CreativeNature_nl

Today, I am offering Aemetis (NASDAQ:AMTX) as my Growth Stock Of The Year in 2023. Aemetis is a biofuels company focused on low, no and negative carbon intensity biofuels from dairy and orchard agricultural waste products in California, carbon capture and biodiesel in India.

The biofuels industry is growing rapidly thanks to a need for low carbon intensity fuels. Biofuels firms have already seen a first wave of buyouts by larger fossil fuels companies trying to gain traction in a government subsidized industry.

Aemetis has contracts in place to generate over $1.5 billion in revenue for full year 2026 and generate around $500 million in profits against a current share count approaching 35 million. The current market cap of the company is down 70% from highs and rests at only about $140 million.

A simple analysis of the math (done below) suggests that Aemetis shares could be a potential 10-bagger or better at rational valuations. If there is a FOMO rally and/or takeover, share appreciation over the next several years could be even higher. Even more importantly than potential gains, is that the company comes with a significant margin of safety.

I rate Aemetis a strong buy for appropriate investors.

Get To Know Aemetis

I’m not a fan of regurgitation, or cheerleading, rather, I will share my thoughts on what the market is missing with Aemetis. That approach has offered the most value over my nearly 3 decades of investing.

I am also a believer in what Warren Buffett and Jimmy Rogers have said about investing: do the reading. So, with that in mind, please start your due diligence with the presentations at the Aemetis investor relations webpage:

Download Aemetis Company Presentation

Download Aemetis Investor Presentation

Download Aemetis Carbon Capture Presentation

And, this recent report from Stonegate Capital Partners:

Stonegate Capital Partners Aemetis Research Report

A year ago I interviewed the CEO of Aemetis, Eric McAfee. I encourage you to give it a listen. I found the story compelling then. With a year of significant business achievements and a lower stock price, I find Aemetis a more compelling story now than a year ago.

Here is an image from the Aemetis website that summarizes their business of refining low carbon to carbon negative biofuels from feedstock that would otherwise be pollution generating waste. They describe this as a “circular bioeconomy” model.

Aemetis Virtuous Low Carbon Biofuels Cycle (Aemetis)

What you can see is that Aemetis is not like other biofuel companies that you have watched for years. Aemetis is not reliant on growing feedstock that could otherwise be food.

Rather, Aemetis is taking agricultural waste that would otherwise put methane and CO2 into the air and refining it to replace fossil fuels. In addition, when their carbon capture site is ready, they will in many use cases be carbon negative.

Aemetis Fundamentals

Aemetis operates in four businesses:

Aemetis 4 Lines Of Business (Aemetis)

Further, the company is broken up into domestic business in California and international business in India.

The company has gone through a long transformation since its inception in 2006. It has had to navigate multiple market conditions, shocks and energy transition developments to build the current company.

Third Eye Capital is the company’s senior lender and a significant equity holder. A year ago Aemetis and Third Eye Capital negotiated a $100 million credit facility (of which about $40 million is still available) at prime plus 6%, which is very reasonable for a company at this phase of its capex phase.

Third Eye’s warrants include entitlement to buy 50k shares at $10.20 and 250k shares at $20. Those warrant tranches are from the March 2022 credit agreement which recapitalized much of Aemetis debt and access to $100 in revolving credit facilities.

In the past two years, Aemetis has moved rapidly on its business model.

- Purchase and approval for the new Riverbank facility which will produce jet fuel and renewable diesel, as well as, be the site for carbon capture and sequestration – this facility is where much of the company’s debt is tied to.

- Aemetis now has 7 dairy digesters for producing renewable natural gas running, with 10 more under development and over 45 more projected by 2026 (I expect that number to dramatically increase as there are over 1000 target dairy farms in California).

The company growth rate for 2023 is projected to be over 28% and was a shade over 37% the trailing 12 months which is mostly due to the law of small numbers. 3rd quarter 2022 growth over 3rd quarter 2021 was 44%.

Aemetis is not yet profitable owing largely to paying down $80 million debt the past year. As you will see in coming sections, it is likely that the company will continue paying down debt in 2023 and, in fact, could be a debt free company with significant free cash flow in the next few years.

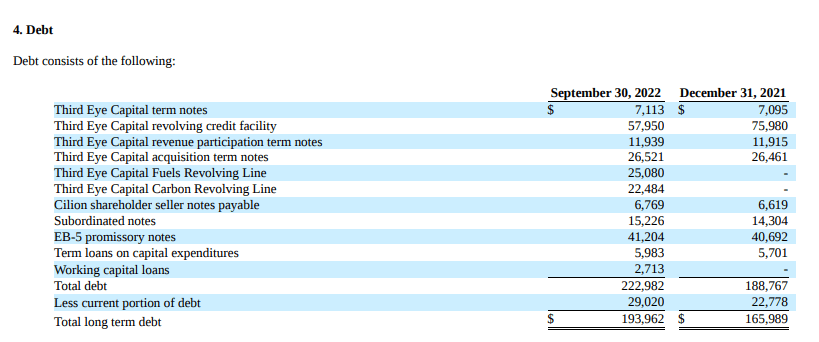

Debt Threat

Under a traditional SWOT analysis, we would find the most pressing threat to the company. In the case of Aemetis, it is debt. Here is what their debt load looks like:

Aemetis Debt Load (Aemetis)

The two large subsets of debt are that to Third Eye and their term loans which are largely subsidized by U.S. government programs, i.e. low rates, easy financing.

It is unlikely the government will reverse course on the loans tied to government programs designed to incentivize biofuel and carbon capture businesses. Indeed, if that were to happen, it would hurt everyone from the “small guys” to the “big guys” like Chevron (CVX), Exxon (XOM) and Occidental Petroleum (OXY) which is 20% owned by Berkshire Hathaway (BRK.B). I am willing to risk that political earthquake not happening.

The Third Eye notes rely on Third Eye continuing to work favorably with Aemetis to repay debt as they have the past decade. It is important to note that Third Eye really gets “paid” when the share price rises.

From the Stonegate report:

Debt level and interest expense could limit cash flows – The Company currently owes approximately $55M to Third Eye Capital with a maturity in April 2023. Notably, Aemetis has repaid $80M worth of debt since the beginning of 2021. The current interest rate will continue to hamper cash flow, cash position, and stock price. Aemetis may not be able to repay the principal at that time. If the Company is unable to refinance, it will have to sell assets to pay off the balance of the loan.

That paragraph contains two important ideas.

- Their is a rapidly impending large debt maturity.

- Aemetis has been rapidly paying down debt.

These items are central to the catalyst equation for the share price appreciating in 2023 and beyond.

The April 1, 2023 debt maturity are also what shorts are pointing to as a danger sign.

I am not afraid of the debt maturity for a number of reasons:

- I believe Third Eye will continue to work favorably with Aemetis.

- I believe that Aemetis has significant assets which could be sold to actually make the company debt free and still maintain a highly profitable business.

I believe the next debt refinancing, likely in Q1 2023, will be a significant catalyst for the stock to rise. But, wait, there’s more.

I believe the market will start to more fully understand the value of Aemetis businesses and assets.

Biofuels Demand

According to the IEA, growth rates for biodiesel in the U.S. are projected to be above 10% through 2030. In Europe and Asia biodiesel growth rates will be higher as both search for energy security and Asia has much of the economic growth in the world.

I point out the growth rate because, clearly, most of the global economy is not growing double digits.

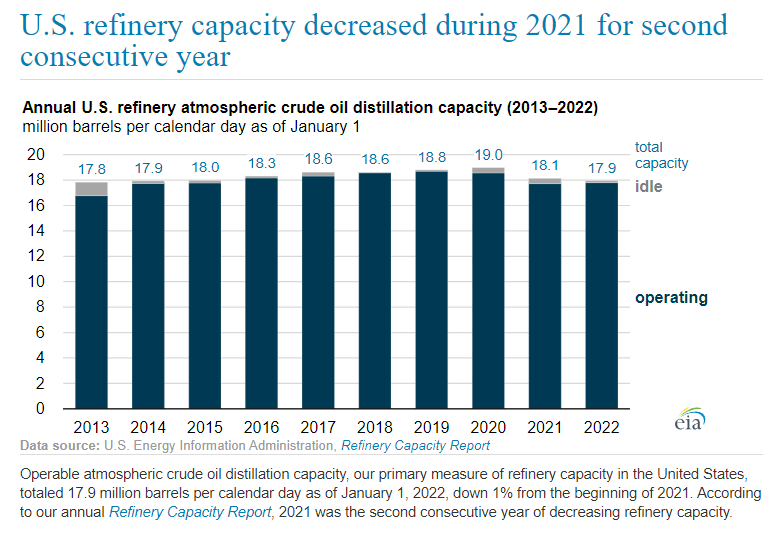

In addition, as noted by the EIA, the U.S. there has developed a refining shortage in the past 3 years.

U.S. Refining Capacity (EIA)

Globally, refining shortages are pervasive in most of the world – though China has extra capacity right now.

In general, new refining is very profitable because it is scarce.

Aemetis represents new refining capacity.

Aemetis Ethanol

When people here biofuel they instinctively think ethanol. And yes, Aemetis has that, but it is not the source of their future growth. Rather, think of it as baseline revenue for the near term.

Their Keyes, CA plant is a 65 million gallon per year facility, but is subject to fluctuating feedstock prices, i.e. corn. The plant also supplies dairies with over 400,000 tons of feed annually and is partner in a business supplying CO2 for the beverage, food and industrial sectors.

The company is currently installing a 1.5MW solar microgrid built by oil major TotalEnergies (TTE) which will increase their tax credits by reducing their own natural gas use by 90% while reducing their energy costs.

Aemetis Biogas

Aemetis is in the process of building out a large biogas network that will capture methane from California dairy farms. To date, Aemetis has 7 digesters running, 3 under construction and about 30 under contract per the earnings call with a planned 66 planned by 2026.

What’s super interesting is that demand is outstripping their ability to keep up on building. Between parts and labor, there is a backlog. More interesting is that there are over 1000 dairies that could provide more demand.

Here’s who wants the RNG…

Aemetis has a contract with Trillium Energy, which is a member of the Love’s group, to sell RNG. Love’s operates over 600 Love’s Travel Stops & Country Stores in 42 states.

Aemetis Signs Six-Year Agreement With Trillium to Supply Dairy Renewable Natural Gas

What is important to note, is that Aemetis has essentially sold out their planned capacity during the construction phase.

This demand is not isolated…

If you read the opening of CEO Eric McAfee’s remarks in his Q3 2023 earnings call you will start to understand the value of Aemetis business.

Aemetis bought out a preferred equity in Q3 and took the non-cash charge to facilitate a future transaction. What does that mean?

It means the company is considering monetizing the biogas unit…

Read More: Aemetis Is My Top Growth Stock Of 2023 (NASDAQ:AMTX)

{kind=link}