hernan4429/iStock via Getty Images

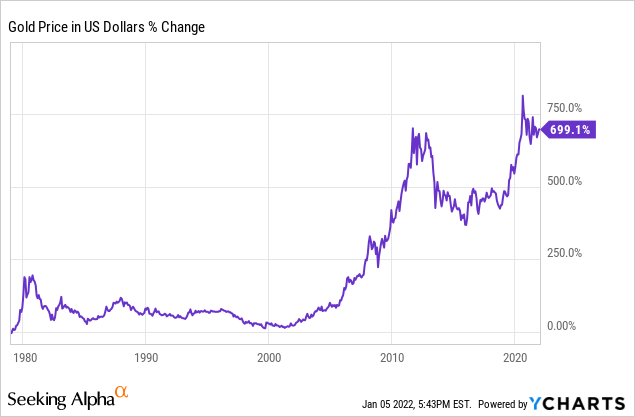

One of the most time-tested inflation hedges is gold (GLD). As you can see from the chart below, during periods of high inflation (like the runaway inflation of the 1970s, the Federal Reserve-fueled housing boom of the 2000s, and the post-Great Financial Crisis and post COVID-19 crash quantitative easing schemes by the Federal Reserve) gold prices have soared:

Based on the chart below, whenever the real interest rate was negative over the past decade, gold was up significantly every time.

| Year | Real Interest Rate | Gold Performance |

| 2010 | Clearly Positive | Up Significantly |

| 2011 | Clearly Negative | Up Significantly |

| 2012 | Clearly Negative | Up Significantly |

| 2013 | Clearly Positive | Down Sharply |

| 2014 | Slightly Positive | Down Slightly |

| 2015 | Clearly Positive | Down Sharply |

| 2016 | Clearly Positive | Up Slightly |

| 2017 | Roughly Zero | Up Slightly |

| 2018 | Slightly Positive | Flattish |

| 2019 | Slightly Negative | Up Significantly |

| 2020 | Roughly Zero | Up Significantly |

source: Author’s calculations comparing CPI, Long-term U.S. Interest rates, and Gold Price movements

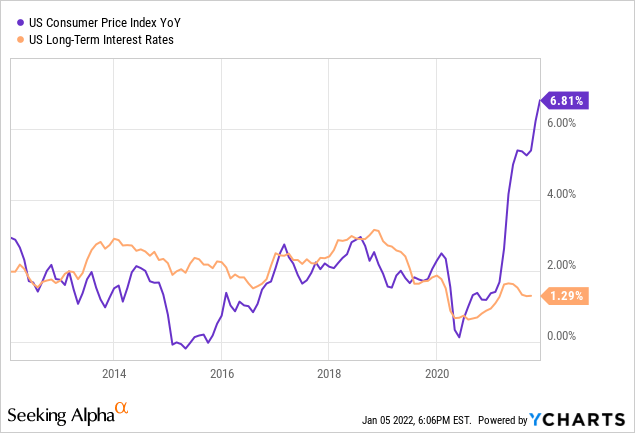

Heading into 2022, the environment is about as favorable as it has ever been as the U.S. Consumer Price Index has soared to multi-decade highs and long-term interest rates remain stuck near historic lows:

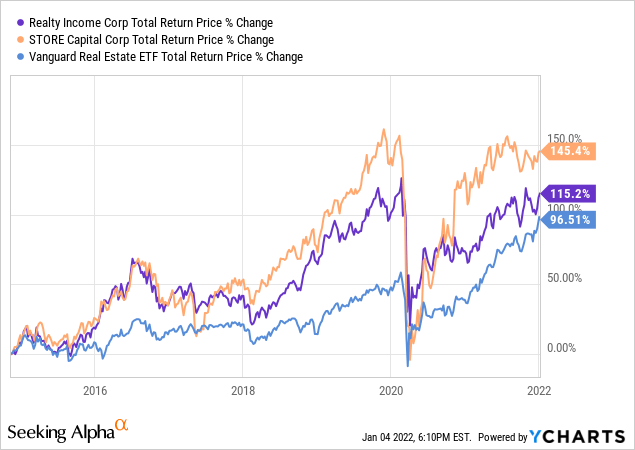

While traditional income growth instruments like triple net lease REITs (NETL) have proven to be one of the top income investments in recent years, with triple net lease REITs like Realty Income (O) and STORE Capital (STOR) beating the broader real estate sector (VNQ) by a healthy margin:

…all of this is about to change with inflation accelerating and interest rates potentially headed higher. Traditional income sectors which have widely been viewed as bond proxies are at significant risk as income investors need their income to keep pace with rising rates of inflation in order to protect their purchasing power.

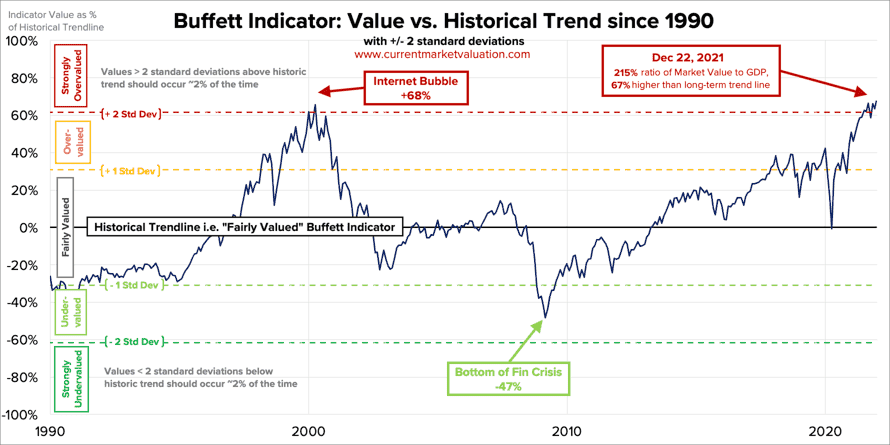

Furthermore, heightened geopolitical and macroeconomic uncertainty alongside elevated stock market valuations make the markets dangerous places to be invested these days. Just take a look at the bloated Buffett Indicator:

As a result, we at High Yield Investor are working tirelessly to identify the rare few remaining investments that combine resistance to geopolitical risk and inflation with value and attractive income yields. In today’s article, we will outline three reasons why we believe that Barrick Gold (GOLD) is one of those increasingly rare opportunities.

#1. Best-In Class Low-Risk Miner

While many investors shy away from gold miners (GDX)(GDXJ) due to their checkered past, we believe that GOLD’s best days are ahead of it.

A big reason for that is simply that GOLD owns arguably the highest quality portfolio of mines with its collection of “tier 1” trophy assets and commitment to operational excellence and improved efficiency.

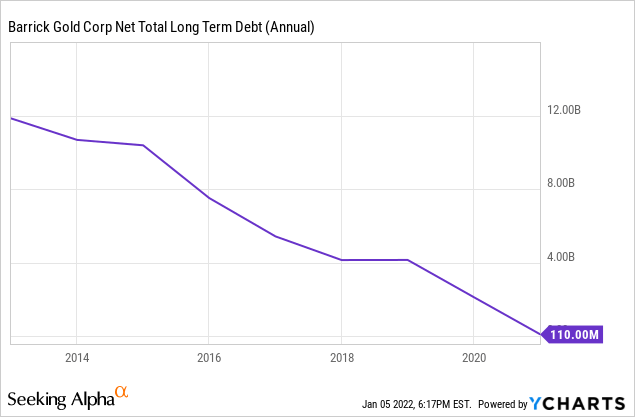

Furthermore, GOLD has further enhanced its risk-reward by attacking its hefty debt pile aggressively over the past decade:

while simultaneously increasing its project profitability standards in order to position it well for weathering any down markets in the gold price.

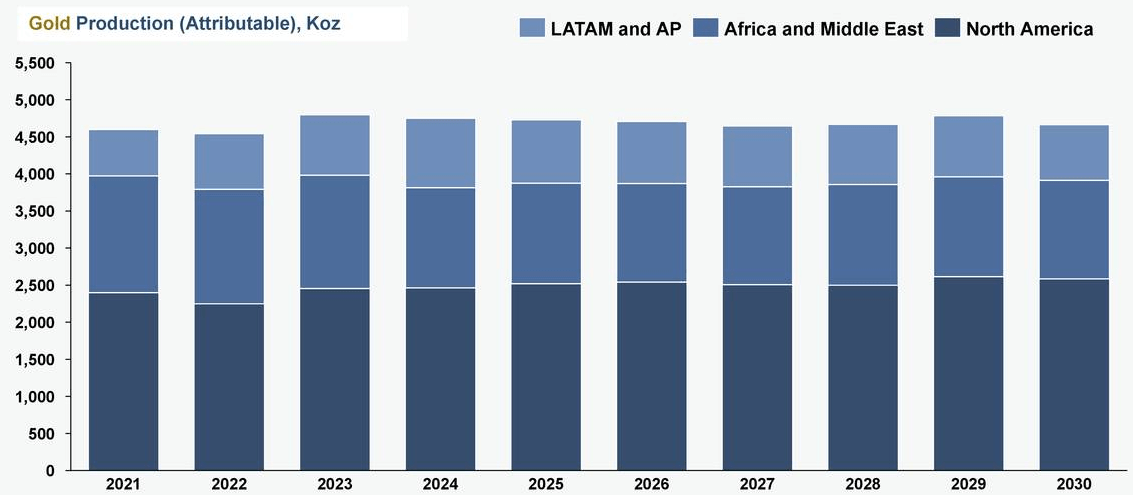

Last, but not least, it has built up a proven and probable reserves portfolio that gives it a 10-year mine life estimate with very stable production over that span:

This massively reduces the risk of the company since it means that even if it experiences poor results from its exploration efforts, it should still have a very stable cash flow profile moving forward. As a result of these strengths, many of the weaknesses and risks that are typically attached to miners do not apply here.

#2. Leveraged To The Price Of Gold

As already mentioned at the beginning of this article, GOLD has leveraged exposure to the price of gold. Whenever gold prices rise, GOLD’s share price should (and almost always does) soar by an even higher amount.

As a result, if you share our bullish thesis for the price of gold in the current environment, GOLD should enjoy a powerful tailwind to its intrinsic value.

#3. Barrick Gold – Compelling Valuation

On top of what should be a strong boost from rising gold prices in the coming years, GOLD’s share price looks very cheap compared to its historical valuation multiple as well as its nearest peer Newmont Corporation (NEM):

| EV/EBITDA | EV/EBITDA (5-yr) | P/E | P/E (5-yr) | |

| GOLD | 5.75x | 6.85x | 15.94x | 22.73x |

| NEM | 7.91x | 7.83x | 21.00x | 23.12x |

As a result, GOLD shares offer leveraged upside to gold prices with a relatively low downside risk thanks to its de-risked business profile, basically net debt free balance sheet, and large margin of safety thanks to its very cheap valuation.

As a cherry on top, GOLD paid out a 4.2% dividend yield on the current share price in 2021 and management has indicated that it will soon be issuing revised dividend guidance for 2022 and beyond. Given the company’s stated aversion to share buybacks, dividend returns should be similar – if not better – than 2021’s if gold prices remain stable or move higher from here. This makes it an excellent inflation-proof dividend stock in the current environment.

Investor Takeaway

We at High Yield Investor are targeting investments that combine resistance to geopolitical risk and inflation with value and attractive income yields. While these are hard to find, we have identified several especially attractive opportunities which we have recently released in our latest Top Picks report. We expect these stocks to continue driving our significant outperformance in 2022 similar to what we have experienced thus far:

| Investment Fund | Total Return |

| HYI Core Portfolio | 41.51% |

| Global X Super Dividend ETF (DIV) | 31.48% |

| S&P 500 ETF (SPY) | 31.51% |

One of our most promising opportunities is found in the gold mining sector as – between extremely negative real interest rates and elevated macroeconomic and geopolitical risk – gold is in what we view as a very bullish environment that we expect to result in meaningfully higher prices within a few years.

As a result, the gold mining sector looks very promising in general, and the dividend paying blue chips like GOLD and NEM look particularly attractive relative to more inflation-sensitive traditional income investments like REITs and utilities (XLU).

GOLD gets the nod from us as the top pick in the space given that it is considerably cheaper than NEM right now and is well-positioned to generate significant long-term outperformance.

Read More: Barrick Gold Stock: One Of Our Top Picks For January (NYSE:GOLD)

{kind=link}