MarkgrafAve/iStock via Getty Images

Introduction

I’ve spent a lot of time discussing dividend growth opportunities this month. That’s based on my focus on these stocks as I prefer dividend growth over high yield and because the market sell-off presented a lot of great opportunities – it still does. I’ve also ignored high yield a bit as most high-yield stocks are likely to encounter a situation of negative real dividend growth in the 1-2 years ahead. In this article, I will explain why that is the case and why I still believe that Southern Company (NYSE:SO) is one of the best high-yield opportunities in a market that makes it incredibly hard for people to buy quality high-yield. The company is yielding 3.6%, dividend growth is very low but sustainable. The valuation is OK and lower bond yields in the future could cause the stock price to continue its rally, generating satisfying total returns for SO investors.

Now, let’s look at the details!

High Yield Risks

I’m overweight dividend growth stocks. Yet, I believe in a healthy mix between high yield (and slow growth) and low yields with higher growth. The closer someone gets to retirement, the more important a high yield becomes.

In my case, I mainly use high yield as a way to get additional cash to invest in my portfolio and because my high yield investments cover areas that would otherwise not be covered: energy, real estate, banks, and utilities.

Now, to get the bad news out of the way first, there are risks to high-yield investing right now. In various articles this month, I highlighted the possibility of negative real dividend growth. Note that real dividend growth is nominal dividend growth (dividend announcements) adjusted for inflation.

Using CME Group’s (CME) S&P 500 Annual Dividend Futures, we see that nominal dividend growth is expected to slow. This includes all S&P 500 holdings, both high yield and low yield – and everything in-between.

CME Group

According to CME,

[…] there are many reasons to be skeptical of the idea that dividend payments will continue to grow rapidly in the 2020s, including the fact that corporate profits are near a record as a percentage of GDP, which might not bode well as input costs soar and as economic activity potentially slows amid tighter fiscal and monetary policy.

Note that nominal dividend expectations are based on S&P 500 Annual Dividend Futures as I already briefly mentioned. This is not based on CME’s opinion.

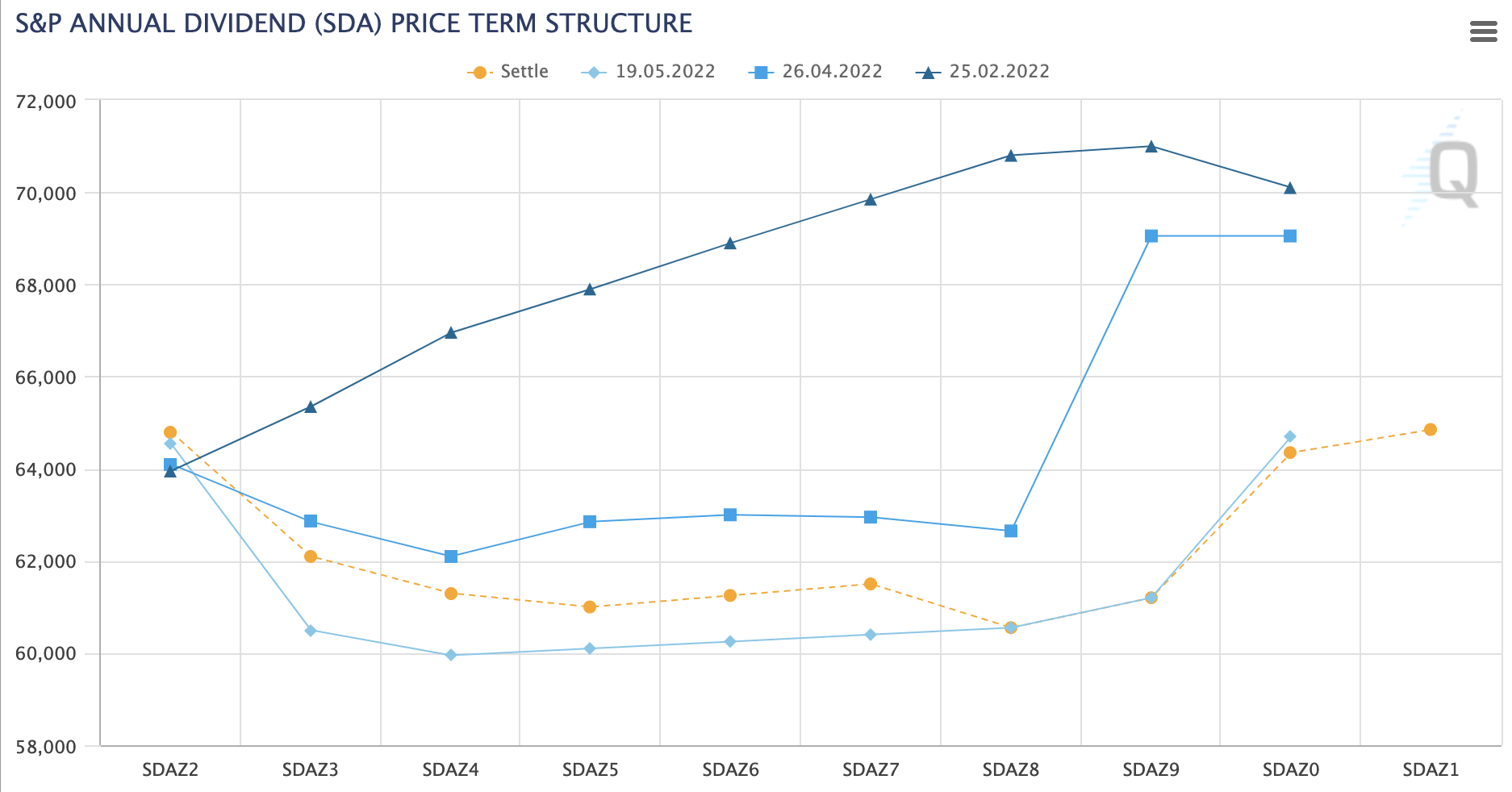

The graph below shows the Dividend Index Futures Term Structure from the Annual Dividend Futures. The X-axis shows the various years. The last number shows which year is covered. For example, SDAZ2 means 2022 expected dividends (the yield multiplied by the S&P 500 in points). SDAZ3 means 2023, and so forth. Going into this year, dividend growth expectations were high. That changed rapidly. As the term structure shows, 2025 dividends are expected to be less than $62 now. That’s down from $68 in February.

CME Group

I’m not making the case that the dividend trajectory will look exactly like this, after all, it’s based on futures that tend to move quickly. However, it does make sense to expect pressure on real dividend growth. Economic growth expectations have come down a lot. Inflation is high, consumer sentiment is low, and supply chain issues are expected to last. Moreover, the trend towards net-zero, labor shortages and related problems are set to cause inflation to more than likely remain above the Fed’s 2% target for an extended period of time.

Southern Company’s Yield

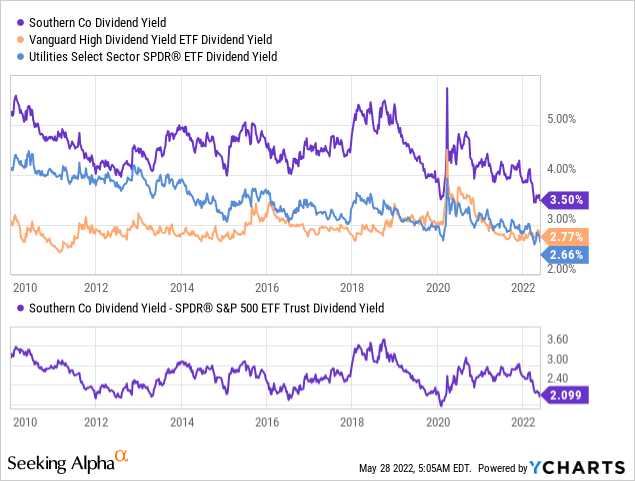

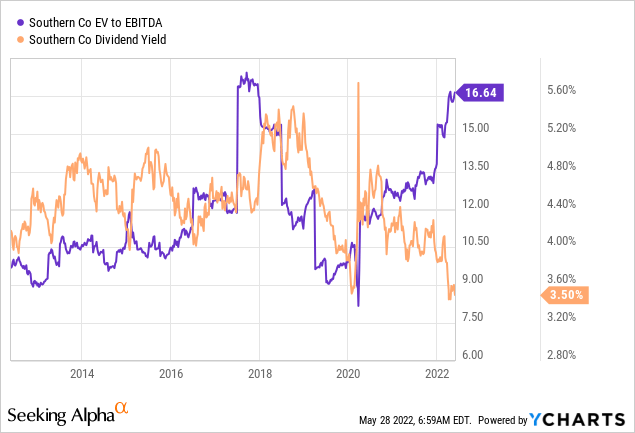

Southern Company distributes a $0.68 quarterly dividend per share. That’s $2.72 per year and a 3.6% yield. In other words, add 10 basis points to the yield in the YCharts graph below. This yield is roughly 100 basis points above its peer average and 80 basis points above the Vanguard High Dividend Yield ETF (VYM). As I’ve said in prior articles, the environment for high-yield investors is dire. Even the high-yield ETF is yielding well below 3%.

Southern Company is yielding 200 basis points above the S&P 500 yield, which is below the median “premium” since 2010 and it is a result of investors rushing to buy quality yield.

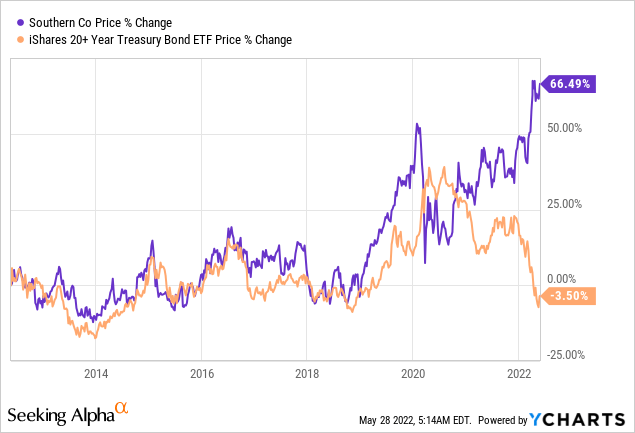

Year-to-date SO is up 11% excluding dividends. This is a remarkable performance because rates have spiked due to high inflation. Generally speaking, SO follows the long-duration bond ETF (TLT). Lower rates and low inflation support utilities because it’s harder for investors to find high-quality yield investments in a low-yield environment. In times when rates are rising, investors often don’t need to buy utilities for yield.

The current divergence is remarkable. High inflation and much higher bond yields have not caused SO (or its peers) to weaken. Investors rushed to buy quality as the stock market took a rather big hit this year – so far.

I don’t believe that SO will have to fall to close the divergence. I believe that once rates start to fall, it will fuel the rally even more. If anything, investors require quality yield – especially if long-term rates start to fall again.

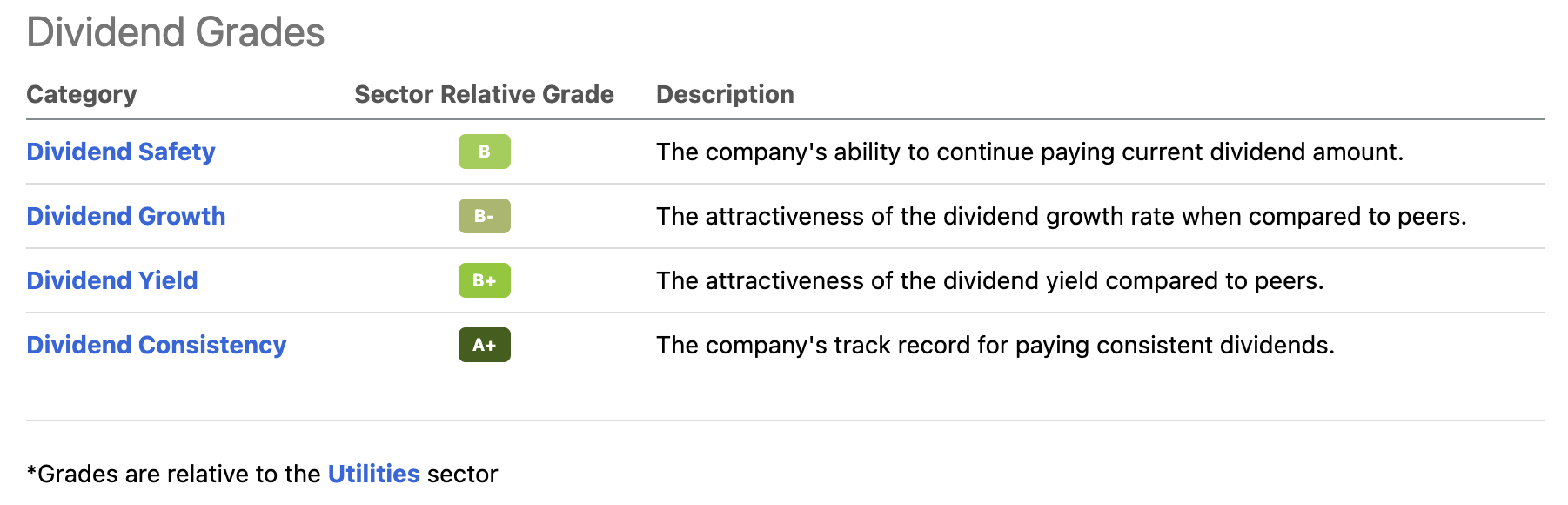

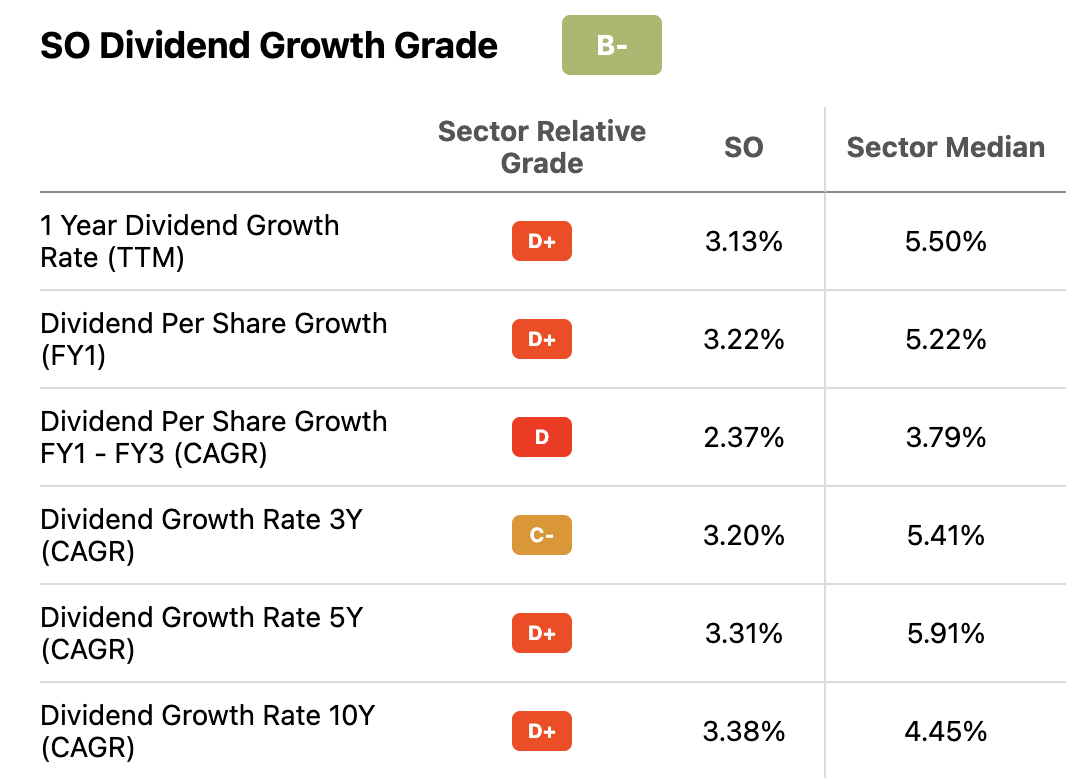

One drawdown of SO’s large yield is its low dividend growth. The Seeking Alpha dividend scorecard grades SO’s dividend growth B-. Note that this is based on numbers and comparisons to the utility sector – not anyone’s opinion.

Seeking Alpha

In this case, I have to “disagree” with B-. When we dig deeper, we find that the CAGR dividend growth rates of the past 3, 5, and 10 years are well below the sector median.

Seeking Alpha

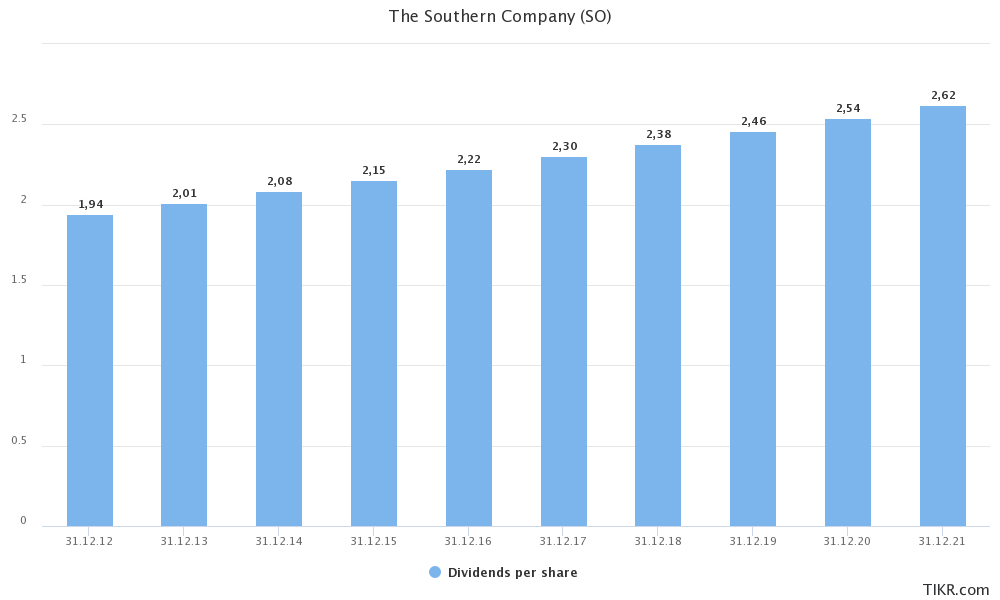

Over the past 3 years, the average dividend growth rate was 3.2%. On April 19, 2022, the company hiked by 3.0%.

TIKR.com

Are these growth rates bad? Absolutely not. It’s what SO is all about. You get a high yield but slow dividend growth. This is only bad for investors who buy a high yield without looking at dividend growth.

However, it more than likely means that its investors will encounter flat to slightly negative longer-term real dividend growth as I believe that longer-term inflation rates will remain close to 3%.

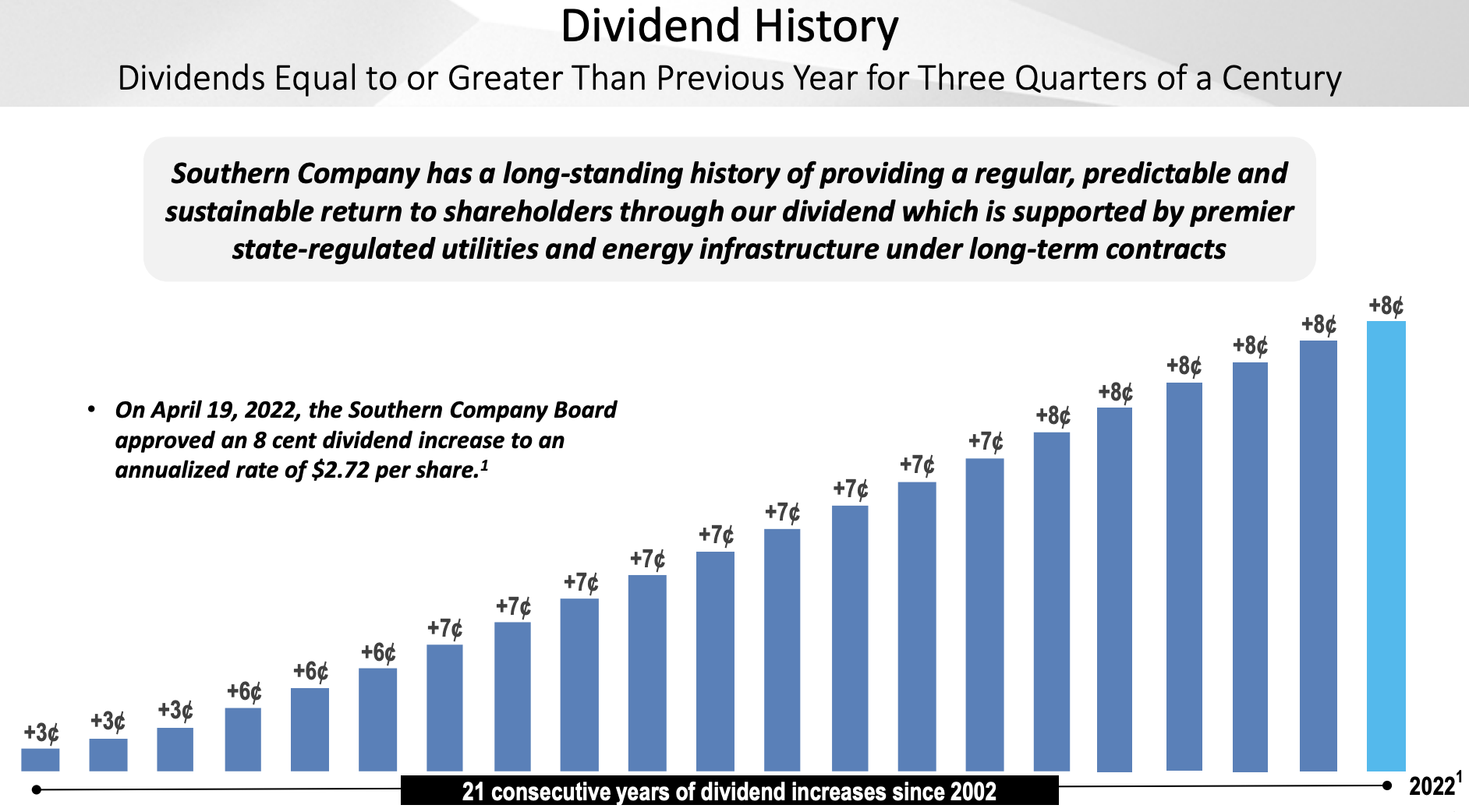

With that in mind, there are pros and cons. The cons are obviously a loss of real investing and spending power based on low or negative expected dividend growth as well as the fact that high yield, in general, isn’t what it used to be in terms of yields. The pros are that Southern Company stands for safety. It has increased dividends for 21 consecutive years since 2002. The hikes have become slow, but it’s still what yield-dependent investors need. I would make the case that investors with a long investment horizon should only buy a very small high-yield exposure. Yet, getting retired investors out of high yield and into high dividend growth for the sake of beating inflation won’t solve anything.

Southern Company

With that said, there is more good news.

Valuation, Balance Sheet, And Current Events

Southern Company aims to be net-zero (no net carbon emissions) by 2050, which follows the Paris agreement. By 2025, the company wants to reduce emissions by 50% compared to 2007 levels. As of 1Q22, the company generates 21% of its energy from coal and 45% from natural gas. While I’m a huge fan of natural gas, it will need to change to comply with the Paris agreement (don’t shoot the messenger, please).

Like all of its peers, Southern Company is accelerating investments in renewables. Its Vogtle 3&4 nuclear energy expansion projects are the most well-known projects in the industry right now. So far, the company has invested $8.7 billion as of March 31, 2021. It estimates that $1.7 billion in additional capital is needed until 4Q23.

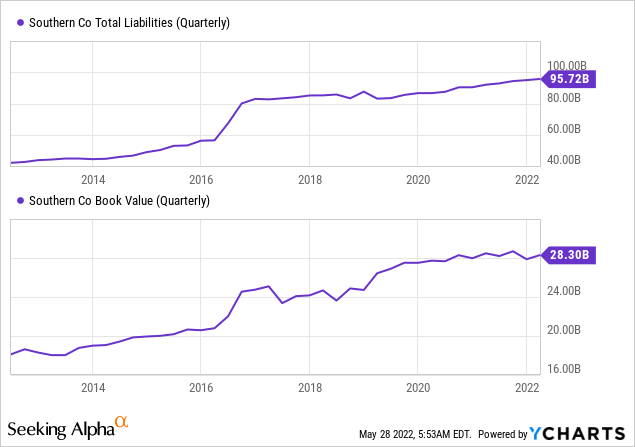

The graph below shows two things. First, total liabilities have exploded. Over the past 10 years, total liabilities have more than doubled to almost $96 billion. However, every penny invested resulted in value as the book value of equity (total assets minus total liabilities) has also steadily increased. If the lower part of the graph below were to display a downtrend, I wouldn’t be discussing this stock today – at least now from a bullish point of view.

This year, the company is expected to end up with $54.0 billion in net financial debt. That’s 5.6x EBITDA. Next year, net debt is expected to be $57.4 billion. That’s higher but 5.5x EBITDA due to outperforming (expected) EBITDA growth.

Moreover, the company uses share offers as a way to finance its business. That’s the opposite of buybacks. Between 2017 and 2021, the number of shares outstanding soared by 6% to 1.06 billion.

That’s fine as long as earnings PER SHARE don’t suffer.

The good news is that that’s not an issue at all as long-term EPS growth is expected to be in the 5% to 7% range:

Southern Company’s adjusted earnings guidance range for 2022 is $3.50 to $3.60 per share vs. consensus of $3.55. In the first quarter of 2022, management estimates Southern Company adjusted earnings per share will be 90 cents. Management continues to project a long-term adjusted earnings per share growth rate for Southern Company in the 5% to 7% range, consistent with adjusted earnings in a range of $4.00 to $4.30 per share in 2024 vs. consensus of $4.11.

Using the company’s $81.3 billion market cap, $57.4 billion in expected 2023 net debt, $1.5 billion in pension-related liabilities, and $4.6 billion in minority interest gives us an enterprise value of $144.8 billion.

This gives us a 13.8x EBITDA valuation using next year’s expected EBITDA of $10.5 billion.

That’s not a great valuation after the stock added roughly 10% since my most recent article. Back then, the valuation was neither cheap nor overvalued. While I’m not making the case that SO is overvalued, I would be more comfortable with prices closer to $70.

Takeaway

It’s a tricky environment for high-yield investors. High yields are still low and even high-quality utilities like Southern Company are now more expensive despite rising rates, which is usually bad for their stock prices.

Moreover, it’s highly likely that real dividend growth…

Read More: Southern Company Stock: 3.6% Yield And Real Dividend Growth (NYSE:SO)

{kind=link}