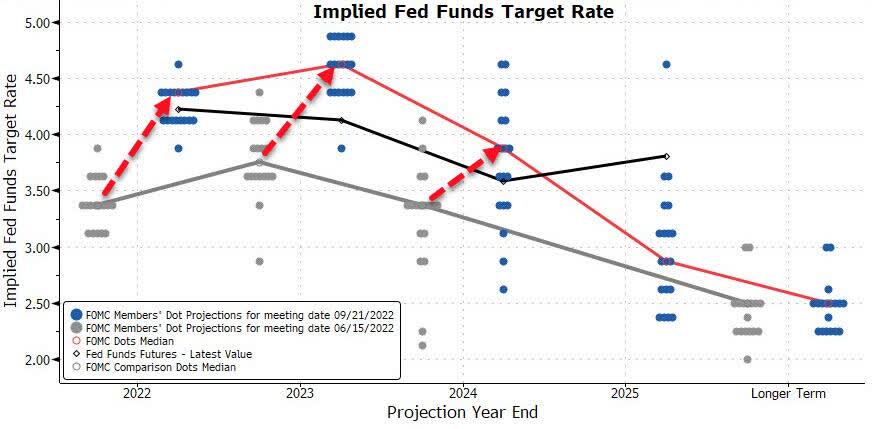

While market expectations (i.e., fed funds futures) are slightly less hawkish than the dot plot, the dot plot and fed funds futures moved up substantial on this week’s Fed meeting. Not only are financial conditions extremely tight already, but they are going to get even more tight in the coming weeks. This is bad news for a cyclical, high growth business like Tesla.

FRED

FRED

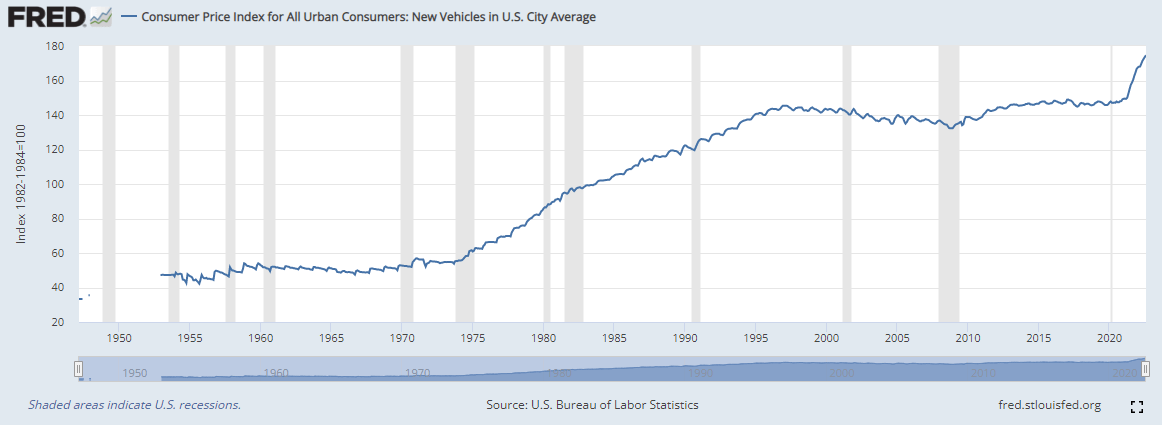

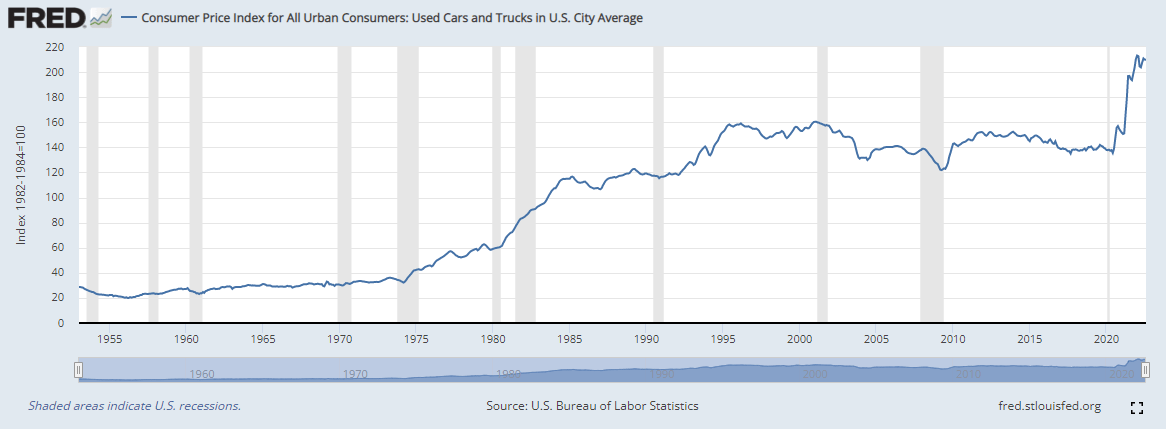

The magnitude of car price increases both for new and used cars in 2021 was astounding. Both of the indexes were roughly flat for 25 years from 1995 to 2020 and then increased over 20% (almost 50% for used cars) in 2021 driven by low rates and home nesting / work-from-home trends which encouraged car ownership particularly during the COVID lockdowns. Car sales (like other consumer durables) are very sensitive to rate increases (Powell said as much himself in his congressional testimony in June) and there is likely to be substantial mean reversion in these sales.

FRED

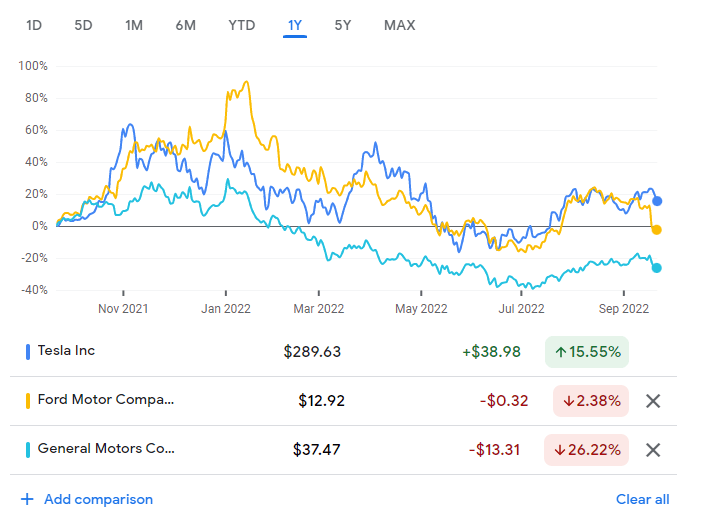

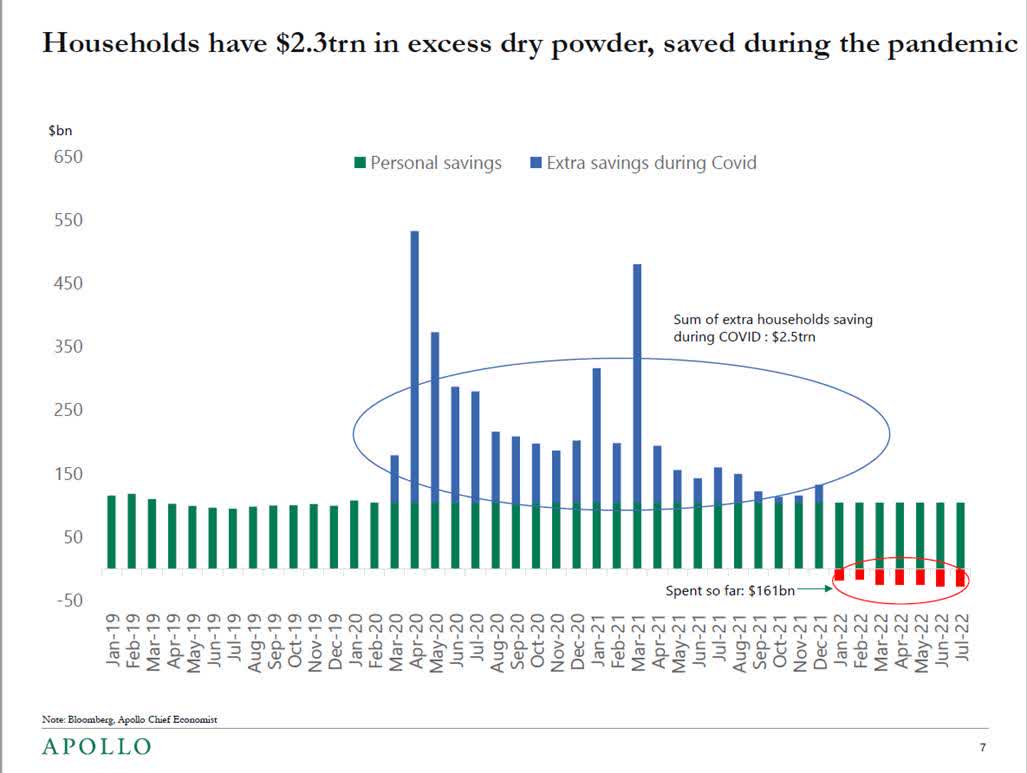

Ford and GM have already begun to price in some of this bearish outlook, notably with Ford’s bearish guidance update earlier this week, but Tesla was relatively unmoved. This again strikes of overly optimistic fervor around this stock, but I would caution that Tesla will be subject to the exact same bearish headwinds as the rest of the auto industry. Not to mention that premium products typically display a greater wealth effect than cheaper alternatives and should thus suffer more in a recession (this has not played out so far, as income has not fallen off substantially yet). Overall the consumer is still strong and has ample savings (particularly the wealthy consumer) but already housing pricing are showing signs of weakening which is often the greatest source of wealth for many middle and upper-middle income consumers, and households have stated to dip into COVID savings. I believe demand destruction will begin to occur in this category in the next 6 months.

Apollo

Zillow

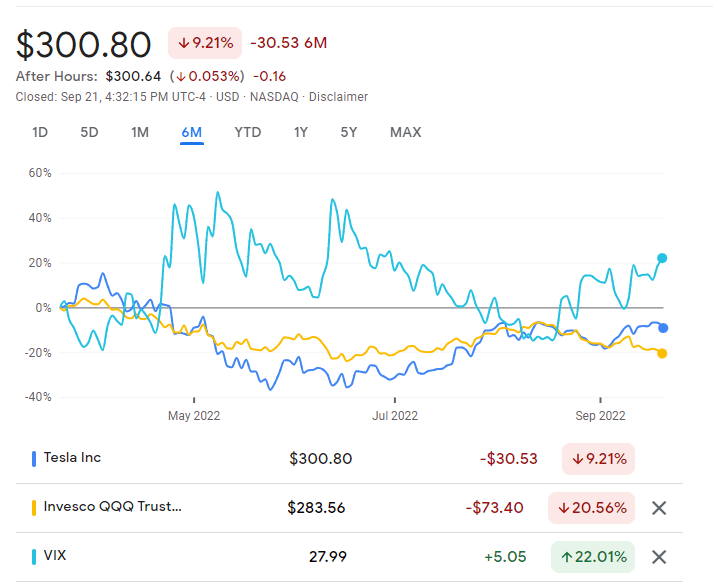

The only brief periods of underperformance for TSLA shares have come during periods of heightened market volatility and fear. This is congruent with my view that TSLA is a relative “bubble” (I know this is a dirty word around TSLA investors but works well in this situation) and during periods of high uncertainty, underperformance should accelerate as investors are less able to sustain their “greedy” expectations.

Google Finance

VIX is near the bottom of its channel currently (note VIX peaking >80 in the last two bear markets and is still near its long-run average currently). This is a further sign of market complacence.

Google Finance

Google Finance

Zooming in on Tesla

Overall, I’ve been very impressed with Tesla’s business performance in 2022. Tesla has done an excellent job of ramping production in 2022 despite production setbacks in Shanghai. Berlin production has already exceeded 1,000 cars per week, and production in Austin is set to pass 1,000 cars per week soon. Battery production credits from the Inflation Reduction Act should also provide a boost to margin for the next few quarters, and additional cost savings will be realized from ramping up of the Austin and Berlin factories. Profitability has ramped up nicely with LTM EBITDA margin at ~21% and finally catching up in quantum to peers F and GM. TSLA has also substantially improved its cash balance, increasing to over $18B in Q2. Production and deliveries are up substantially YOY despite the supply chain setbacks.

Tesla has negative net debt currently and given the business’s improved profitability profile, there is essentially zero insolvency risk. While TSLA has been reluctant to issue more shares in the past few years, that option is always on the table and TSLA’s premium valuation is a massive competitive advantage over competitors via its lower cost of capital. This is part of the Elon Musk halo effect and is part of the reason why I’m a long-term believer in the business – Elon is a master at gaining the favor of capital markets.

I have almost nothing negative to say about the business in its current state. I do think that the market is somewhat complacent about the risk of competition from other automakers entering the EV market. Given the market’s favorable sentiment toward EVs, I would expect competition to generally increase in the coming years (this is not to mention increased competition from Chinese EV makers in the China market). I don’t have a strong opinion on Tesla’s market share, and I think the massive TAM for EVs will present plenty of opportunity for Tesla to profit in the future. I am not an expert, though, and I’m certain many reading this article and other commentators have better opinions on the consumer tastes and industry competition.

Valuation

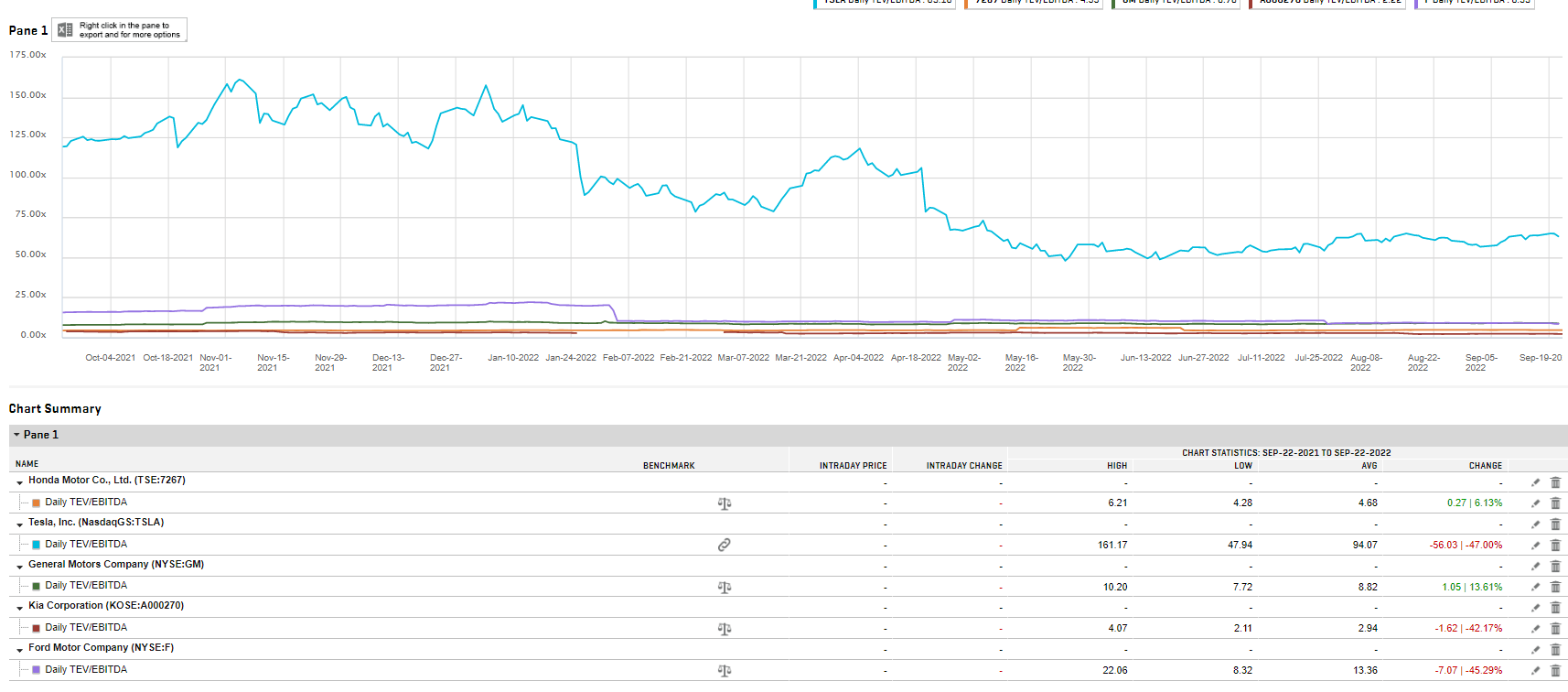

I’m also certain bulls are tired of bears pointing to valuation disparities as they simply have not mattered for the past three years, but it goes without saying that TSLA trades at a massive premium to its peers in the industry (a premium gap that has closed somewhat as TSLA profitability has improved). Where this gap starts to matter is when the industry starts to sell off as a whole, the high-flyers will typically see their multiples contract more on an absolute basis as the spread between the winners and losers shrinks.

S&P Capital IQ

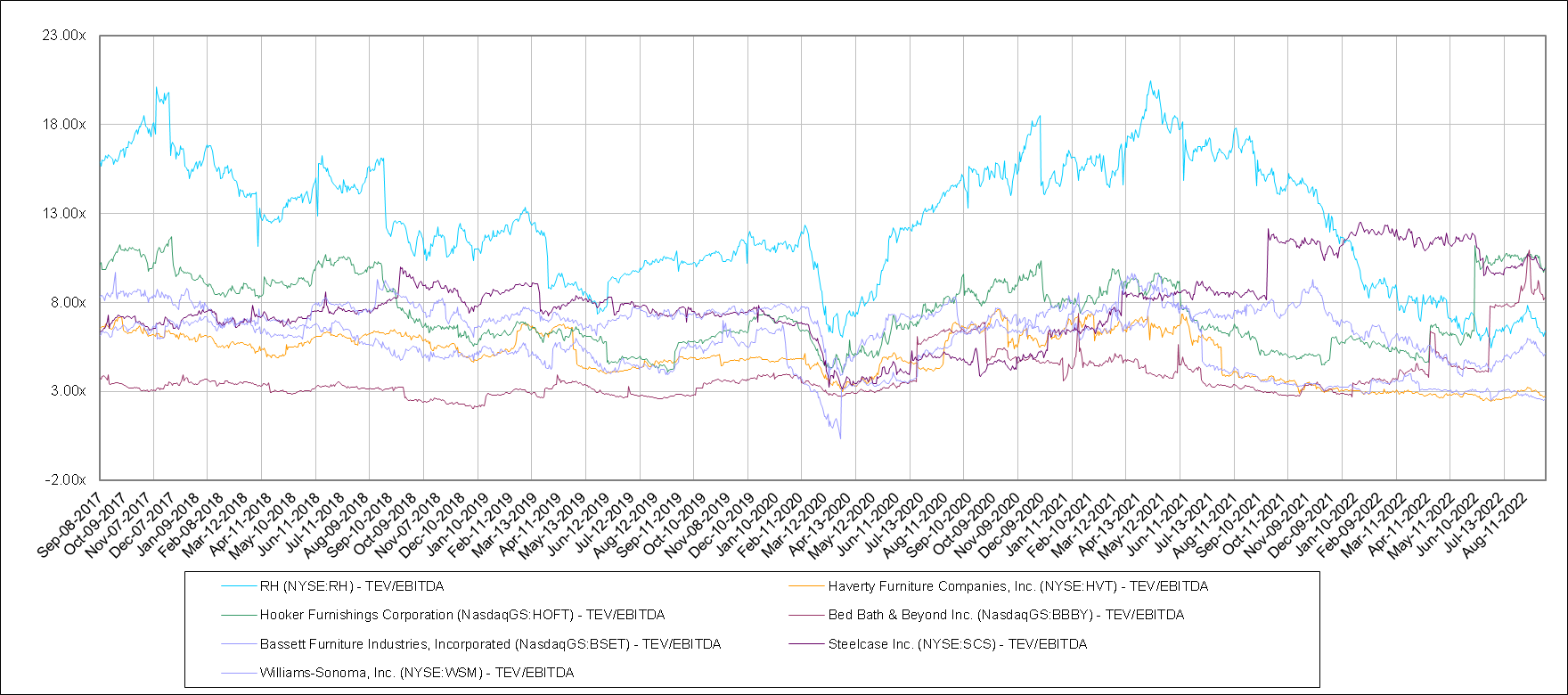

A great example of this is RH in the furniture industry, an industry which is similarly discretionary and rate sensitive (can see my RH article for additional commentary). RH traded at a substantial premium to the rest of the furniture industry for almost two years due to its premium brand reputation and operational excellence, but as the entire industry has sold off, RH has seen its multiple contract the most relative to its peers. While I don’t see TSLA ever trading below any of its peers on a multiple basis, I do see the potential for the relative pain to actually be greater for TSLA as the industry contracts (assuming my call for the industry to contract is correct).

S&P Capital IQ

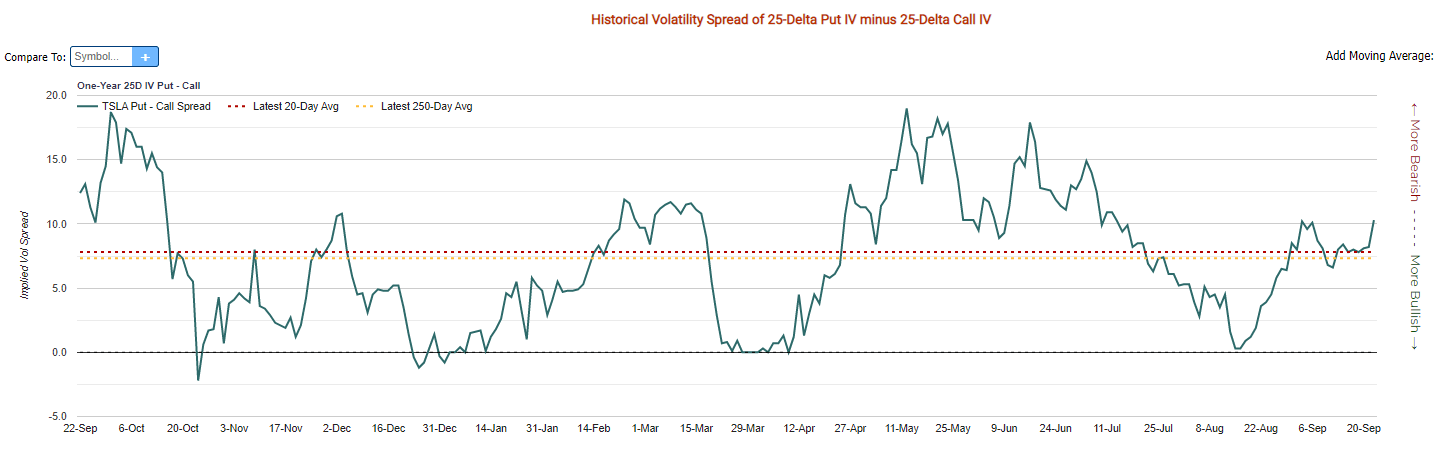

TSLA Put/Call ratio is slightly below market which stands near 1.00 currently and short interest in TSLA is low at 2.32% indicating some relative complacency among investors given the meteoric rise of TSLA shares over the past 3 years.

Barchart.com

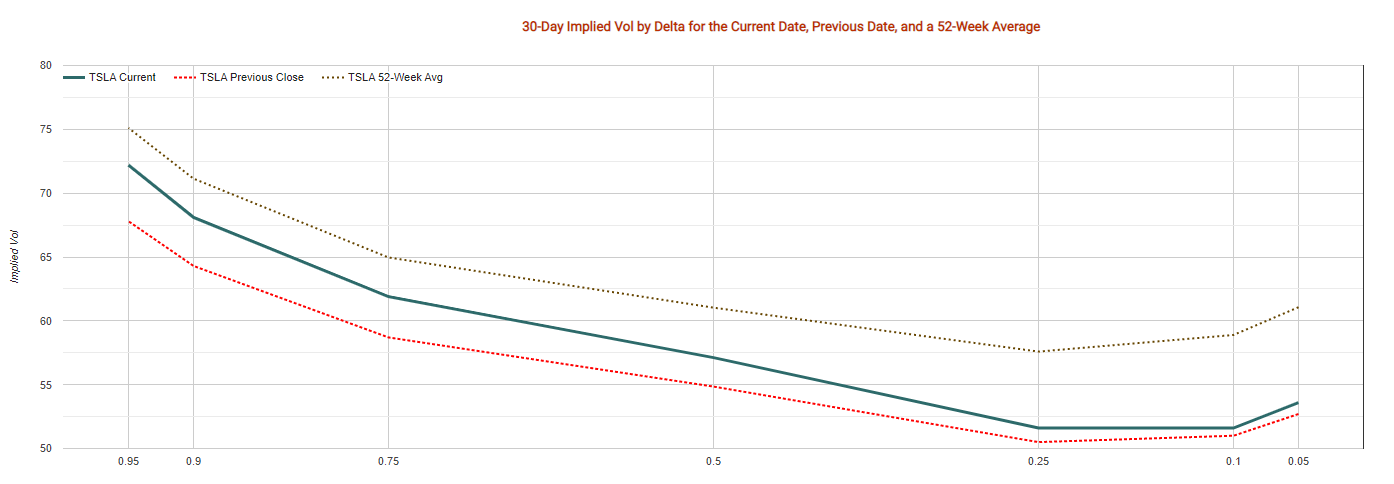

TSLA implied vol is still lower than its 52-week average (I think market vol in general is discounted right now) and put-call spread is barely above its 250-day average. Even if you’re a long-term believer in TSLA and you don’t want to sell, at least consider hedging, as insurance is still relatively cheap.

Market Chameleon Market Chameleon Google Finance

TSLA bulls will not like this chart, but a somewhat messy head and shoulders pattern has appeared in 2022 with strong support around $200 and resistance around $350 (although this was temporarily penetrated). This would imply downside in a bear case near pre-COVID highs of $60 which is congruent with my broader market outlook. If you draw the head at the ~$300 resistance level, you would see downside to roughly $150 which is near YE 2020 levels. I won’t take a specific bet on which I think is the floor for TSLA in this bear market, but I do believe in the next 6 months we will see the S&P and NASDAQ test pre-COVID highs, and while TSLA has enjoyed a substantial advantage over the broad market indices this past year, I would personally look to take gains or hedge downside risk. I’m not sure TSLA will actually trade all the way down to $60 given the fundamental improvements in the business in the past 2 years, I’m more showing this chart to highlight downside risk. For far too long, TSLA investors have been complacent about valuation risk, and I believe the paradigm is shifting as market volatility rises and TSLA will see its premium erode for a time. This will present a great buying opportunity at the bottom of this bear market.

Conclusion

In conclusion, TSLA is a well run business that has enjoyed spectacular equity performance for several years running. The car market is set to cool off substantially in the near future, and I believe we may have already seen peak demand for this cycle. As the industry falls off, Tesla being the relative outperformer over the past three years should suffer more than its competitors on a valuation basis.

Read More: Tesla Stock: Now Is A Good Time To Sell Or Hedge (NASDAQ:TSLA)

{kind=link}