marrio31

I Expect A Slow Burn with S&P 500 Earnings Dropping to $210 in 2023

Company management and analysts have not been forthcoming enough in reducing S&P 500 (SP500) earnings estimates, and are still fostering hopes of earnings not declining significantly in 2023. It is indeed delusional as Morgan Stanley’s Lisa Shalett puts it, that CEOs and subsequently, analysts haven’t lowered 2023 and 2024 earnings estimates commensurately – even as many confidently predict a recession. I expect inflation, which caused a single digit revenue increase for S&P 500 companies to reduce gradually in 2023. The 6-8% increase in CPI and CPE throughout 2022, which depleted customers wallets, also contributed strongly to the S&P 500 top line. We paid higher at the pump and at the grocery store because companies passed along these costs to us, their customers. This is highly unlikely to happen in 2023, especially on a higher base. In fact, excess inventory and lower demand should lead to lower prices across the board.

I see the slow reaction from investors and traders to lower earnings guidance as the biggest threat to the market in the first quarter of 2023. For now, however, it feels like a slow burn till Q4-22 earnings season starts in earnest in the third week of Jan 2023, when Q1-2023 and full year 2023 guidance finally tips over and the disappointment hits the markets like a freight train.

It is not that analysts have been sleeping, they did mark earnings down 5.6% for Q4 2022 in October and November.

According to FactSet the Q4 bottom-up EPS estimate (which is an aggregation of the median EPS estimates for Q4 for all the companies in the index) decreased by 5.6% (to $54.58 from $57.79) from September 30 to November 30. Thus, the decline in the bottom-up EPS estimate recorded during the first two months of the fourth quarter was larger than the 5-year average, the 10-year average, the 15-year average, and the 20-year average. The fourth quarter also marked the largest decrease in the bottom-up EPS estimate during the first two months of a quarter since Q2 2020 (-35.9%).

The bottom-up EPS estimate for CY 2023 declined by 3.6% (to $232.52 from $241.22) from September 30 to November 30.”

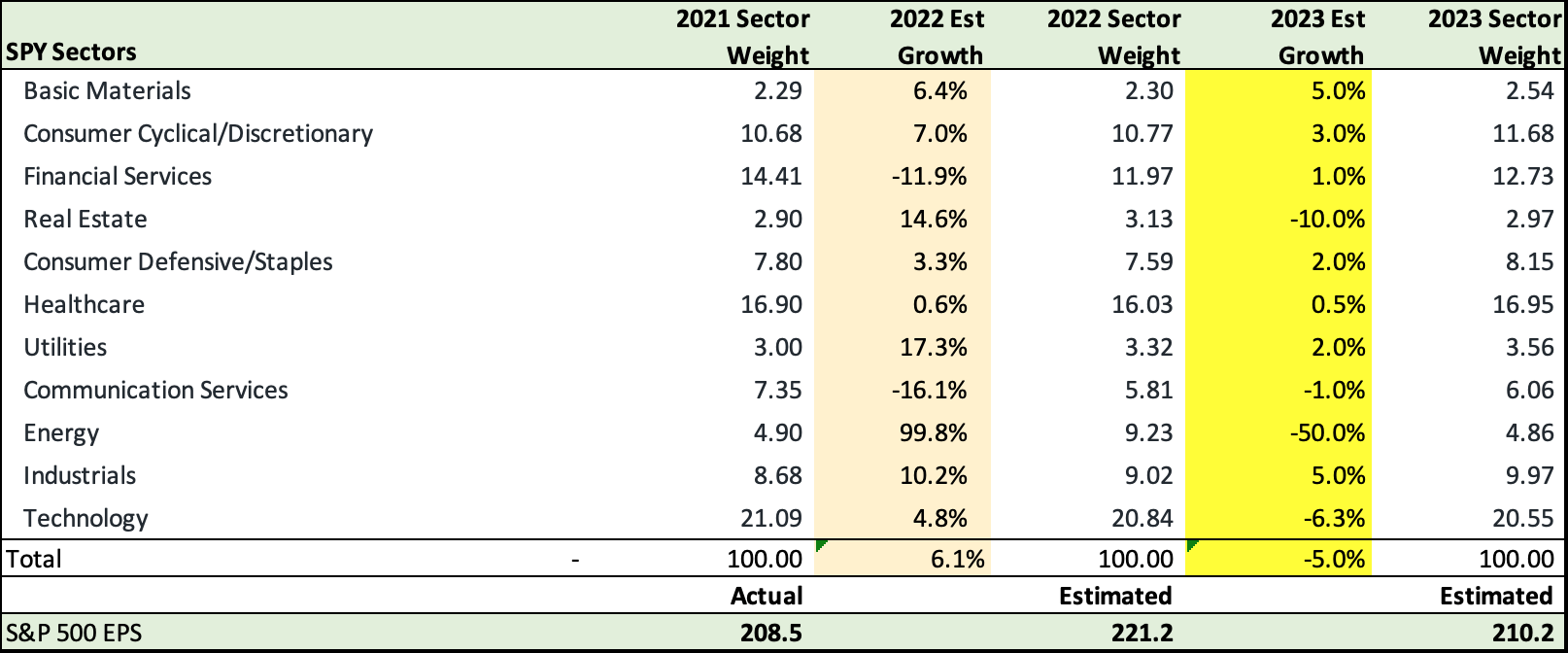

As of now, in my opinion, consensus bottoms up revenue estimates of $232.52 are still way too high and don’t reflect weaknesses in the energy, real estate, technology and communication sectors:

Here are my S&P 500 sector specific growth rates estimates that point to a 5% lower YoY 2023 earnings of $210 compared to 2022.

S&P 500 earnings By Sector (FactSet, Bloomberg, The Heisenberg Report, Fountainhead)

In my opinion, these are the sectors that should weigh strongest on the S&P 500 in 2023.

- High oil prices, which led to a massive 100% increase in Energy earnings will see a 50% reversal to earnings in 2023 and bring its sector weighting back to the more normal 5%.

- Real Estate, which saw gains of 15% in 2022 should fall with the housing bust and drop 10% in 2023.

- Consumer cyclicals should also lose much of its inflationary gains of 2022 with tepid growth of 3% in 2023.

- Technology, the highest weighting, which still eked out an estimated gain of 4.8% is likely to lose about 6.3% in 2023.

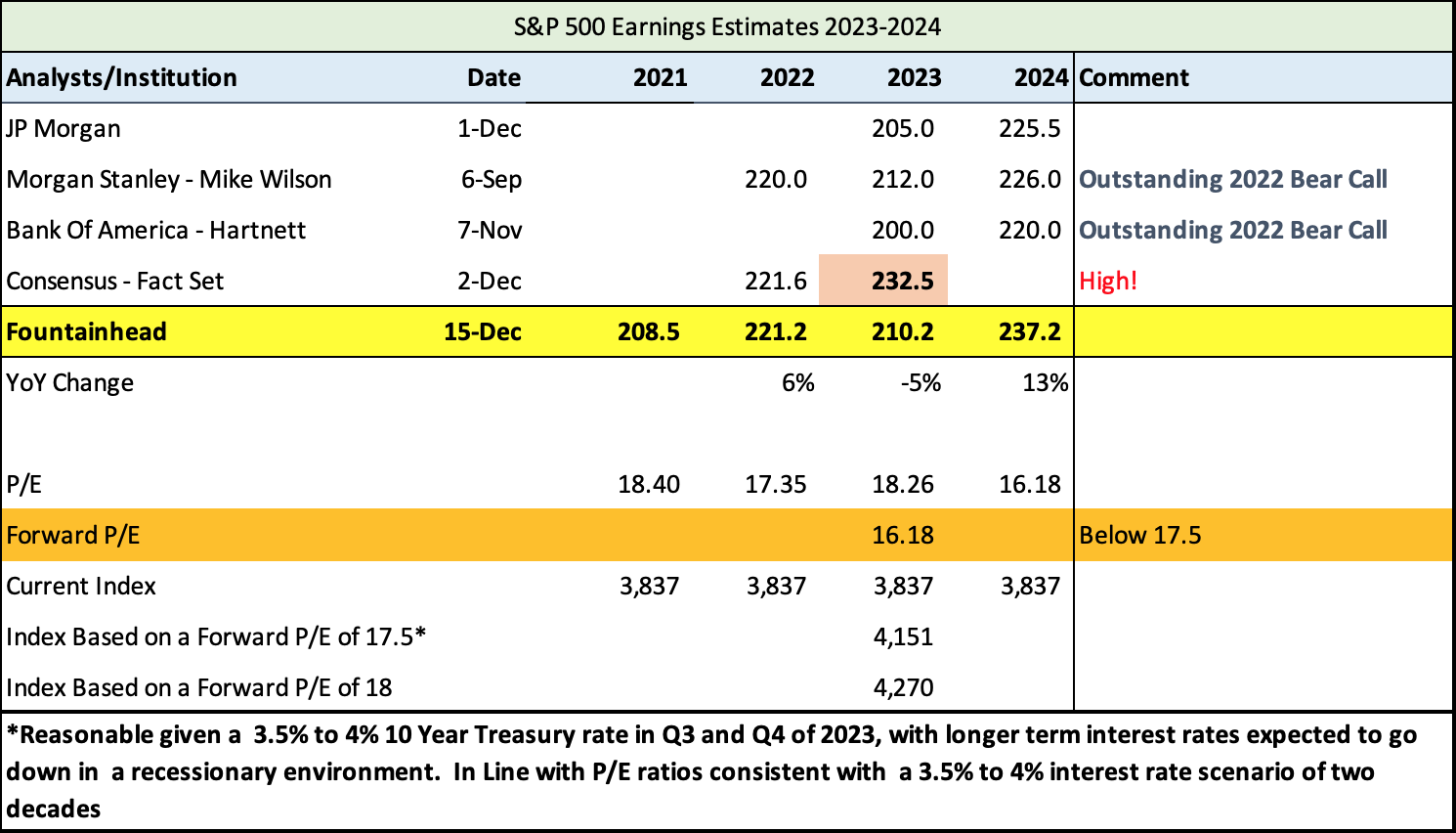

I Expect Growth to Resume in 2024

S&P 500 Earnings Estimate 2023 (FactSet, The Heisenberg Report, Bloomberg, Seeking Alpha, Fountainhead)

I stacked up my estimates against consensus and Morgan Stanley and Bank of America, whose analysts had outstanding bear calls for 2022. I’m not as bearish as Bank of America, which has an EPS estimate of just 200, but also looks for a return to growth of 10% in 2024. My own growth estimates for 2024 are higher at 13% for three reasons –

a) Technology and Communications, the two biggest sectors, will return to higher growth.

b) I don’t anticipate the labor market to falter beyond an unemployment rate of 5.5 %

c) In my view, there will be “normal” inflation of 3% going forward, hence I do expect it to show in the nominal earnings numbers.

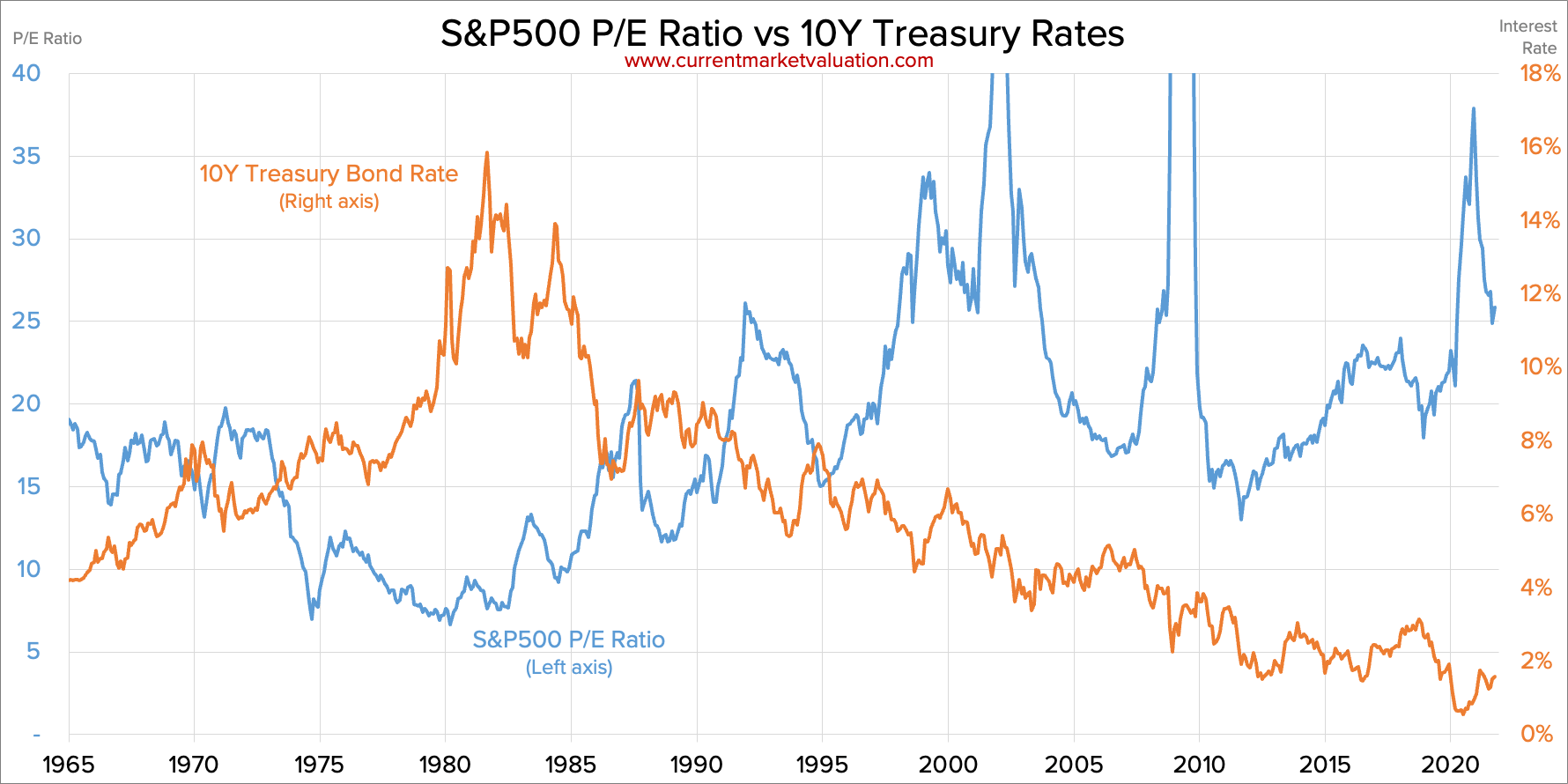

S&P 500 PE V Interest Rates (Current Market Valuation)

A Conservative Multiple and Growth Rate

Based on the historical chart above, in 1995, the 10-year treasury was above 6% and then fell to a low of 2% during the Great Financial Crisis, ranging between 3.5% to 4.5% for the most part in those 15 years. During this period, the S&P 500 P/E ranged between 15 and 25 for the most part except for those two years when earnings plummeted during the GFC. The “supposedly high” 10-year interest rate of 3.5%, which has given investors so much consternation was “normal” for 15 years and we still had P/E’s of 15+ during that time. Therefore, I believe that a P/E of 17.5 around the end of 2023 with a trending decline in interest rates in 2024 is not a big ask at all – if anything I may be conservative.

Going forward, I’m not looking at P/E’s beyond 18, which would make us guilty of a recency bias. In the greatest bond market in history, before inflation reared its ugly head, after the GFC, 10-year treasuries ranged between 2% and 4% and of course between 0.5% and 2% during COVID, which led to the S&P at 4,800 having a trailing P/E of 23 on a 2021 EPS of $209! If it looks like an asset bubble, if it walks like an asset bubble… That should be a clear warning!

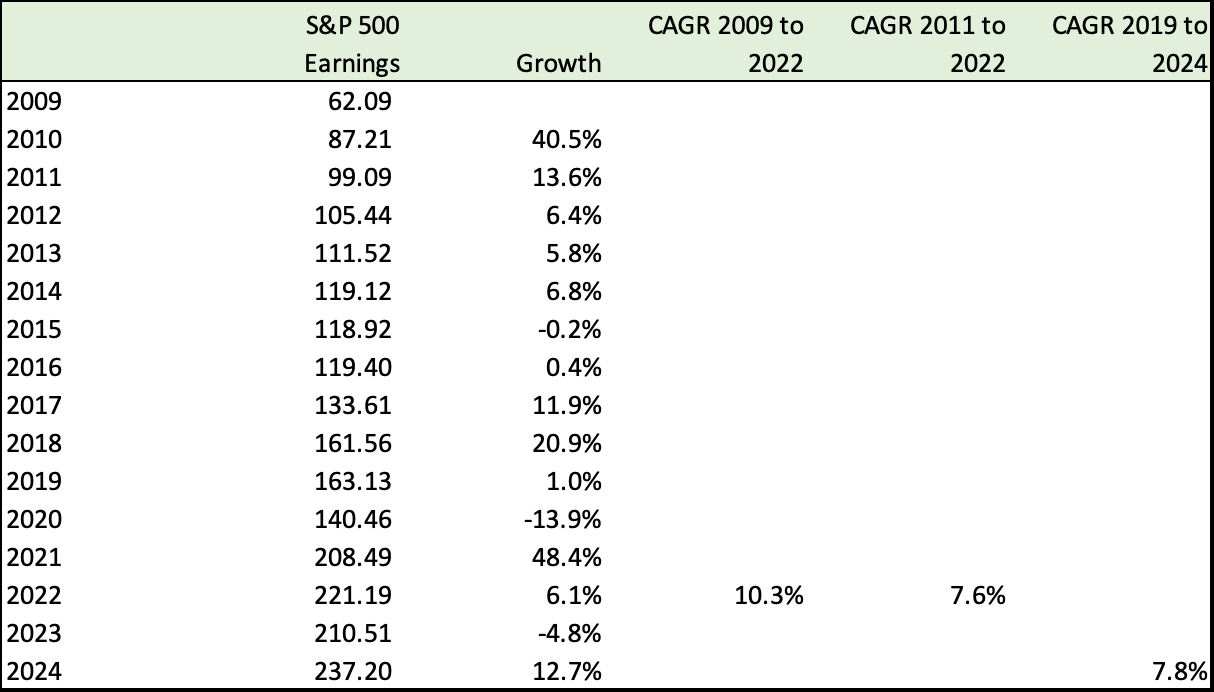

Also from an earnings standpoint, if you smoothen out COVID fluctuations, the 5 year 2019-2024 earnings CAGR is only 7.8%, which is consistent with the 2011-2022 growth of 7.6%. I’m not taking the higher 2009-2022 rate because post GFC the base of 62.09 was extremely low and it distorts the historical trend.

S&P 500 Earnings (Fountainhead, Yahoo Finance, Yardeni)

I believe The Fed Pivot is not Pivotal

I actually believe that the Fed pivot is not pivotal, and instead of navel-gazing as to when Powell will blink in the face of recession, we should be looking at a new, “new normal” of 10 year treasuries ranging between 3.75% to 4.5% in the first half of 2023 and flattening to 3.5% to 4% in Q3 and Q4 2023 with a likely decrease in 2024. As we saw from the chart above, we have survived and thrived in 3.5 to 4% interest rates – if you’re not looking for outlandish “Stimmy” valuations! Instead I would rather focus on finding a) Great investments and b) Scouting for bargains which will be available in spades in 2023 and c) Putting strict limits to take profits when either we’ve reached our price target or the market has given it an absurd valuation.

I expect the Fed’s 2% Target Inflation Rate To be Ditched – Live With the New Normal

I believe the Fed will explicitly or implicitly ditch its 2% target inflation rate. With the PCE (the Fed’s preferred inflation gauge) running at 6% Year on Year, it doesn’t make sense to target 2% knowing that you’d have to set a nominal interest rate of 8% to reach that target. The PCE actually peaked at a 7% YoY increase in June 2022 and while confident of a decline, I don’t believe it will go below 3-4% for the most part of 2023. Wage and shelter inflation are far stickier than commodity and supply chain inflation.

We tend to forget that the Fed hikes have a limited impact – their biggest impact and effectiveness is in pricking asset bubbles, ironically the same ones that they helped create! And to a large extent, in 2022 the markets have been punished for irrational exuberance, for buying the dip and paying excessive multiples without realizing that interest rates cannot stay at zero forever.

To that extent and if that is their mandate – they have been successful in spades. Every asset class has dropped in 2022.

Forget about the pivots and when the Feds will stop increasing rates; I think the focus should be to accept that inflation is not likely to reduce in a hurry – I don’t believe the Feds can actually reduce wage growth way the way they can puncture asset bubbles.

The Feds also have a hard time fighting inflation caused by supply chain disruptions and geopolitical tensions. For example, the Fed can do little to influence oil prices, which are again dictated by the monopolistic OPEC. Sure, higher interest rates make capital investment more expensive, thereby preventing over capacity, but simply not making capital available also has the opposite effect – you are reducing capital expenditure, which means existing manufacturers or material producers and miners can charge more without worrying about new capacity coming up soon again. I don’t believe higher interest rates are going to reduce material and commodity prices in a big way. It’s counterproductive.

To the Fed’s credit – it is crucial to understand that the Fed is seen to be fighting inflation. Entrenched inflation expectations are worse because they predicate human behavior, which means instead of spending, we hoard since we expect prices to go up even further, which then creates a vicious inflationary spiral. Or we postpone, which reduces demand in the economy, not because prices have gone up recently, but we want to buy when things are cheaper. Besides, the Fed has to be that one institution, which should be seen as winning the fight on inflation – even if they attack in a “whack a mole” fashion. I believe the outcomes will be selective and the biggest influence will be on asset prices, and with more than a 30% drop in the NASDAQ Composite Index (COMP.IND) and 20% in the S&P 500 the Fed has already achieved that.

The Fed has also done a reasonable job in reducing the housing bubble. With mortgage rates ratcheting to over 7 percent, it has shaken out a fair amount of excessive speculation. The Fed’s second goal was to reduce shelter inflation/renters inflation, which usually occurs with a time lag, and I believe this should happen in Q2 of 2023, simply because leases are annual affairs and will show up in the statistics with a lag even if this is already happening. Shelter inflation is the biggest part of our monthly budget and we should see some improvements in 2023, which will continue to reduce inflation.

The last frontier – High wages. As…

Read More: Poor Earnings To Drag S&P 500 In First Half, But Expect Recovery To 4,151 By Year-End

{kind=link}