marchmeena29/iStock via Getty Images

Investment Thesis

I wrote two articles recommending growth investors buy the Invesco S&P 500 GARP ETF (NYSEARCA:SPGP) in October and January. I calculated that the amount of growth investors was giving up by introducing SPGP’s value screens was relatively small and that it was prudent to choose the heavily discounted option. The end result was SPGP ranking #1 out of 34 growth ETFs in the last three and six months. SPGP embraced its status as a reasonable compromise for concerned growth investors and has lost 8% less than the iShares S&P 500 Growth ETF (IVW) this year.

Nevertheless, after acknowledging this positive trend and the uncertainty in today’s market, I am downgrading my rating on SPGP today from buy to hold. The reason is that I am surprised at the amount of style drift its Index has experienced in just a few short months, and SPGP is no longer a compelling alternative to low-fee growth ETFs. With this article, I’ll explain why.

SPGP Overview

SPGP tracks the S&P 500 GARP Index, using five factors to select 75 constituents at each semi-annual reconstitution:

- Three-year earnings per share growth

- Three-year sales per share growth

- Financial leverage ratio

- Return on equity ratio

- Earnings to price ratio

In a previous article, I outlined why the Financial Leverage ratio was important since it ensures growth is driven by higher profit margins or the efficient use of assets, per the DuPont Equation. I also expressed some reservations about the use of historical ratios only. To compensate, I chose to examine mainly forward-looking metrics and will be doing the same today.

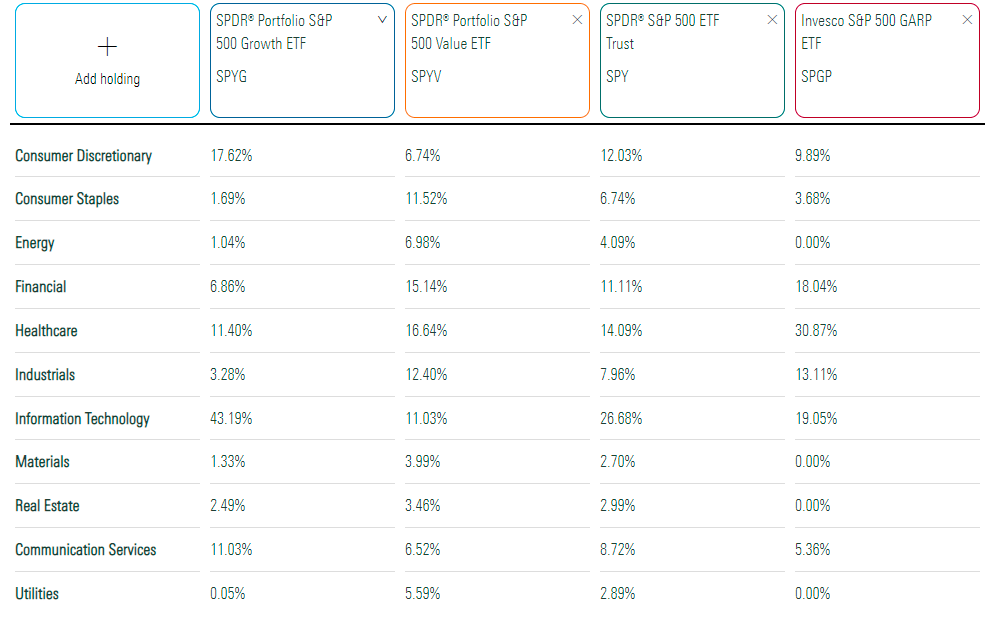

Sector Exposures and Top Ten Holdings

SPGP is 31% Health Care, which will undoubtedly surprise growth investors. Technology and Financials make up nearly 20% each, but exposures in other sectors are relatively small after that. The defensive nature is evident, especially when compared with the SPDR S&P 500 Growth ETF (SPYG), implying that there weren’t many growth stocks trading at reasonable valuations left when the Index last reconstituted to begin the year.

Morningstar

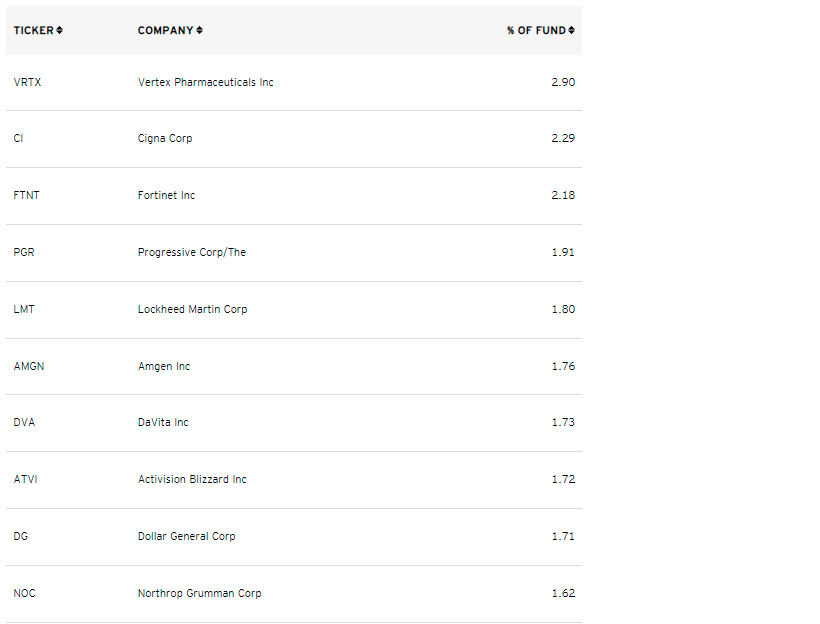

The top ten holdings are shown below, totaling 19.62%. The Index is weighted based on a company’s growth score and is led by Vertex Pharmaceuticals (VRTX). Vertex was the top stock in early January, too, but there have been several significant changes due to performance differences. For example, Progressive (PGR) was the 10th largest holding but is now in 4th place. Lockheed Martin (LMT) previously was in the 31st spot, but the stock has soared 25% YTD due to the war in Ukraine and now occupies SPGP’s 5th spot. In contrast, Teradyne (TER) used to be the 4th largest holding but now sits in 45th place. This year, the entire semiconductor industry has experienced a substantial correction, with the iShares Semiconductor ETF (SOXX) down 23%.

Invesco

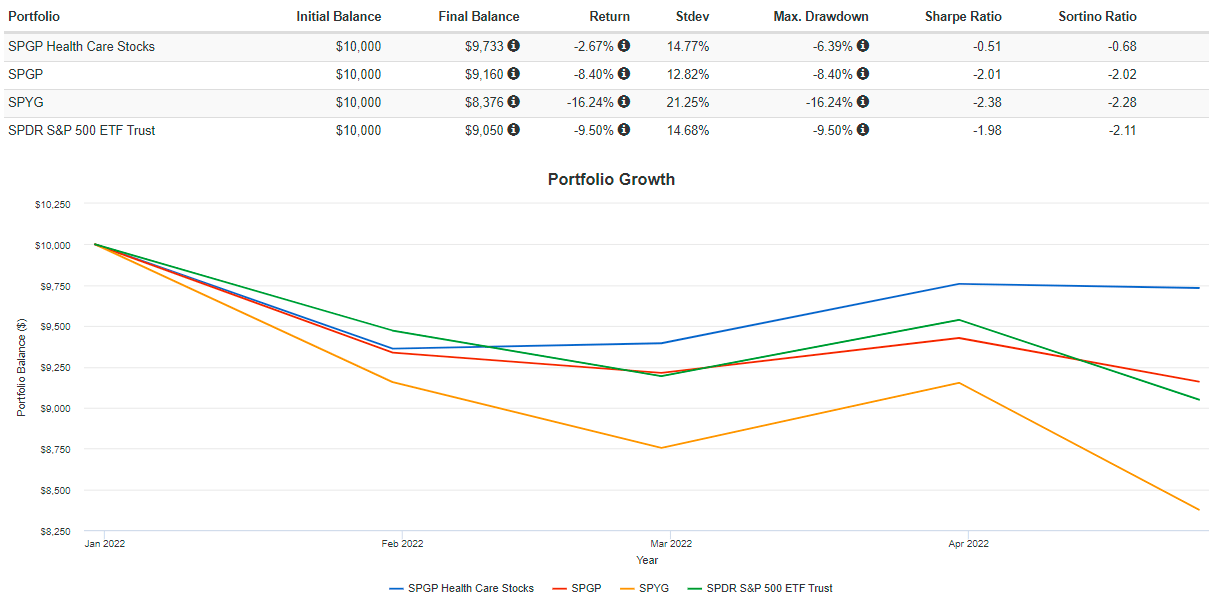

Performance History

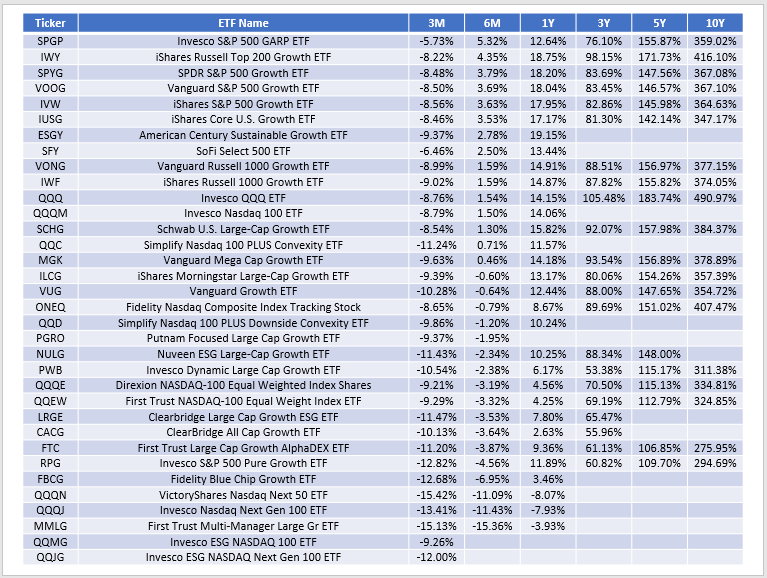

Earlier, I mentioned how SPGP was the best-performing large-cap growth ETF over the last three- and six months. Here are periodic returns for SPGP and 33 of its peers through March 2022, showing SPGP has gained 5.32% from October to March compared to 3.79% for SPYG. SPGP has outperformed by a further 6% this month through April 25, so the valuation screens performed in December were timely.

The Sunday Investor

Fundamental Analysis

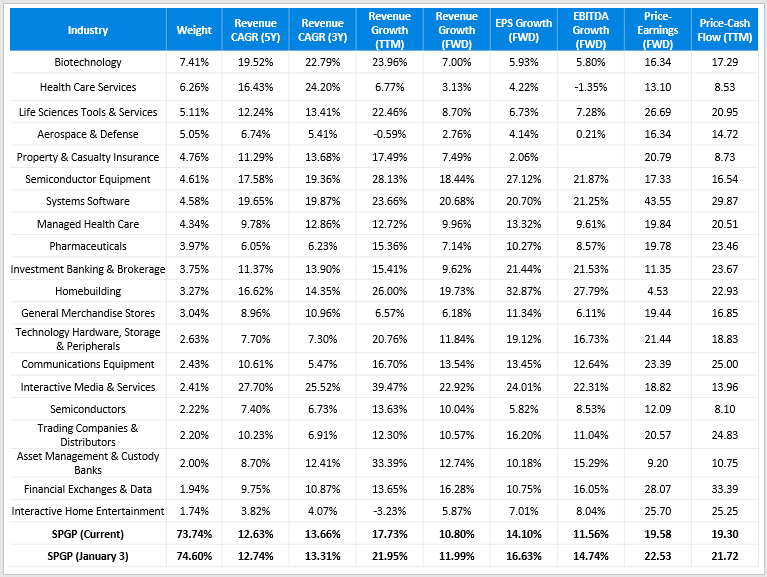

I’m extra cautious of rules-based ETFs during volatile periods. The reason is that during these periods, an Index is less likely to achieve its investment objective as we move farther away from its last reconstitution date, which was almost four months ago. Also, trailing and forward-looking metrics may differ in a fast-changing market, so there’s additional risk in holding these ETFs blindly and assuming the strategy continues to be executed appropriately. To illustrate, consider the table below highlighting SPGP’s growth and valuation metrics today compared to January 3.

The Sunday Investor

First, valuations have declined, as they have for virtually all growth ETFs. SPGP’s weighted-average forward P/E is now 19.58 compared to 22.53 in January, and its trailing price-cash flow ratio is now 19.30 compared to 21.72. Second, forward-looking earnings per share and EBITDA growth rates have declined by about 2.5% and 3%, so overall, SPGP has become more like a value ETF. I found 20 large-cap value ETFs with forward EPS growth rates above 14% and forward P/E’s below 20, so its growth/value combination isn’t exactly impressive.

Dragging down SPGP is its Health Care holdings, which are substantial at 31%. The table below looks at the changes in the last four months in more depth, showing how expectations have sagged yet valuations have remained relatively the same.

The Sunday Investor

Forward revenue growth has declined from 10.14% to 7.44%. Forward EPS growth declined from 14.39% to 8.07%. About two-thirds of companies saw their revenue and earnings per share growth rates decline since January 3 due to a relatively weak quarter. SPGP’s health care stocks had a weighted-average quarterly revenue surprise figure of just 2.87%, which is about on par for the S&P 500 but in line with the general downward trend. And finally, analysts also reduced their earnings expectations. The average Seeking Alpha EPS Revision Grade is now “B-” compared to “B+” in January. Yet, the forward price-earnings ratio remains relatively unchanged (19.71 vs. 20.63), as the Health Care sub-portfolio has held up reasonably well this year. In my view, these mispricings are material, and they will reverse eventually.

Portfolio Visualizer

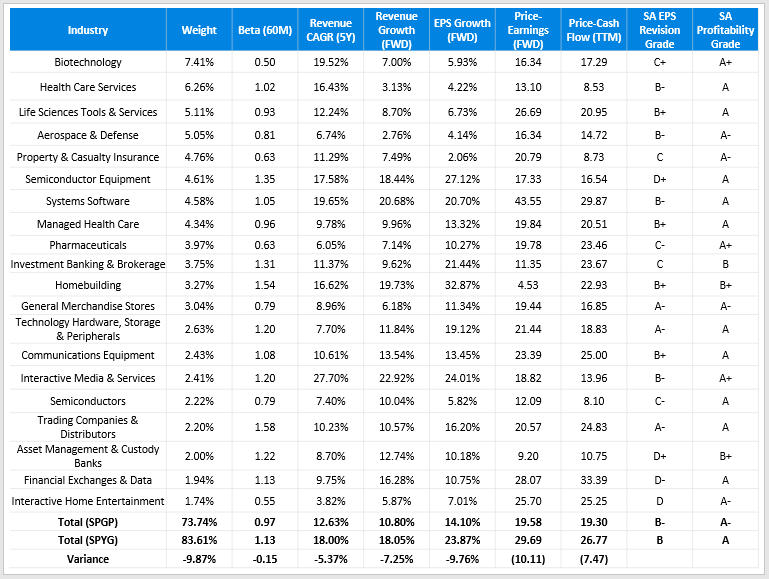

SPGP’s current portfolio offers a very different yet uncompelling alternative to SPYG. Here is a comparison of the two.

The Sunday Investor

Worth noting is that SPGP’s five-year beta is now 0.97 and much lower than the ETF’s 1.17 and SPYG’s 1.13 figures. Growth rates are substantially lower, which is expected when valuation is considered, but now we’re in the ballpark of where many value ETFs are in terms of growth. And their P/E ratios are much lower. For a more diversified fund with a lower P/E and higher growth rates, I suggest looking into the Schwab Fundamental U.S. Large Company Index ETF (FNDX), which I reviewed last month.

Investment Recommendation

I no longer see SPGP as having an advantage over low-fee growth ETFs like SPYG and am downgrading my rating to a hold. I’m surprised at the amount of style drift it experienced in just a few months, and SPGP’s price-earnings ratio didn’t move as much as it should have given the growth downgrade. SPGP is now closer to a value ETF, which is not the target audience.

We have approximately two months until the Index next reconstitutes. Selling to assuage these short-term concerns probably isn’t in your best interest, but I hope this article will cause you to evaluate what you hope to achieve by holding this ETF. SPGP is a growth-focused fund in regular times, but its beta has moved below one, and its growth rates are unimpressive. This suggests that SPGP won’t be a good option once growth stocks recover. I’ll be hoping for a better-looking portfolio come July, and look forward to providing an update then. Thank you for reading, and I hope to discuss this further in the comments section below.

Read More: Invesco S&P 500 GARP ETF: Now A Value ETF, And Not A Great One

{kind=link}