This post was originally published on TKer.co.

Stocks climbed last week, with the S&P 500 jumping 4%. The index is now up 9% from its October 12 closing low of 3,577.03 and down 19% from its January 3 closing high of 4,796.56.

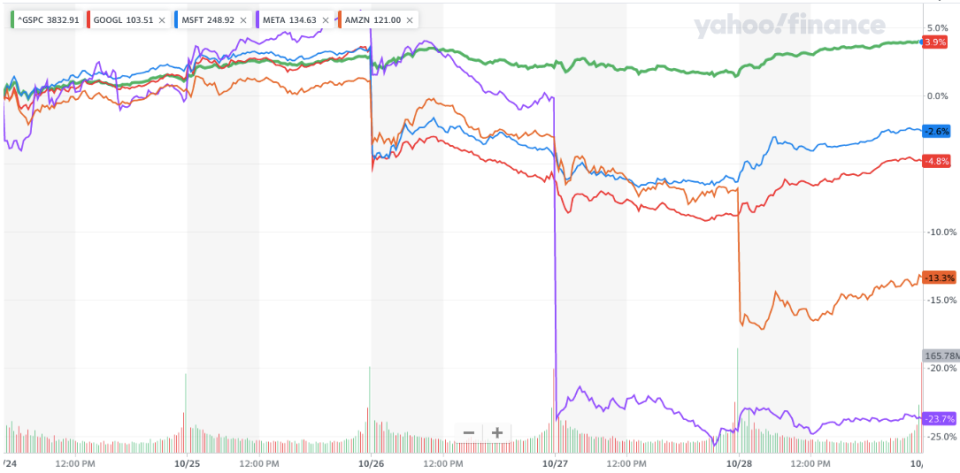

The broad market rally, however, belies some big selloffs among some of the biggest stocks on the planet.

Last week, Microsoft MSFT 4.97%↑, Alphabet GOOGL 4.89%↑, Amazon AMZN 8.66%↑, and Meta Platforms META 0.33%↑ shares fell 3%, 5%, 13%, and 24%, respectively, as the companies gave disappointing quarterly results. All four of these names have been underperforming the S&P basically all year.

This means investors with concentrated exposures to these companies have been experiencing a much more painful 2022 than those in low-cost, passively managed S&P 500 index funds.

All of this speaks to the merits of diversification. By investing in a variety of assets that aren’t closely correlated, you limit the ability of a handful of stocks to ruin your finances.

Of course, diversification comes with some opportunity costs. Specifically, it prevents investors from fully cashing in on the massive gains that are sometimes generated by a handful of stocks.

Unfortunately, it’s extraordinarily difficult to identify which stocks will become the big winners and losers. On top of that, it’s extraordinarily difficult to know when those winners and losers will generate their gains and losses. In fact, the vast majority of professional stock pickers aren’t able to do any of this successfully on a consistent basis. And as a result, most pros underperform the market.

It can be frustrating to see folks with concentrated positions rake it in on some big winners. But it’s during weeks like this that diversified investors should remember to be grateful that they aren’t getting totally smoked.

Reviewing the macro crosscurrents ?

There were a few notable data points from last week to consider:

? The economy is slowing. Gross domestic product (GDP) grew at a 2.6% rate during the third quarter, according to BEA data released Thursday. This follows negative GDP prints in Q1 and Q2. However, the headline GDP number always includes a lot of noise that doesn’t give a good picture of the economy.

To get a better sense of the underlying health of the U.S. economy, many economists will point to “final sales to domestic purchasers,“ which strips out net exports and changes in inventories. This measure increased at a more modest 0.5% annualized rate in Q3.

If you strip government spending from that measure, “final sales to private domestic purchasers” was barely positive, climbing at a 0.1% rate in Q3, down from 0.5% in Q2.

“This series usually means next quarter GDP growth will be soft,“ Neil Dutta, head of economics at Renaissance Macro Research, said on Thursday.

? Early Q4 data doesn’t look good for the economy. The S&P Global Flash US PMI Composite Output Index signaled contraction in economic activity in October. From the report: “The US economic downturn gathered significant momentum in October, while confidence in the outlook also deteriorated sharply. The decline was led by a downward lurch in services activity, fueled by the rising cost of living and tightening financial conditions. While output in manufacturing remains more resilient for now, October saw a steep drop in demand for goods, meaning current output is only being maintained by firms eating into backlogs of previously placed orders. Clearly this is unsustainable absent of a revival in demand, and it’s no surprise to see firms cutting back sharply on their input buying to prepare for lower output in coming months.“

? Several U.S. states are already in contraction. From the Philly Fed’s September State Coincident Indexes report: “Over the past three months, the indexes increased in 44 states, decreased in four states, and remained stable in two. … Additionally, in the past month, the indexes increased in 38 states, decreased in 10 states, and remained stable in two…”

? Consumer confidence deteriorates. From The Conference Board’s Lynn Franco: “Consumers’ expectations regarding the short-term outlook remained dismal. The Expectations Index is still lingering below a reading of 80 — a level associated with recession — suggesting recession risks appear to be rising. Notably, concerns about inflation — which had been receding since July — picked up again, with both gas and food prices serving as main drivers. Vacation intentions cooled; however, intentions to purchase homes, automobiles, and big-ticket appliances all rose. Looking ahead, inflationary pressures will continue to pose strong headwinds to consumer confidence and spending, which could result in a challenging holiday season for retailers. And, given inventories are already in place, if demand falls short, it may result in steep discounting which would reduce retailers’ profit margins.“

? The housing market is taking a toll on the economy. According to the Q3 GDP report, residential investment fell at an annualized rate of 26.4% during the period. That shaved about 1.4 percentage points off of GDP growth.

? New home sales fall. According to the Census Bureau, the pace of new home sales in September fell to an annualized rate of 603,000 units, down 10.9% from the month prior.

? Home prices cool. According to the S&P CoreLogic Case-Shiller index, home prices fell 0.9%…

Read More: The merits of diversification were on full display last week

{kind=link}