MF3d/E+ via Getty Images

Boy, this market is tough. Really tough. Dividends have helped, but stocks have as a whole been crushed. So what is the right type of stock to own in this environment? We think it is those names that are necessary. Insurance is necessary. But when to buy? We think we are at levels you can start scaling into names you like, even though the market is still falling. We have to remind you that we do not (and will not) support selling everything. We support adding to long-term investments, making short-term trades with momentum, and hedging your portfolio with inverse funds or market puts.

Today, we have a stock that we feel is right for this environment to start buying. It is relatively stable and is a dividend growth investment. The name in question is The Travelers Companies (NYSE:TRV). This is a dividend growth name that is on sale, but should see its business be relatively robust even in a recessionary period because insurance is a requirement in most states and a must-have for many consumers and businesses. Look, the backdrop stinks here, but we have to start buying quality when it is on sale. We will never catch the bottom, so we pick our spots. Much of what is happening to this stock is a result of the macro environment. The VIX is now over 30 here. It has felt as though we have been at a minor degree of panic type action, with this index spiking into the 30s. There has not been a day of complete washout, or full capitulation, but this week we have seen some signs of capitulation starting as major gains from completely wiped out yesterday, and then some. We continue to believe the market bottom is going to be made in late October and that we will see a rally into year-end after the elections. However, earnings will be key, as well as any revisions. With Federal Reserve’s efforts to reduce rampant inflation, equities have largely priced in a recession, though we believe well capitalized insurers are a place to be. Let us discuss.

Dividend growth matters, but watch performance

Just because any stock offers dividend growth and relatively stable returns over time doesn’t mean we just stop paying attention. Always watch performance. When recent earnings were put out, we felt the insurer continues to be a strong company and subsequent investment. While the market is selling off everything, keep in mind the great dividend growth.

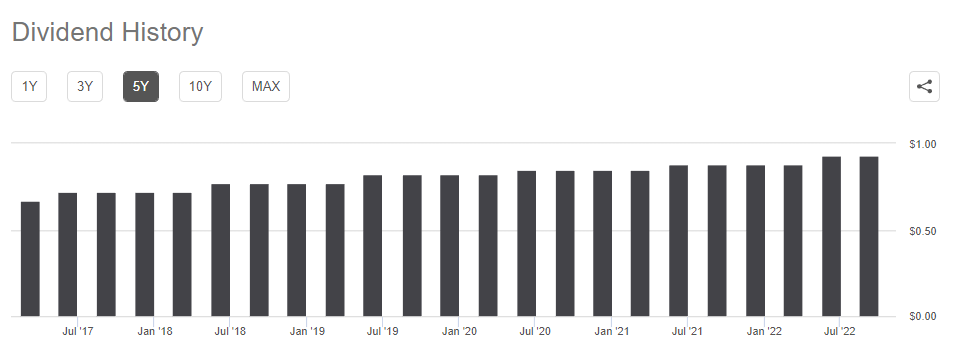

Seeking Alpha TRV Dividend History

So this growth is solid as you get paid to wait. Further, it offers a chance to compound your investment long-term. In the present column, we will discuss performance metrics that you need to be aware of. The stock has been slammed lately, but it was a good quarter. We do not see inflation as extremely detrimental to the business. Perhaps some delinquent payments of premiums increase some, but it’s all about claims volume really relative to net written premiums. We feel it is prudent to highlight some of the critical metrics that you should be keeping an eye on.

The quarter saw a strong top line and bottom line. The insurer continues to be incredibly profitable, and frankly, the market has priced the stock for the future to show much worse results, in our opinion. Catastrophe losses come and go, and those are what matter. In the present quarter, gains were higher than expected. It is the nature of being an insurer. For every quarter with these kinds of gains, there will be others with way more claims than expected. Remember that.

In terms of what we need to look for, like to watch for net income, core income, the customer base (net written premiums), and the underlying combined ratios. The name continues to be one we recommend for the long term, even if the short term is volatile.

Net and core income metrics

Travelers reported net income of $551 million or $2.27 per share in Q2. This is down heavily from last year’s $934 million, or $3.66 per share. This may seem poor by comparison, but last year saw a very unusual year with low catastrophe claims. This was a more normalized quarter. When we look at the last few years, the income pattern shows that there is variability in earnings, and this is just the nature of claims. They vary. The company has just been hit by claims, hard, at times, and other times has light claim quarters. This one was about average. So, core income fell to $625 million, or $2.57 per share. Of course, due to the more normal nature of this quarter, but also was better than expected.

Assuming catastrophe losses that were on pace with historical norms, and factoring in some pain in March weather wise, we were looking for core earnings of $2.25-2.55, which factored in a 5-6% growth in net written premiums as well, but assumed even higher losses on claims. While the results were certainly well above our expectations, it points directly at the volatility and unpredictable nature of insurance. Tough to gauge, but the company continues to do well.

Keep an eye on these metrics too

It was a good quarter in many respects, not just on the income figures. While the combined ratio fluctuates, it did tick up from last year to 98.3% from 95.3%. But for the first half of 2022, it is down from H1 2021 coming in at 94.8%.

The underlying combined ratio remains strong at 92.8%, but this was up from 91.4% last year. Even with the increase, this is still among industry leaders on this important metric. The commercial business is doing well, and the personal auto insurance lines seems to improve meaningfully every quarter. In both, the commercial and personal insurance sides of the business, net written premiums grew once again.

Net written premiums in the quarter were up nearly 11%, and set a new record at $9 billion. This was due to a strong renewal rate change in all three segments, and all three segments showing double-digit percentage gains in premiums. In Business Insurance, Travelers saw a strong renewal rate change of 4.9%, and premiums were up 10%. Renewal premiums were up 10.3%. This was solid. Over in Bond & Specialty Insurance, net written premiums increased by 13%, with amazing performance in both the Surety and Management Liability Businesses. In Personal Insurance, net written premiums increased by 12%, driven by strong retention and new business in both Auto and Homeowners business lines.

This set of results is superb and the company once again delivered yet another year of increases in net written premiums, something that continues a long line of increases. They are doing well. We want to own the right stocks here and finding one that the underlying company, over time, is showing earnings patterns that grow (within the normal quarter-to-quarter variation of operating an insurance business), is not easy. Looking forward, we urge you to continue to watch net premium growth, while monitoring the underlying and combined ratios each quarter. Management has executed well here. And, it is shareholder friendly.

Travelers is shareholder-friendly

The company usually repurchases shares. In Q2, Travelers repurchased 2.9 million shares at an average price of $172.57 per share for a total of $500 million. Reducing the float also boosts EPS. At the end of the quarter, Travelers had $3.005 billion of capacity remaining under its share repurchase authorization approved by the Board of Directors. The ratio of debt-to-capital was 24%, and if we control for net unrealized investment gains included in shareholders’ equity, the ratio was just 21.5%. This is nicely within the company’s target range of 15% to 25% for this metric. And as we mentioned above, this company is a dividend growth machine. We expect the dividend to continue to be raised each year, and the stock now offers a 2.5% yield following the pullback.

Forward view

This is a great stock to start buying now that it has been revalued almost 20% lower. We like it under $150 per share. The balance sheet is healthy and the debt-to-capital ratio is solid. Looking at premium volume for the remainder of the year, we would only expect to see more significant impacts on written premium and earned premium if there is a larger economic contraction from an absolutely severe recession, or excessive claims from natural events. While Hurricane Ian is going to lead to a lot of claims, as there has been a lot of damage, but Travelers appears well insulated compared to many of its competitors which are more heavily exposed to the market in the southeast. In the above link analysts looked and listed the top insurers with exposure, and Travelers is not there, thus, some degree of a buffer relative to other insurers.

Putting it altogether, and assuming continued net premium growth and roughly average catastrophe gains, on the top line, we are anticipating net written premium revenues of $34.5-$36.0 billion. This would be a double-digit increase from last year. We expect more premiums volume-wise, and still see premium charges remaining elevated in this inflationary environment. It is possible if we see disinflation that premium prices could lower next year, but that remains to be seen. We think that a higher combined ratio is likely, earnings will be much more normalized for the year. We think the company sees $13.00-$14.00 in EPS for this fiscal year. That puts the stock at about 11.5X FWD EPS, which is attractive.

With the dividend growth and lower beta of this name following this pullback, we think you want to own a stock like this in the chaos.

Read More: Travelers Companies: A Stock To Own In This Chaos (NYSE:TRV)

{kind=link}